Coca Cola 2008 Annual Report Download - page 93

Download and view the complete annual report

Please find page 93 of the 2008 Coca Cola annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

|

|

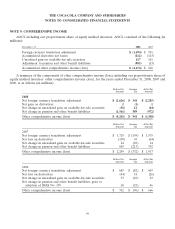

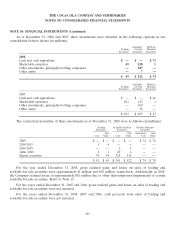

THE COCA-COLA COMPANY AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

NOTE 3: BOTTLING INVESTMENTS (Continued)

concentrate to fully recover the capitalized costs plus a return on the Company’s investment. Should CCE fail to

purchase the specified numbers of cold-drink equipment for any calendar year through 2010, the parties agreed

to mutually develop a reasonable solution. Should no mutually agreeable solution be developed, or in the event

that CCE otherwise breaches any material obligation under the contracts and such breach is not remedied within

a stated period, then CCE would be required to repay a portion of the support funding as determined by our

Company. In the third quarter of 2004, our Company and CCE agreed to amend the contract to defer the

placement of some equipment from 2004 and 2005, as previously agreed under the original contract, to 2009 and

2010. In connection with this amendment, CCE agreed to pay the Company approximately $2 million in 2004,

$3 million annually in 2005 through 2008, and $1 million in 2009. In 2005, our Company and CCE agreed to

amend the contract for North America to move to a system of purchase and placement credits, whereby CCE

earns credit toward its annual purchase and placement requirements based upon the type of equipment it

purchases and places. The amended contract also provides that no breach by CCE will occur even if it does not

achieve the required number of purchase and placement credits in any given year, so long as (1) the shortfall

does not exceed 20 percent of the required purchase and placement credits for that year; (2) a compensating

payment is made to our Company by CCE; (3) the shortfall is corrected in the following year; and (4) CCE

meets all specified purchase and placement credit requirements by the end of 2010. The payments we made to

CCE under these programs are recorded in prepaid expenses and other assets and in noncurrent other assets

and amortized as deductions from revenues over the 10-year period following the placement of the equipment.

The amortizable carrying values for these infrastructure programs with CCE were approximately $388 million

and $494 million as of December 31, 2008 and 2007, respectively. The Company has no further commitments

under these programs.

On January 1, 2008, CCE adopted the measurement provisions of SFAS No. 158, which require entities to

measure the funded status of retirement benefit plans as of their fiscal year end. SFAS No. 158 requires a

cumulative adjustment to be made to the beginning balance of retained earnings in the period of adoption. We

reduced the beginning balance of our retained earnings and our investment basis in CCE by approximately

$8 million for our proportionate share of CCE’s adjustment. Refer to Note 9 and Note 16.

Effective December 31, 2006, CCE adopted all of the requirements of SFAS No. 158, with the exception of

the measurement provisions. Our proportionate share of the impact of CCE’s adoption of SFAS No. 158 was an

approximate $132 million pretax ($84 million after-tax) reduction in both the carrying value of our investment in

CCE and our AOCI. Refer to Note 9 and Note 16.

If valued at the December 31, 2008 quoted closing price of CCE shares, the fair value of our investment in

CCE would have exceeded our carrying value by approximately $2.0 billion.

Other Equity Method Investments

Our other equity method investments include our ownership interests in Coca-Cola Hellenic, Coca-Cola

FEMSA and Coca-Cola Amatil. As of December 31, 2008, we owned approximately 23 percent, 32 percent and

30 percent, respectively, of these companies’ common shares.

Operating results include our proportionate share of income (loss) from our equity method investments. As

of December 31, 2008, our investment in our equity method investees in the aggregate, other than CCE,

exceeded our proportionate share of the net assets of these equity method investees by approximately

$984 million. This difference is not amortized.

91