Target 2004 Annual Report Download - page 20

Download and view the complete annual report

Please find page 20 of the 2004 Target annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

|

|

1818

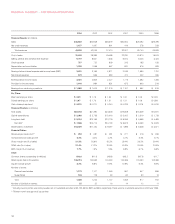

In 2004, our consolidated SG&A expense rate increased to 21.4

percent compared to 21.2 percent in 2003. Approximately half of the

year-over-year increase was attributable to a change in the method

of accounting for leases. See further discussions in the Notes to

Consolidated Financial Statements on page 32. The primary driver

of the remaining increase was higher workers’ compensation costs.

In 2003, our consolidated SG&A expense rate rose to 21.2

percent compared to 20.5 percent in 2002 primarily due to the reclas-

sification of vendor income.

In 2005, we expect our SG&A expense rate to be equal to or

increase slightly from 2004, reflecting our belief that certain expenses,

such as health care costs, will increase at a faster pace than sales.

Depreciation and Amortization

In 2004, depreciation and amortization increased 14.6 percent to

$1,259 million compared to 2003. Depreciation and amortization

expense grew faster than sales partially due to accelerated depreci-

ation on existing stores that were planned to be closed, or torn down

and rebuilt. In 2003, depreciation and amortization increased 13.6

percent to $1,098 million compared to 2002 due to new store growth.

In 2005, we expect depreciation and amortization to increase in line

with our sales growth.

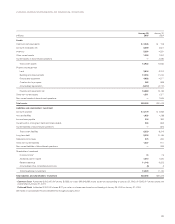

Credit Card Contribution

We offer credit to qualified guests through our branded credit cards:

the Target Visa and proprietary Target Card. Our credit card products

strategically support earnings growth by driving sales at our stores

and through the continued growth of our credit card contribution.

Our credit card revenues are primarily derived from finance

charges, late fees and other revenues. Also, third-party merchant fees

are paid to us by merchants who have accepted the Target Visa credit

card. In 2004 and 2003, our net credit card revenues increased 5.5

percent and 23.2 percent, respectively, due to continued growth in

the Target Visa portfolio.

Credit card expenses include a bad debt provision as well as

operations and marketing expenses supporting our credit card

portfolio. In 2004, our bad debt provision decreased $25 million to

$451 million, primarily due to improved quality of the portfolio. In 2003,

our bad debt provision increased $85 million to $476 million, primarily

due to the substantial growth of the Target Visa portfolio. In 2004,

2003 and 2002, the allowance for doubtful accounts as a percent of

year-end receivables was 7.1 percent, 7.1 percent and 7.0 percent,

respectively.

In 2004, operations and marketing expense increased to $286

million from $246 million in 2003 and $238 million in 2002, primarily

due to the growth of the Target Visa portfolio.

We expect our 2005 credit card operations to grow at a rate

similar to our growth rate in 2004. Our pre-tax credit card contribution

as a percent of total average receivables is expected to continue to be

in line with recent performance. The impact of the change to our

revenue related to a prime-based floating rate instead of a fixed rate,

as discussed on pages 19 and 21, will be determined by future

changes in the prime rate.

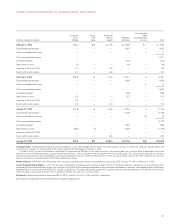

Credit Card Contribution

(millions) 2004 2003 2002

Revenues:

Finance charges, late fees

and other revenues $1,059 $1,015 $ 821

Merchant fees

Intracompany 65 49 49

Third-party 98 82 70

Total revenues 1,222 1,146 940

Expenses:

Bad debt provision 451 476 391

Operations and marketing 286 246 238

Total expenses 737 722 629

Pre-tax credit card contribution $ 485 $ 424 $ 311

As a percent of average receivables 9.8% 9.1% 8.8%

Receivables

(millions, before allowance) 2004 2003 2002

Year-end receivables $5,456 $4,973 $4,601

Average receivables $4,927 $4,661 $3,515

Past Due

Accounts with three or more

payments past due as a percent

of year-end receivables: 3.5% 4.2% 4.0%

Allowance for Doubtful Accounts

(millions) 2004 2003 2002

Allowance at beginning of year $352 $ 320 $ 180

Bad debt provision 451 476 391

Net write-offs (416) (444) (251)

Allowance at end of year $387 $ 352 $ 320

As a percent of year-end receivables 7.1% 7.1% 7.0%

Other Credit Card Contribution Information

2004 2003 2002

Total revenues as a percent

of average receivables: 24.8% 24.6% 26.7%

Net write-offs as a percent

of average receivables: 8.4% 9.5% 7.1%