Charter 2010 Annual Report Download - page 62

Download and view the complete annual report

Please find page 62 of the 2010 Charter annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

|

|

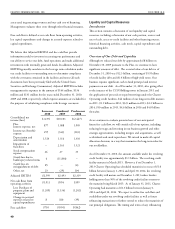

assets used in generating revenues and our cash cost of financing.

Management evaluates these costs through other financial measures.

Free cash flow is defined as net cash flows from operating activities,

less capital expenditures and changes in accrued expenses related to

capital expenditures.

We believe that Adjusted EBITDA and free cash flow provide

information useful to investors in assessing our performance and

our ability to service our debt, fund operations and make additional

investments with internally generated funds. In addition, Adjusted

EBITDA generally correlates to the leverage ratio calculation under

our credit facilities or outstanding notes to determine compliance

with the covenants contained in the facilities and notes (all such

documents have been previously filed with the United States

Securities and Exchange Commission). Adjusted EBITDA includes

management fee expenses in the amount of $144 million, $136

million and $131 million for the years ended December 31, 2010,

2009 and 2008, respectively, which expense amounts are excluded for

the purposes of calculating compliance with leverage covenants.

Successor

2010 Combined

2009 Predecessor

2008

Consolidated net

income (loss) $ (237) $10,101 $(2,447)

Plus:

Interest expense, net 877 1,088 1,905

Income tax (benefit)

expense 295 (343) (103)

Depreciation and

amortization 1,524 1,316 1,310

Impairment of

franchises -- 2,163 1,521

Stock compensation

expense 26 27 33

(Gain) loss due to

bankruptcy related items 6 (11,830) --

(Gain) loss on

extinguishment of debt 85 -- (4)

Other, net 23 (29) 104

Adjusted EBITDA $2,599 $2,493 $2,319

Net cash flows from

operating activities $1,911 $594 $399

Less: Purchases of

property, plant and

equipment (1,209) (1,134) (1,202)

Change in accrued

expenses related to

capital expenditures 8 (10) (39)

Free cash flow $710 $(550) $(842)

Introduction

is section contains a discussion of our liquidity and capital

resources, including a discussion of our cash position, sources and

uses of cash, access to credit facilities and other financing sources,

historical financing activities, cash needs, capital expenditures and

outstanding debt.

Overview of Our Debt and Liquidity

Although we reduced our debt by approximately $8 billion on

November 30, 2009 pursuant to the Plan, we continue to have

significant amounts of debt. e accreted value of our debt as of

December 31, 2010 was $12.3 billion, consisting of $5.9 billion

of credit facility debt and $6.4 billion of high-yield notes. Our

business requires significant cash to fund principal and interest

payments on our debt. As of December 31, 2010, after giving effect

to the issuance of the CCO Holdings notes in January 2011 and

the application of proceeds to repay borrowings under the Charter

Operating credit facilities, $44 million of our long-term debt matures

in 2011, $1.1 billion in 2012, $323 million in 2013, $2.2 billion in

2014, $30 million in 2015, $4.6 billion in 2016 and $4.0 billion

thereafter.

As we continue to evaluate potential uses of our anticipated

future free cash flow, we will consider all of our options, including

reducing leverage and investing in our business growth and other

strategic opportunities, including mergers and acquisitions, as well

as dividends and stock repurchases. We intend to make all capital

allocation decisions in a way that maximizes the long-term value for

our stockholders.

As of December 31, 2010, the amount available under the revolving

credit facility was approximately $1.1 billion. e revolving credit

facility matures in March 2015. However, if on December 1,

2013 Charter Operating has scheduled maturities in excess of $1.0

billion between January 1, 2014 and April 30, 2014, the revolving

credit facility will mature on December 1, 2013 unless lenders

holding more than 50% of the revolving credit facility consent to

the maturity being March 2015. As of January 31, 2011, Charter

Operating had maturities of $1.3 billion between January 1,

2014 and April 30, 2014. We expect to utilize free cash flow and

availability under our revolving credit facilities as well as future

refinancing transactions to further extend or reduce the maturities of

our principal obligations. e timing and terms of any refinancing