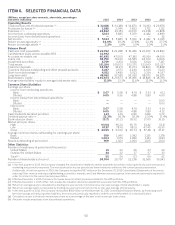

American Express 2015 Annual Report Download - page 56

Download and view the complete annual report

Please find page 56 of the 2015 American Express annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

|

|

Adverse currency fluctuations and foreign exchange controls could decrease earnings we receive from our

international operations and impact our capital.

During 2015, approximately 24 percent of our total revenues net of interest expense were generated from

activities outside the United States. We are exposed to foreign exchange risk from our international operations, and

accordingly the revenue we generate outside the United States is subject to unpredictable fluctuations if the values of

other currencies change relative to the U.S. dollar, which could have a material adverse effect on our results of

operations. For the year ended December 31, 2015, foreign currency movements relative to the U.S. dollar negatively

impacted our net revenues of $32.8 billion by approximately $1.3 billion as the U.S. dollar strengthened against many

currencies over the course of the year.

We may become subject to exchange control regulations that might restrict or prohibit the conversion of other

currencies into U.S. dollars. Political and economic conditions in other countries could also impact the availability of

foreign exchange for the payment by the local card issuer of obligations arising out of local Card Members’ spending

outside such country and for the payment of card bills by Card Members who are billed in a currency other than their

local currency. Substantial and sudden devaluation of local Card Members’ currency can also affect their ability to

make payments to the local issuer of the card in connection with spending outside the local country. The occurrence of

any of these circumstances could further impact our result of operations.

Interest rate increases could materially adversely affect our earnings.

Interest rates have remained at historically low levels for a prolonged period of time and we expect interest rates

to rise in the future. If the rate of interest we pay on our borrowings increases more than the rate of interest we earn on

our loans, our net interest yield, and consequently our net income, could fall. Our interest expense was approximately

$1.6 billion for the year ended December 31, 2015. A hypothetical 1.0 percent increase in interest rates would have

resulted in a decrease to our annual net interest income of approximately $216 million as of December 31, 2015. In

addition, interest rate changes may affect customer behavior, such as impacting the loan balance amounts Card

Members carry on their credit cards or their ability to make payments as higher interest rates lead to higher payment

requirements, further impacting our results of operations.

For a further discussion of our interest rate risk, see “Risk Management — Market Risk Management Process”

under “MD&A.”

The value of our assets or liabilities may be adversely impacted by economic, political or market conditions.

Market risk represents the loss in value of portfolios and financial instruments due to adverse changes in market

variables, which could negatively impact our financial condition. We held approximately $3.8 billion of investment

securities as of December 31, 2015. In the event that actual default rates of these investment securities were to

significantly change from historical patterns due to challenges in the economy or otherwise, it could have a material

adverse impact on the value of our investment portfolio. Defaults or economic disruptions, even in countries or territories

in which we do not have material investment exposure, conduct business or have operations, could adversely affect us.

An inability to accept or maintain deposits due to market demand or regulatory constraints could materially

adversely affect our liquidity position and our ability to fund our business.

As a source of funding, our U.S. bank subsidiaries accept deposits from individuals through third-party brokerage

networks as well as directly from consumers through American Express Personal Savings. As of December 31, 2015,

we had approximately $54.1 billion in total U.S. retail deposits. We face strong competition in the deposit markets,

particularly as to brokerage networks. Aggressive pricing throughout the industry may adversely affect our retention

of existing balances and the cost-efficient acquisition of new deposit funds. If we are required to offer higher interest

rates to attract or maintain deposits, our funding costs will be adversely impacted. Customers could also close their

accounts or reduce balances in favor of products and services offered by competitors for reasons other than price,

including general dissatisfaction with our products or services and concerns over online security or our reputation.

Our ability to obtain deposit funding and offer competitive interest rates on deposits is also dependent on capital

levels of our U.S. bank subsidiaries. The FDIA in certain circumstances prohibits banks, including Centurion Bank and

American Express Bank, from accepting brokered deposits and applies other restrictions, such as a cap on interest

rates we may pay. See “Prompt Corrective Action” under “Regulation and Supervision” for additional information. A

significant amount of our outstanding U.S. retail deposits has been raised through third-party brokerage networks, and

such deposits are considered brokered deposits for bank regulatory purposes.

While Centurion Bank and American Express Bank were considered “well capitalized” as of December 31, 2015 and

had no restrictions regarding acceptance of brokered deposits or setting of interest rates, there can be no assurance

they will continue to meet this definition. The New Capital Rules, when fully phased in, will require bank holding

companies and their bank subsidiaries to maintain substantially more capital, with a greater emphasis on common

45