American Express 2015 Annual Report Download - page 52

Download and view the complete annual report

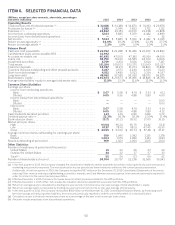

Please find page 52 of the 2015 American Express annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

|

|

suffer due to our customers’ association with certain countries, persons or entities or the existence of any such

transactions. In addition, Member States of the European Economic Area have implemented the PSD for electronic

payment services that put in place a common legal framework for licensing and supervision of payment services

providers, including card issuers and merchant acquirers, and for their conduct of business. Complying with these and

other regulations increases our costs and could reduce our revenue opportunities.

Various regulatory agencies and legislatures are also considering regulations and legislation covering identity

theft, account management guidelines, credit bureau reporting, disclosure rules, security and marketing that would

impact us directly, in part due to increased scrutiny of our underwriting and account management standards. These

new requirements may restrict our ability to issue charge and credit cards or partner with other financial institutions,

which could adversely affect our revenue growth.

See “Supervision and Regulation” for more information about the material laws and regulations to which we are subject.

Litigation and regulatory actions could subject us to significant fines, penalties, judgments and/or

requirements resulting in significantly increased expenses, damage to our reputation and/or a material

adverse effect on our business.

Businesses in the financial services and payments industries have historically been subject to significant legal

actions, including class action lawsuits. Many of these actions have included claims for substantial compensatory or

punitive damages. While we have historically relied on our arbitration clause in agreements with customers to limit our

exposure to class action litigation, there can be no assurance that we will continue to be successful in enforcing our

arbitration clause in the future. On October 7, 2015, the CFPB announced a proposal that would, among other changes,

require that our consumer arbitration clause not apply to cases filed in court as class actions, unless and until class

certification is denied or the class claims are dismissed. This proposal is the beginning of a rulemaking process that

may not result in a final rule, if any, becoming effective before 2018. The continued focus of merchants on issues

relating to the acceptance of various forms of payment may lead to additional litigation and other legal actions. Given

the inherent uncertainties involved in litigation, and the very large or indeterminate damages sought in some matters

asserted against us, there is significant uncertainty as to the ultimate liability we may incur from litigation matters.

We have been subject to regulatory actions by the CFPB and other regulators and may continue to be involved in

such actions, including governmental inquiries, investigations and enforcement proceedings, in the event of

noncompliance or alleged noncompliance with laws or regulations. Regulatory action could subject us to significant fines,

penalties or other requirements resulting in increased expenses, limitations or conditions on our business activities, and

damage to our reputation and our brand, which could adversely affect our results of operations and financial condition.

The recent trend towards larger settlement amounts could lead to more adverse outcomes in any enforcement actions

against us in the future. We expect that regulators will continue taking formal enforcement actions against financial

institutions in addition to addressing supervisory concerns through non-public supervisory actions or findings, which

could involve restrictions on our activities, among other limitations that could adversely affect our business.

We are subject to capital adequacy and liquidity rules, and if we fail to meet these rules, our business would be

adversely affected.

Failure to meet current or future capital or liquidity requirements, including those imposed by the New Capital Rules,

the LCR or by regulators in implementing other portions of the Basel III framework, could compromise our competitive

position and could result in restrictions imposed by the Federal Reserve, including limiting our ability to pay common

stock dividends, repurchase our common stock, invest in our business, expand our business or engage in acquisitions.

There continues to be substantial uncertainty regarding significant portions of the capital and liquidity regime that will apply

to us and our U.S. bank subsidiaries. As a result, the ultimate impact on our long-term capital and liquidity planning and our

results of operations is not certain, although an increase in our capital and liquid asset levels could lower our return on equity.

The capital requirements applicable to the Company as a bank holding company and our U.S. bank subsidiaries have

been substantially revised to implement the international Basel III framework and are in the process of being phased-in.

Once these revisions are fully phased-in, the Company and our U.S. bank subsidiaries will be required to satisfy more

stringent capital adequacy standards than in the past. As part of our required stress testing, both internally and by the

Federal Reserve, we must continue to comply with applicable capital standards in the adverse and severely adverse

economic scenarios published by the Federal Reserve each year. To satisfy these requirements, it may be necessary for us

to hold additional capital in excess of that required by the New Capital Rules as they are phased-in.

Compliance with capital adequacy and liquidity rules, including the New Capital Rules and the LCR, will require a material

investment of resources. An inability to meet regulatory expectations regarding our compliance with applicable capital

adequacy and liquidity rules may also negatively impact the assessment of the Company and our U.S. bank subsidiaries by

federal banking regulators.

We continue to progress through the parallel run phase of Basel III advanced approaches implementation.

Depending on how the advanced approaches are ultimately implemented for our asset types, our capital ratios

41