Charter 2003 Annual Report Download - page 62

Download and view the complete annual report

Please find page 62 of the 2003 Charter annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

|

|

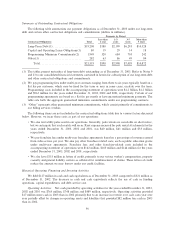

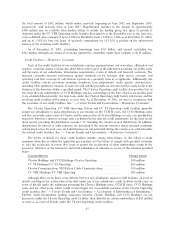

December 31, 2003 Semi-Annual Start Date for

Face Accreted Interest Payment Interest Payment Maturity

Value Value(a) Dates on Discount Notes Date(b)

CCO Holdings, LLC

8∂% senior notes due 2013 ÏÏÏÏ 500 500 5/15&11/15 11/15/13

Renaissance Media Group LLC:

10.000% senior discount notes

due 2008 ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 114 116 4/15&10/15 10/15/03 4/15/08

CC V Holdings, LLC:

11.875% senior discount notes

due 2008 ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 113 113 6/1&12/1 6/1/04 12/1/08

Credit Facilities

Charter OperatingÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 4,459 4,459

CC VI Operating ÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 868 868

Falcon Cable ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 856 856

CC VIII OperatingÏÏÏÏÏÏÏÏÏÏÏÏÏ 1,044 1,044

$19,208 $18,647

(a) The accreted value presented above represents the face value of the notes less the original issue discount

at the time of sale plus the accretion to the balance sheet date.

(b) In general, the obligors have the right to redeem all of the notes set forth (except the Charter Holdings

notes with terms of eight years) in the above tables in whole or part at their option, beginning at various

times prior to their stated maturity dates, subject to certain conditions, upon the payment of the

outstanding principal amount (plus a speciÑed redemption premium) and all accrued and unpaid interest.

We currently have no intention of redeeming any of these notes prior to their stated maturity dates. For

additional information, see Note 9 to our consolidated Ñnancial statements contained herein.

(c) The 5.75% convertible senior notes and the 4.75% convertible senior notes are convertible at the option of

the holders into shares of Class A common stock at a conversion rate of 46.3822 and 38.0952 shares,

respectively, per $1,000 principal amount of notes, which is equivalent to a price of $21.56 and $26.25 per

share, respectively, subject to certain adjustments. SpeciÑcally, the adjustments include anti-dilutive

provisions, which cause adjustments to occur automatically based on the occurrence of speciÑed events to

provide protection rights to holders of the notes. Additionally, the conversion ratio may be adjusted by us

when deemed appropriate.

As of December 31, 2003, we had unused total potential availability of $1.7 billion under our subsidiaries'

credit facilities, although our Ñnancial covenants limited our availability to $828 million at December 31,

2003. Continued access to these credit facilities is subject to our remaining in compliance with the applicable

covenants of these credit facilities.

As of December 31, 2003 and 2002, the weighted average interest rate on our bank debt was

approximately 5.4%, the weighted average interest rate on our high-yield debt was approximately 10.3%, and

the weighted average rate on the convertible debt was approximately 5.5% and 5.3%, respectively, resulting in

a blended weighted average interest rate of 8.2% and 7.9%, respectively. Approximately 80% of our debt

eÅectively bore Ñxed interest rates including the eÅects of our interest rate hedge agreements as of

December 31, 2003 compared to approximately 79% at December 31, 2002. The fair value of our high-yield

debt was $10.6 billion and $4.4 billion at December 31, 2003 and 2002, respectively. The fair value of bank

debt was $6.9 billion and $6.4 billion at December 31, 2003 and 2002, respectively. The fair value of high-yield

debt and bank debt is based on quoted market prices.

60