American Express 2015 Annual Report Download - page 66

Download and view the complete annual report

Please find page 66 of the 2015 American Express annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

|

|

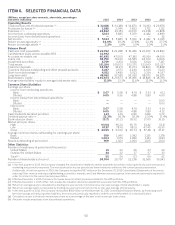

TOTAL REVENUES NET OF INTEREST EXPENSE

Discount revenue remained relatively flat in 2015 compared to 2014, and increased $798 million or 4 percent in

2014 compared to 2013, driven by 2 percent and 7 percent growth in billed business, respectively, offset by a decline in

the average discount rate, faster growth in GNS billings than in overall Company billings, increases in contra-discount

revenues, such as cash rebate rewards and higher payments during 2015 related to cobrand partnership agreements.

U.S. billed business increased 5 percent, and non-U.S. billed business increased 8 percent on an FX-adjusted basis in

2015 compared to 2014, due to increases in average spending per proprietary basic card and basic cards-in-force.1

The average discount rate was 2.46 percent, 2.48 percent and 2.51 percent for 2015, 2014 and 2013, respectively.

The decrease in the average discount rate in 2015 compared to 2014 was driven, in part, by growth of the OptBlue

program to expand card acceptance by U.S. small merchants, changes in industry mix and competition, partially offset

by the decline in Costco merchant volume in Canada (which was at a lower discount rate than the average) due to the

expiration of our merchant agreement. The average discount rate will likely decline by a greater amount during 2016

due to the continued expansion of Optblue, a greater impact from international regulatory changes and continued

competitive pressures. Overall, changes in the mix of spending by location and industry, merchant incentives and

concessions, volume related pricing discounts, strategic investments, certain pricing initiatives, competition, pricing

regulation (including regulation of competitors’ interchange rates) and other factors will likely result in continued

erosion of our discount rate over time. See Tables 5 and 6 for more details on billed business performance and the

average discount rate.

Net card fees remained relatively flat in 2015 compared to 2014 and increased $81 million or 3 percent in 2014

compared to 2013, while FX-adjusted net card fees increased 5 percent in both periods.1The increases in both years

on an FX-adjusted basis were primarily driven by higher average proprietary cards-in-force. The current year increase

also reflects a benefit from certain pricing initiatives.

Travel commissions and fees decreased $769 million or 69 percent in 2015 compared to 2014 and $795 million or

42 percent in 2014 compared to 2013. The decreases in both years were primarily due to the business travel joint

venture transaction, resulting in a lack of comparability between periods.

Other commissions and fees remained relatively flat in 2015 compared to 2014 and increased $94 million or 4

percent in 2014 compared to 2013. FX-adjusted other commissions and fees increased 9 percent in 2015 compared to

2014 and 6 percent in 2014 compared to 2013. 1The increases, on an FX-adjusted basis, in both periods were primarily

driven by higher loyalty coalition revenues, as well as higher delinquency fees.

Other revenues decreased $956 million or 32 percent in 2015 compared to 2014 and increased $715 million or 31

percent in 2014 compared to 2013. The decrease in the current year was primarily driven by prior-year gains related to

the sales of investment securities in Concur, and the sales of investment securities in Industrial and Commercial Bank

of China. The increase in the prior year was primarily driven by the gains on the sales of our investment securities in

Concur, revenues earned related to the GBT JV transition services agreement, and higher Loyalty Edge revenues,

partially offset by the loss of revenue from the publishing business, which was sold in the fourth quarter of 2013.

Interest income increased $366 million or 5 percent in 2015 compared to 2014, and $174 million or 2 percent in

2014 compared to 2013. The increase in both years primarily reflects higher average Card Member loans, partially

offset by decreases in interest and dividends on investment securities, driven by lower average investment securities.

Interest expense decreased $84 million or 5 percent in 2015 compared to 2014, and $251 million or 13 percent in

2014 compared to 2013. The decrease in both years was primarily driven by a lower cost of funds on debt and

customer deposits, partially offset by increases in average customer deposit balances.

1The foreign currency adjusted information assumes a constant exchange rate between the periods being compared for purposes of currency

translation into U.S. dollars (e.g., assumes the foreign exchange rates used to determine results for the current year apply to the corresponding

year period against which such results are being compared). Certain amounts included in the calculations of foreign currency-adjusted

revenues and expenses, which constitute non-GAAP measures, are subject to management allocations. We believe the presentation of

information on a foreign currency adjusted basis is helpful to investors by making it easier to compare our performance in one period to that of

another period without the variability caused by fluctuations in currency exchange rates.

55