Walmart 2007 Annual Report Download - page 50

Download and view the complete annual report

Please find page 50 of the 2007 Walmart annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

|

|

Wal-Mart 2007 Annual Report 48

Net Investment Instruments

At January 31, 2007, the Company is party to cross-currency interest

rate swaps that hedge its net investment in the United Kingdom. At

January 31, 2006, the Company was party to cross-currency interest

rate swaps that hedge its net investments in the United Kingdom and

Japan. The agreements are contracts to exchange xed-rate payments

in one currency for xed-rate payments in another currency.

The Company has outstanding approximately £3.0 billion and

£2.0 billion of debt that is designated as a hedge of the Company’s

net investment in the United Kingdom as of January 31, 2007 and

2006, respectively. The Company also has outstanding approximately

¥142.1 billion and ¥87.1 billion of debt that is designated as a hedge

of the Company’s net investment in Japan at January 31, 2007 and

2006, respectively. All changes in the fair value of these instruments

are recorded in accumulated other comprehensive income, o set-

ting the foreign currency translation adjustment that is also recorded

in accumulated other comprehensive income.

Cash Flow Instruments

The Company was party to a cross-currency interest rate swap to

hedge the foreign currency risk of certain foreign-denominated

debt. The swap was designated as a cash flow hedge of foreign

currency exchange risk. The agreement was a contract to exchange

fixed-rate payments in one currency for fixed-rate payments in

another currency. Changes in the foreign currency spot exchange

rate resulted in reclassification of amounts from accumulated

other comprehensive income to earnings to offset transaction

gains or losses on foreign-denominated debt. The instruments

matured in fiscal 2007.

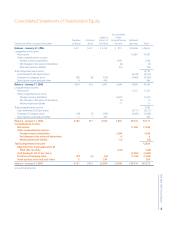

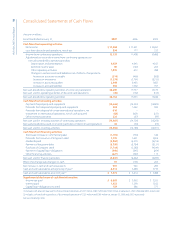

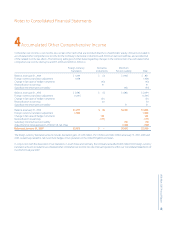

Notes to Consolidated Financial Statements

Hedging instruments with an unrealized gain are recorded on the

Consolidated Balance Sheets in other current assets or other assets

and deferred charges, based on maturity date. Those instruments

with an unrealized loss are recorded in accrued liabilities or deferred

income taxes and other, based on maturity date.

Cash and cash equivalents: The carrying amount approximates fair value

due to the short maturity of these instruments.

Long-term debt: Fair value is based on the Company’s current incremental

borrowing rate for similar types of borrowing arrangements.

Fair value instruments and net investment instruments: The fair values are

estimated amounts the Company would receive or pay to terminate

the agreements as of the reporting dates.

Fair Value of Financial Instruments

Instrument Notional Amount Fair Value

Fiscal Year Ended January 31, (in millions) 2007 2006 2007 2006

Derivative nancial instruments designated for hedging:

Receive xed-rate, pay oating rate interest rate swaps designated as fair value hedges $ 5,195 $ 6,945 $ (1) $ 133

Receive xed-rate, pay xed-rate cross-currency interest rate swaps designated

as net investment hedges (Cross-currency notional amount: GBP 795 at

1/31/2007 and 1/31/2006) 1,250 1,250 (181) (107)

Receive xed-rate, pay xed-rate cross-currency interest rate swap designated

as a cash ow hedge (Cross-currency notional amount: CAD 0 and CAD 503

at 1/31/2007 and 1/31/2006, respectively) – 325 – (120)

Receive xed-rate, pay xed-rate cross-currency interest rate swap designated

as a net investment hedge (Cross-currency notional amount: ¥0 and ¥52,056

at 1/31/2007 and 1/31/2006, respectively) – 432 – (17)

Total $ 6,445 $ 8,952 $ (182) $ (111)

Non-derivative nancial instruments:

Long-term debt $32,650 $31,024 $32,521 $31,580