Charter 2010 Annual Report Download - page 98

Download and view the complete annual report

Please find page 98 of the 2010 Charter annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

|

|

F- F-PB

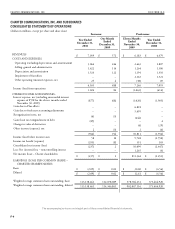

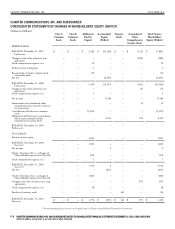

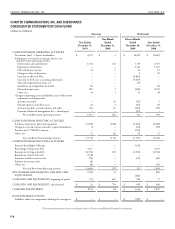

CHARTER COMMUNICATIONS, INC. AND SUBSIDIARIES NOTES TO CONSOLIDATED FINANCIAL STATEMENTS DECEMBER 31, 2010, 2009, AND 2008

(dollars in millions, except share or per share data or where indicated)

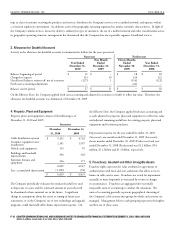

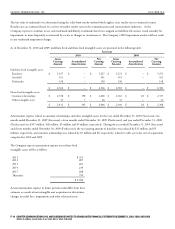

e Company recorded non-cash franchise impairment charges of $2.2

billion and $1.5 billion for the eleven months ended November 30,

2009 (Predecessor) and year ended December 31, 2008 (Predecessor),

respectively. e impairment charges recorded in 2009 and 2008

were primarily the result of the impact of the economic downturn

along with increased competition. e Company’s 2010 impairment

analyses did not result in any franchise impairment charges.

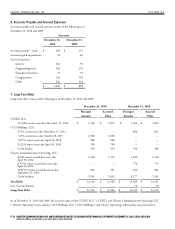

On the Effective Date, the Company applied fresh start accounting

and adjusted its franchise, goodwill, and other intangible assets

including trademarks and customer relationships to reflect fair value.

e Company’s valuations, which are based on the present value of

projected after tax cash flows, resulted in a value for property, plant

and equipment, franchises, and customer relationships for each unit

of accounting. As a result of applying fresh start accounting, the

Company recorded goodwill of $951 million which represents the

excess of reorganization value over amounts assigned to the other assets.

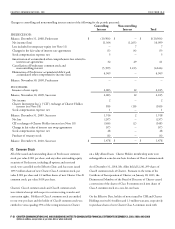

Franchises, for valuation purposes, are defined as the future economic

benefits of the right to solicit and service potential customers

(customer marketing rights), and the right to deploy and market

new services, such as Internet and telephone, to potential customers

(service marketing rights). Fair value is determined based on

estimated discrete discounted future cash flows using assumptions

consistent with internal forecasts. e franchise after-tax cash flow

is calculated as the after-tax cash flow generated by the potential

customers obtained (less the anticipated customer churn), and the

new services added to those customers in future periods. e sum

of the present value of the franchises' after-tax cash flow in years

1 through 10 and the continuing value of the after-tax cash flow

beyond year 10 yields the fair value of the franchises.

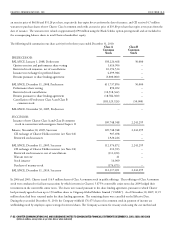

e Company determined the estimated fair value of each unit

of accounting utilizing an income approach model based on the

present value of the estimated discrete future cash flows attributable

to each of the intangible assets identified for each unit assuming

a discount rate. is approach makes use of unobservable factors

such as projected revenues, expenses, capital expenditures, and a

discount rate applied to the estimated cash flows. e determination

of the discount rate was based on a weighted average cost of capital

approach, which uses a market participant’s cost of equity and after-

tax cost of debt and reflects the risks inherent in the cash flows.

e Company estimated discounted future cash flows using

reasonable and appropriate assumptions including among others,

penetration rates for basic and digital video, high-speed Internet,

and telephone; revenue growth rates; operating margins; and

capital expenditures. e assumptions are derived based on the

Company’s and its peers’ historical operating performance adjusted

for current and expected competitive and economic factors

surrounding the cable industry. e estimates and assumptions made

in the Company’s valuations are inherently subject to significant

uncertainties, many of which are beyond its control, and there is no

assurance that these results can be achieved. e primary assumptions

for which there is a reasonable possibility of the occurrence of a

variation that would significantly affect the measurement value

include the assumptions regarding revenue growth, programming

expense growth rates, the amount and timing of capital expenditures

and the discount rate utilized.

Goodwill is tested for impairment as of November 30 of each year, or

more frequently as warranted by events or changes in circumstances.

e first step involves a comparison of the estimated fair value of

each of our reporting units to its carrying amount. If the estimated

fair value of a reporting unit exceeds its carrying amount, goodwill of

the reporting unit is not considered impaired and the second step of

the goodwill impairment is not necessary. If the carrying amount of a

reporting unit exceeds its estimated fair value, then the second step of

the goodwill impairment test must be performed, and a comparison

of the implied fair value of the reporting unit’s goodwill is compared

to its carrying amount to determine the amount of impairment, if any.

Reporting units are consistent with the units of accounting used for

franchise impairment testing. Likewise the fair values of the reporting

units are determined using a consistent income approach model as that

used for franchise impairment testing. e Company’s 2010 impairment

analyses did not result in any goodwill impairment charges.

Customer relationships, for valuation purposes, represent the value of

the business relationship with existing customers (less the anticipated

customer churn), and are calculated by projecting the discrete

future after-tax cash flows from these customers, including the right

to deploy and market additional services to these customers. e

present value of these after-tax cash flows yields the fair value of the

customer relationships. Customer relationships are amortized on

an accelerated method over useful lives of 11-15 years based on the

period over which current customers are expected to generate cash

flows. Customer relationships are evaluated upon the occurrence

of events or changes in circumstances indicating that the carrying

amount of an asset may not be recoverable.