Coca Cola 2008 Annual Report Download - page 88

Download and view the complete annual report

Please find page 88 of the 2008 Coca Cola annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

|

|

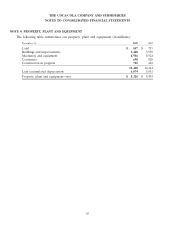

THE COCA-COLA COMPANY AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

NOTE 1: BUSINESS AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

SFAS No. 160 clarifies that a noncontrolling interest in a subsidiary should be accounted for as a component of

equity separate from the parent’s equity, rather than in liabilities or the mezzanine section between liabilities

and equity. In addition, SFAS No. 160 establishes disclosure requirements that clearly identify and distinguish

between the controlling and noncontrolling interests and require the separate disclosure of income attributable

to controlling and noncontrolling interests. SFAS No. 160 is effective for fiscal years beginning after

December 15, 2008. Other than the reclassification of noncontrolling interests as described above, the Company

does not anticipate that the adoption of SFAS No. 160 will have a material impact on our consolidated financial

statements.

In December 2007, the FASB ratified Emerging Issues Task Force (‘‘EITF’’) Issue No. 07-1, ‘‘Accounting for

Collaborative Arrangements.’’ EITF 07-1 defines collaborative arrangements and establishes reporting

requirements for transactions between participants in a collaborative arrangement and between participants in

the arrangement and third parties. It also establishes the appropriate income statement presentation and

classification for joint operating activities and payments between participants, as well as the sufficiency of the

disclosures related to these arrangements. EITF 07-1 is effective for fiscal years beginning after December 15,

2008. The Company does not expect the adoption of EITF 07-1 to have a material impact on our consolidated

financial statements.

In February 2007, the FASB issued SFAS No. 159, ‘‘The Fair Value Option for Financial Assets and

Financial Liabilities—Including an amendment of FASB Statement No. 115.’’ SFAS No. 159 permits entities to

choose to measure many financial instruments and certain other items at fair value. Unrealized gains and losses

on items for which the fair value option has been elected will be recognized in earnings at each subsequent

reporting date. SFAS No. 159 was effective for our Company on January 1, 2008. The adoption of SFAS No. 159

did not have a material impact on our consolidated financial statements.

In September 2006, the SEC staff published SAB No. 108, ‘‘Considering the Effects of Prior Year

Misstatements when Quantifying Misstatements in Current Year Financial Statements.’’ SAB No. 108 addresses

quantifying the financial statement effects of misstatements, specifically, how the effects of prior year

uncorrected errors must be considered in quantifying misstatements in the current year financial statements.

SAB No. 108 was effective for fiscal years ending after November 15, 2006. The adoption of SAB No. 108 by our

Company in the fourth quarter of 2006 did not have a material impact on our consolidated financial statements.

As previously discussed, our Company adopted SFAS No. 158 related to defined benefit pension and other

postretirement plans. Refer to Note 16.

In September 2006, the FASB issued SFAS No. 157, ‘‘Fair Value Measurements.’’ SFAS No. 157 defines fair

value, establishes a framework for measuring fair value and expands disclosure requirements about fair value

measurements. SFAS No. 157 was effective for our Company on January 1, 2008. However, in February 2008, the

FASB released a FASB Staff Position (FSP FAS 157-2—Effective Date of FASB Statement No. 157) which

delayed the effective date of SFAS No. 157 for all nonfinancial assets and nonfinancial liabilities, except those

that are recognized or disclosed at fair value in the financial statements on a recurring basis (at least annually).

The adoption of SFAS No. 157 for our financial assets and liabilities did not have a material impact upon

adoption. We do not believe the adoption of SFAS No. 157 for our nonfinancial assets and liabilities, effective

January 1, 2009, will have a material impact on our consolidated financial statements.

In July 2006, the FASB issued Interpretation No. 48 which clarifies the accounting for uncertainty in income

taxes recognized in an enterprise’s financial statements in accordance with SFAS No. 109, ‘‘Accounting for

86