Charter 2003 Annual Report Download - page 25

Download and view the complete annual report

Please find page 25 of the 2003 Charter annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

|

|

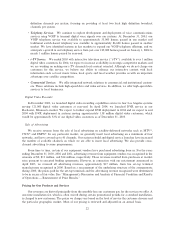

In accordance with the Federal Communications Commission's rules, the prices we charge for cable-

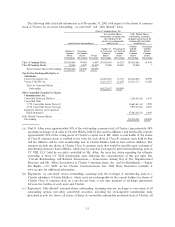

related equipment, such as set-top terminals and remote control devices, and for installation services are based

on actual costs plus a permitted rate of return.

Although our cable service oÅerings vary across the markets we serve because of various factors including

competition and regulatory factors, our services, when oÅered on a stand-alone basis, are typically oÅered at

monthly price ranges, excluding franchise fees and other taxes, as follows:

Price Range as of

Service December 31, 2003

Analog video packages ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ $8.00-$54.00

Premium channel ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ $10.00-$15.00

Pay-per-view (per movie or event)ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ $3.95-$179.00

Digital video packages (including high-speed data service for higher tiers) $34.00-$106.00

High-speed data service ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ $29.99-$39.99

Video on demand (per selection) ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ $0.99-$12.99

High deÑnition television ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ $3.99-$6.99

In addition, from time to time we oÅer free service or reduced-price service during promotional periods in

order to attract new customers. There is no assurance that these customers will remain as customers when the

period of free service expires.

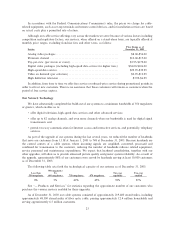

Our Network Technology

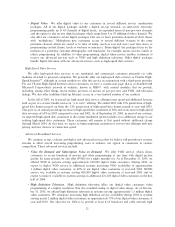

We have substantially completed the build-out of our systems to a minimum bandwidth of 550 megahertz

or greater, which enables us to:

‚ oÅer digital television, high-speed data services and other advanced services;

‚ oÅer up to 82 analog channels, and even more channels when our bandwidth is used for digital signal

transmission; and

‚ permit two-way communication for Internet access and interactive services, and potentially, telephony

services.

As part of the upgrade of our systems during the last several years, we reduced the number of headends

that serve our customers from 1,138 at January 1, 2001 to 748 at December 31, 2003. Because headends are

the control centers of a cable system, where incoming signals are ampliÑed, converted, processed and

combined for transmission to the customer, reducing the number of headends reduces related equipment,

service personnel and maintenance expenditures. We expect that headend consolidation, together with our

other upgrades, will allow us to provide enhanced picture quality and greater system reliability. As a result of

the upgrade, approximately 88% of our customers were served by headends serving at least 10,000 customers

as of December 31, 2003.

The following table sets forth the technological capacity of our systems as of December 31, 2003:

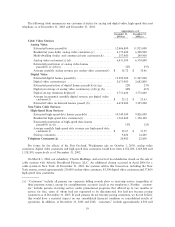

550 megahertz

Less than To Two-way Two-way

550 megahertz 660 megahertz 750 megahertz 870 megahertz capability enabled

8% 5% 42% 45% 92% 87%

See ""Ì Products and Services'' for statistics regarding the approximate number of our customers who

purchase the various services enabled by these upgrades.

As of December 31, 2003 our cable systems consisted of approximately 219,400 strand miles, including

approximately 48,300 strand miles of Ñber optic cable, passing approximately 12.4 million households and

serving approximately 6.5 million customers.

23