Charter 2010 Annual Report Download - page 67

Download and view the complete annual report

Please find page 67 of the 2010 Charter annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

|

|

Overview

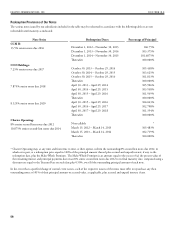

As of December 31, 2010 and 2009, the blended weighted average

interest rate on our debt was 6.7% and 5.5%, respectively. e

interest rate on approximately 65% and 37% of the total principal

amount of our debt was effectively fixed, including the effects of

our interest rate hedge agreements, if any, as of December 31, 2010

and 2009, respectively. e fair value of our high-yield notes was

$6.6 billion and $5.4 billion at December 31, 2010 and 2009,

respectively. e fair value of our credit facilities was $6.3 billion

and $8.0 billion at December 31, 2010 and 2009, respectively. e

fair value of our high-yield notes and credit facilities were based on

quoted market prices.

e following description is a summary of certain provisions of

our credit facilities and our notes (the “Debt Agreements”). e

summary does not restate the terms of the Debt Agreements in their

entirety, nor does it describe all terms of the Debt Agreements. e

agreements and instruments governing each of the Debt Agreements

are complicated and you should consult such agreements and

instruments for more detailed information regarding the Debt

Agreements.

CCO Holdings Credit Facility

In March 2007, CCO Holdings entered into a credit agreement

(the “CCO Holdings credit facility”) which consists of a $350

million term loan facility. e facility matures in September 2014.

Borrowings under the CCO Holdings credit facility bear interest at

a variable interest rate based on either LIBOR or a base rate plus, in

either case, an applicable margin. e applicable margin for LIBOR

term loans is 2.50% above LIBOR. If an event of default were to

occur, CCO Holdings would not be able to elect LIBOR and would

have to pay interest at the base rate plus the applicable margin. e

CCO Holdings credit facility is secured by the equity interests of

Charter Operating, and all proceeds thereof.

Charter Operating Credit Facilities

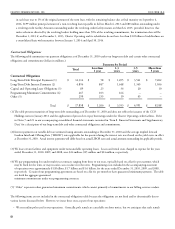

e Charter Operating credit facilities have an outstanding principal

amount of $6.0 billion at December 31, 2010 as follows:

A term B-1 loan with a remaining principal amount of

approximately $2.4 billion, which is repayable in equal quarterly

•

installments and aggregating $25 million in each loan year, with

the remaining balance due at final maturity on March 6, 2014;

A term B-2 loan with a remaining principal amount of

approximately $307 million, which is repayable in equal

quarterly installments and aggregating $3 million in each loan

year, with the remaining balance due at final maturity on March

6, 2014;

A term C loan with a remaining principal amount of approximately

$3.0 billion, which is repayable in equal quarterly installments

and aggregating $30 million in each loan year, with the

remaining balance due at final maturity on September 6, 2016;

A non-revolving loan with a remaining principal amount of

approximately $199 million repayable in full on March 6, 2013;

and

A revolving loan with an outstanding balance of $80 million at

December 31, 2010 and allowing for borrowings of up to $1.3 billion.

e revolving loan matures in March 2015. However, if on

December 1, 2013 Charter Operating has scheduled maturities in

excess of $1.0 billion between January 1, 2014 and April 30, 2014,

the revolving loan will mature on December 1, 2013 unless lenders

holding more than 50% of the revolving loan consent to the maturity

being March 2015. As of January 31, 2011, Charter Operating had

maturities of $1.3 billion between January 1, 2014 and April 30,

2014. e revolving credit facility amount may be increased, but it

may not exceed $1.75 billion in aggregate revolving commitments

plus the amount outstanding under the non-revolving loan.

Amounts outstanding under the Charter Operating credit facilities

bear interest, at Charter Operating’s election, at a base rate or

LIBOR, as defined, plus a margin. e applicable LIBOR margin for

the non-revolving loans and the term B-1 loans is 2%. e LIBOR

term B-2 loan bears interest at LIBOR plus 5.0%, with a LIBOR floor

of 3.5%, or at Charter Operating’s election, a base rate plus a margin

of 4.00%. Charter Operating has currently elected to pay based on

the base rate. e applicable margin for the term C loans is currently

3.25% in the case of LIBOR loans, provided that if certain other

term loans are borrowed or certain extended loans are established,

then the term C loans shall automatically increase to the extent

necessary to cause the yield for the term C loans to be 25 basis points

•

•

•

•