Charter 2010 Annual Report Download - page 56

Download and view the complete annual report

Please find page 56 of the 2010 Charter annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

|

|

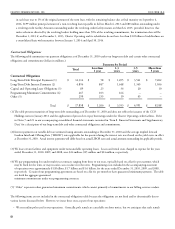

A tax position that meets the more-likely-than-not recognition threshold

is measured to determine the amount of benefit to be recognized

in our financial statements. e tax position is measured at the

largest amount of benefit that has a greater than 50% likelihood

of being realized when the position is ultimately resolved. ere is

considerable judgment involved in determining whether positions

taken on the tax return are “more likely than not” of being sustained.

Charter adjusts its uncertain tax reserve estimates periodically because

of ongoing examinations by, and settlements with, the various

taxing authorities, as well as changes in tax laws, regulations and

interpretations.

No tax years for Charter or Charter Holdco are currently under

examination by the Internal Revenue Service. Tax years ending 2007

through 2010 remain subject to examination and assessment. Years

prior to 2007 remain open solely for purposes of examination of

Charter’s loss and credit carryforwards.

Litigation

Legal contingencies have a high degree of uncertainty. When a loss

from a contingency becomes estimable and probable, a reserve is

established. e reserve reflects management's best estimate of the

probable cost of ultimate resolution of the matter and is revised as

facts and circumstances change. A reserve is released when a matter

is ultimately brought to closure or the statute of limitations lapses.

We have established reserves for certain matters. Although certain

matters are not expected individually to have a material adverse effect

on our consolidated financial condition, results of operations or

liquidity, such matters could have, in the aggregate, a material adverse

effect on our consolidated financial condition, results of operations or

liquidity.

Programming Agreements

We exercise significant judgment in estimating programming expense

associated with certain video programming contracts. Our policy

is to record video programming costs based on our contractual

agreements with our programming vendors, which are generally

multi-year agreements that provide for us to make payments to

the programming vendors at agreed upon market rates based on

the number of customers to which we provide the programming

service. If a programming contract expires prior to the parties' entry

into a new agreement and we continue to distribute the service,

we estimate the programming costs during the period there is no

contract in place. In doing so, we consider the previous contractual

rates, inflation and the status of the negotiations in determining

our estimates. When the programming contract terms are finalized,

an adjustment to programming expense is recorded, if necessary, to

reflect the terms of the new contract. We also make estimates in the

recognition of programming expense related to other items, such as

the accounting for free periods and credits from service interruptions,

as well as the allocation of consideration exchanged between the

parties in multiple-element transactions.

Significant judgment is also involved when we enter into agreements

that result in us receiving cash consideration from the programming

vendor, usually in the form of advertising sales, channel positioning

fees, launch support or marketing support. In these situations,

we must determine based upon facts and circumstances if such

cash consideration should be recorded as revenue, a reduction in

programming expense or a reduction in another expense category

(e.g., marketing).