Walmart 2007 Annual Report Download - page 61

Download and view the complete annual report

Please find page 61 of the 2007 Walmart annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68

|

|

Wal-Mart 2007 Annual Report 59

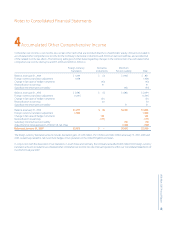

Notes to Consolidated Financial Statements

13

Recent Accounting

Pronouncements

In June 2006, the Emerging Issues Task Force reached a consensus on

Issue No. 06-3 (“EITF 06-3”), “Disclosure Requirements for Taxes Assessed

by a Governmental Authority on Revenue-Producing Transactions.”

The consensus allows an entity to choose between two acceptable

alternatives based on their accounting policies for transactions in which

the entity collects taxes on behalf of a governmental authority, such

as sales taxes. Under the gross method, taxes collected are accounted

for as a component of sales revenue with an offsetting expense.

Conversely, the net method allows a reduction to sales revenue.

Entities should disclose the method selected pursuant to APB No. 22,

“Disclosure of Accounting Policies.” If such taxes are reported gross

and are signi cant, entities should disclose the amount of those taxes.

The guidance should be applied to nancial reports through retrospec-

tive application for all periods presented, if amounts are signi cant, for

interim and annual reporting beginning February 1, 2007. Historically,

the Company has presented sales net of tax collected.

In July 2006, the Financial Accounting Standards Board (“FASB”) issued

Interpretation No. 48, “Accounting for Uncertainty in Income Taxes”

(“FIN 48”). FIN 48 clari es the accounting for income taxes, by prescrib-

ing a minimum recognition threshold a tax position is required to

meet before being recognized in the nancial statements. FIN 48 also

provides guidance on derecognition, measurement, classi cation,

interest and penalties, accounting in interim periods, disclosure and

transition. The Company will adopt FIN 48 on February 1, 2007, as

required and for which the cumulative e ect will be recorded in

retained earnings. The Company is currently evaluating the

Interpretation to determine the impact the Interpretation will have

on its nancial condition, results of operations or liquidity.

In September 2006, the FASB issued Statement of Financial Accounting

Standards No. 157, “Fair Value Measurements” (“SFAS 157”). This stan-

dard de nes fair value, establishes a framework for measuring fair value

in generally accepted accounting principles and expands disclosures

about fair value measurements. The Company will adopt SFAS 157 on

February 1, 2008, as required. The adoption of SFAS 157 is not expected

to have a material impact on the Company’s nancial condition,

results of operations or liquidity.

In September 2006, the FASB also issued Statement of Financial

Accounting Standards No. 158, “Employers’ Accounting for De ned

Bene t Pension and Other Postretirement Plans – an amendment of

FASB Statements No. 87, 88, 106 and 132(R)” (“SFAS 158”). This standard

requires recognition of the funded status of a bene t plan in the state-

ment of nancial position. The standard also requires recognition in

other comprehensive income of certain gains and losses that arise

during the period but are deferred under pension accounting rules, as

well as modi es the timing of reporting and adds certain disclosures.

The Company adopted the funded status recognition and disclosure

elements as of January 31, 2007, and will adopt measurement elements

as of January 31, 2009, as required by SFAS 158. The adoption of

SFAS 158 did not have a material impact on the Company’s finan-

cial condition, results of operations or liquidity.

In September 2006, the Securities and Exchange Commission (“SEC”)

issued Sta Accounting Bulletin No. 108, “Considering the E ects of

Prior Year Misstatements when Quantifying Misstatements in Current

Year Financial Statements” (“SAB 108”), in which the Sta provides guid-

ance on the consideration of the e ects of prior year misstatements in

quantifying current year misstatements for the purpose of assessing

materiality. The Company adopted SAB 108 as of January 31, 2007, as

required. The adoption of SAB 108 did not have a material impact on

the Company’s nancial condition, results of operations or liquidity.

In February 2007, the FASB issued Financial Accounting Standards

No. 159, “The Fair Value Option for Financial Assets and Financial

Liabilities – Including an amendment of FASB Statement No. 115”

(“SFAS 159”). SFAS 159 permits companies to measure many nancial

instruments and certain other items at fair value at speci ed election

dates. SFAS 159 will be effective beginning February 1, 2008. The

Company is currently assessing the impact of SFAS 159 on its

financial statements.

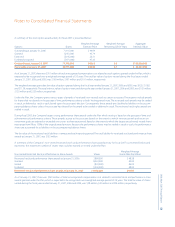

14 Subsequent Events

On March 8, 2007, the Company’s Board of Directors approved

an increase in the Company’s annual dividend to $0.88 per share.

The annual dividend will be paid in four quarterly installments

on April 2, 2007, June 4, 2007, September 4, 2007, and January 2,

2008 to holders of record on March 16, May 18, August 17 and

December 14, 2007, respectively.

In February 2007, the Company announced the purchase of a 35%

interest in Bounteous Company Ltd. (“BCL”). BCL operates 101 hyper-

markets in 34 cities in China under the Trust-Mart banner. The purchase

price for the 35% interest was $264 million. Also in February 2007, the

Company paid $376 million to purchase a loan issued to the selling

BCL shareholders which is securitized by the remaining equity of BCL.

Concurrent with the initial investment in BCL, the Company entered

into a stockholders agreement which provides the Company with

voting rights associated with a portion of the common stock of BCL

secured by the loan, amounting to an additional 30% of the aggregate

outstanding shares. Pursuant to the purchase agreement, the Company

is committed to purchase the remaining interest in BCL on or before

February 2010 subject to certain conditions. The nal purchase price

for the remaining interest will be approximately $320 million, net of

loan repayments and subject to reduction under certain circumstances.