Coca Cola 2008 Annual Report Download - page 108

Download and view the complete annual report

Please find page 108 of the 2008 Coca Cola annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

|

|

THE COCA-COLA COMPANY AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

NOTE 11: HEDGING TRANSACTIONS AND DERIVATIVE FINANCIAL INSTRUMENTS (Continued)

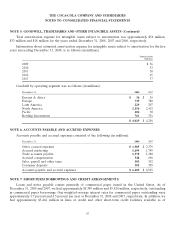

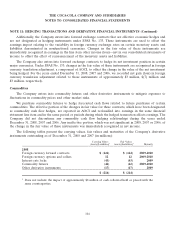

The following table summarizes activity in AOCI related to derivatives designated as cash flow hedges held

by the Company during the applicable periods (in millions):

Before-Tax Income After-Tax

Amount Tax Amount

2008

Accumulated derivative net gains (losses) as of January 1, 2008 $ (112) $ 43 $ (69)

Net changes in fair value of derivatives (62) 23 (39)

Net reclassification from AOCI into earnings 53 (20) 33

Accumulated derivative net gains (losses) as of December 31, 2008 $ (121) $ 46 $ (75)

Before-Tax Income After-Tax

Amount Tax Amount

2007

Accumulated derivative net gains (losses) as of January 1, 2007 $ (16) $ 6 $ (10)

Net changes in fair value of derivatives (158) 61 (97)

Net reclassification from AOCI into earnings 62 (24) 38

Accumulated derivative net gains (losses) as of December 31, 2007 $ (112) $ 43 $ (69)

Before-Tax Income After-Tax

Amount Tax Amount

2006

Accumulated derivative net gains (losses) as of January 1, 2006 $ 35 $ (14) $ 21

Net changes in fair value of derivatives (38) 15 (23)

Net reclassification from AOCI into earnings (13) 5 (8)

Accumulated derivative net gains (losses) as of December 31, 2006 $ (16) $ 6 $ (10)

NOTE 12: FAIR VALUE MEASUREMENTS

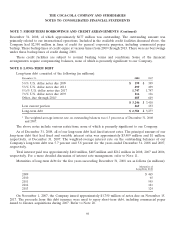

Effective January 1, 2008, the Company adopted SFAS No. 157, which defines fair value as the exchange

price that would be received for an asset or paid to transfer a liability (an exit price) in the principal or most

advantageous market for the asset or liability in an orderly transaction between market participants at the

measurement date. FSP FAS 157-2 delayed the effective date for all nonfinancial assets and liabilities until

January 1, 2009, except those that are recognized or disclosed at fair value in the financial statements on a

recurring basis. SFAS No. 157 establishes a three-level fair value hierarchy that prioritizes the inputs used to

measure fair value. This hierarchy requires entities to maximize the use of observable inputs and minimize the

use of unobservable inputs. The three levels of inputs used to measure fair value are as follows:

• Level 1 — Quoted prices in active markets for identical assets or liabilities.

• Level 2 — Observable inputs other than quoted prices included in level 1, such as quoted prices for

similar assets and liabilities in active markets; quoted prices for identical or similar assets and liabilities in

markets that are not active; or other inputs that are observable or can be corroborated by observable

market data.

106