Target 2013 Annual Report Download - page 24

Download and view the complete annual report

Please find page 24 of the 2013 Target annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

|

|

19

outstanding receivables at the time of closing, and a $225 million beneficial interest asset. The beneficial interest

asset effectively represents a receivable for the present value of future profit-sharing we expect to receive on the

receivables sold. Based on historical payment patterns, we estimate that the beneficial interest asset will be reduced

over a four-year period following the sale, with larger reductions in the early years. As of February 1, 2014, a $127

million beneficial interest asset remained. Concurrent with the sale of the portfolio, we repaid the nonrecourse debt

collateralized by credit card receivables (2006/2007 Series Variable Funding Certificate) at par of $1.5 billion, resulting

in net cash proceeds of $4.2 billion.

TD now underwrites, funds and owns Target Credit Card and Target Visa consumer receivables in the U.S. TD controls

risk management policies and oversees regulatory compliance, and we perform account servicing and primary

marketing functions. We earn a substantial portion of the profits generated by the Target Credit Card and Target Visa

portfolios. Income from the TD profit-sharing arrangement and our related account servicing expenses are classified

within SG&A expenses in the U.S. Segment.

Beginning with the first quarter of 2013, we no longer report a U.S. Credit Card Segment.

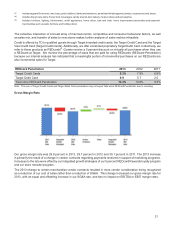

Analysis of Results of Operations

U.S. Segment

U.S. Segment Results Percent Change

(dollars in millions) 2013 2012 (a) 2011 2013/2012 2012/2011

Sales $71,279 $ 71,960 $ 68,466 (0.9)% 5.1%

Cost of sales 50,039 50,568 47,860 (1.0) 5.7

Gross margin 21,240 21,392 20,606 (0.7) 3.8

SG&A expenses (b) 14,285 13,759 13,079 3.8 5.2

EBITDA 6,955 7,633 7,527 (8.9) 1.4

Depreciation and amortization 1,996 2,044 2,084 (2.4) (1.9)

EBIT $ 4,959 $ 5,589 $ 5,443 (11.3)% 2.7%

Note: Prior period segment results have been revised to reflect the combination of our historical U.S. Retail Segment and U.S. Credit Card

Segment into one U.S. Segment. Quarterly and full-year historical information for the three most recently completed years reflecting the results

for the U.S. Segment and Canadian Segment are attached as Exhibit (99) to our current report on Form 8-K filed April 16, 2013.

Note: See Note 28 to our Consolidated Financial Statements for a reconciliation of our segment results to earnings before income taxes.

(a) Consisted of 53 weeks.

(b) SG&A includes credit card revenues and expenses for all periods presented prior to the March 2013 sale of our U.S. consumer credit

card portfolio to TD. For 2013, SG&A also includes $653 million of profit-sharing income from the arrangement with TD.

U.S. Segment Rate Analysis Twelve Months Ended February 2, 2013 2013 U.S. Segment Change vs. 2012

Twelve Months

Ended

February 1,

2014 U.S. Segment,

as revised

Impact of

Historical U.S.

Credit Card

Segment(a)

Historical

U.S. Retail

Segment U.S. Segment,

as revised

Historical

U.S. Retail

Segment

Gross margin rate 29.8% 29.7% — pp 29.7% 0.1pp 0.1pp

SG&A expense rate 20.0 19.1 (0.8)19.9 0.9 0.1

EBITDA margin rate 9.8 10.6 0.8 9.8 (0.8)—

Depreciation and amortization

expense rate 2.8 2.8 — 2.8 — —

EBIT margin rate 7.0 7.8 0.8 7.0 (0.8)—