Target 2004 Annual Report Download - page 33

Download and view the complete annual report

Please find page 33 of the 2004 Target annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

|

|

31

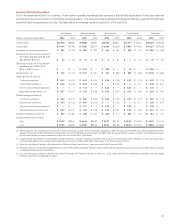

Leasehold

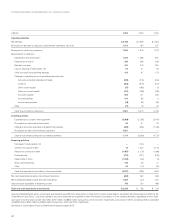

Acquisition

Goodwill Costs Other Total

(millions) 2004 2003 2004 2003 2004 2003 2004 2003

Gross asset $80 $80 $185 $182 $201 $200 $466 $462

Accumulated

amortization (20) (20) (52) (34) (188) (179) (260) (233)

Net goodwill

and intangible

assets $60 $60 $133 $148 $13 $21 $206 $229

As required, we adopted SFAS No. 142, “Goodwill and Other

Intangible Assets,” during the first quarter of 2002. In 2004, 2003 and

2002, the adoption of this statement reduced annual amortization

expense of certain intangible assets by approximately $5 million (less

than $.01 per share). The estimated aggregate amortization expense

of our definite-lived intangible assets for each of the five succeeding

fiscal years, 2005 to 2009, is expected to be $24 million, $22 million,

$20 million, $19 million and $19 million, respectively. During 2004,

goodwill with an approximate carrying value of $63 million was sold as

part of the Marshall Field’s transaction. There was no goodwill included

in the Mervyn’s sale transaction that also occurred in 2004.

Discounted cash flow models were used in determining fair value

for the purposes of the required annual goodwill impairment analysis.

No impairments were recorded in 2004, 2003 and 2002 as a result of

the tests performed.

Accounts Payable

Our accounting policy is to reduce accounts payable when checks

to vendors clear the bank from which they were drawn. Outstanding

checks included in accounts payable were $992 million and $966

million at year-end 2004 and 2003, respectively.

Accrued Liabilities

Accrued liabilities as of January 29, 2005 and January 31, 2004

consist of the following:

2004 2003

Wages and benefits $ 412 $ 369

Taxes payable 287 245

Gift card liability 214 169

Other 720 505

Tot al $1,633 $1,288

Taxes payable consist of real estate, employee withholdings and sales tax liabilities.

Gift card liability represents the amount of gift cards that have been issued but have

not been presented for redemption.

Commitments and Contingencies

At January 29, 2005, our obligations included notes and debentures

of $9,447 million (discussed in detail under Notes Payable and Long-

term Debt below), the present value of capital lease obligations

of $91 million and total future payments of operating leases with

total contractual lease payments of $3,049 million, including certain

options to extend the lease term that are expected to be exercised

in the amount of $1,415 million (discussed in detail under Leases on

page 32). In addition, commitments for the purchase, construction,

lease or remodeling of real estate, facilities and equipment were

approximately $544 million at year-end 2004. Merchandise royalty

commitments of approximately $102 million are due during the five-

year period ending in 2009. Throughout the year, we enter into various

commitments to purchase inventory. In addition to the accounts

payable reflected in our Consolidated Statements of Financial Position

on page 25, we had commitments with various vendors for the

purchase of inventory as of January 29, 2005. These purchase com-

mitments are cancelable by their terms.

We expect to receive a share of the proceeds from the $3 billion

Visa/MasterCard antitrust litigation settlement, as we are a member of

the class action lawsuit. However, the amount and timing of the pay-

ment are not certain at this time.

We are exposed to claims and litigation arising out of the ordinary

course of business and use various methods to resolve these matters

in a manner that we believe serves the best interest of our shareholders

and other constituents. Our policy is to disclose pending lawsuits and

other known claims that we expect may have a material impact on

our results of operations, cash flows or financial condition. Other than

the matter discussed above, we do not believe any of the currently

identified claims and litigated matters meet this criterion, either

individually or in the aggregate.

Notes Payable and Long-term Debt

At January 29, 2005, no notes payable were outstanding. The average

amount of notes payable outstanding during 2004 was $55 million at

a weighted average interest rate of 1.3 percent. In 2004, notes payable

balances fluctuated significantly during the year due to seasonal

financing needs, proceeds from sale of Marshall Field’s and Mervyn’s

and other factors. On July 28, 2004, our short-term borrowing reached

$1,422 million, its highest level for the year.

At January 31, 2004, no notes payable were outstanding. The

average amount of notes payable outstanding during 2003 was

$377 million at a weighted average interest rate of 1.2 percent. On

October 31, 2003, our short-term borrowing reached $1,409 million,

its highest level for the year.

At January 29, 2005, two committed credit agreements totaling

$1,600 million were in place through a group of 25 banks at specified

rates. Of these credit lines, an $800 million credit facility expires in

June 2005 and includes a one-year term-out option to June 2006.

The remaining $800 million credit facility expires in June 2008. There

were no balances outstanding at any time during 2004 or 2003 under

these agreements.

In 2004, we issued no long-term debt. We called or repurchased

$542 million of long-term debt with an average remaining life of 24

years and a weighted average interest rate of 7.0 percent, resulting in

a pre-tax loss of $89 million (approximately $.06 per share), reflected

in interest expense.

In 2003, we issued $500 million of long-term debt maturing in

2008 at 3.38 percent, $200 million of long-term debt maturing in 2018

at 4.88 percent and $500 million of long-term debt maturing in 2013

at 4.00 percent. We also called or repurchased $297 million of long-

term debt with an average remaining life of 20 years and a weighted

average interest rate of 7.8 percent, resulting in a pre-tax loss of $15

million (approximately $.01 per share), reflected in interest expense.

The portion of long-term debt secured by credit card receivables

was $750 million at January 29, 2005. On January 31, 2004, we had

$1,500 million of long-term debt secured by credit card receivables,

$750 million of which was classified as current portion of long-term debt.