Lowe's 2012 Annual Report Download - page 29

Download and view the complete annual report

Please find page 29 of the 2012 Lowe's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

|

|

15

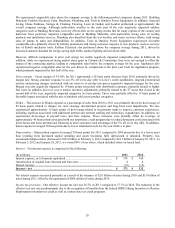

As we redefine our business to become more seamless and simple, we must also continue to protect retail relevance. In

2012, our focus was on two key initiatives: Value Improvement and Product Differentiation. Value Improvement is

designed to enhance our ability to offer compelling products and value while Product Differentiation is designed to help us

drive excitement and flexibility in our stores by highlighting innovative products through better display techniques. These

strategic initiatives build on Lowe’s core strengths and are expected to deliver comparable transaction growth, better gross

margins, and greater inventory productivity by localizing assortments and driving excitement in our stores.

Value Improvement enhances our ability to offer compelling products and value by having the right product, at the right

quantity, at the right place, at the right time. In 2012, we leveraged our Integrated Planning and Execution tool to create

clusters of stores, based on specific differences and customer buying preferences, which enhanced the assortment strategy

that was used to guide the line review process. For each cluster, the product assortments were designed to reduce

duplication of features and functions within price points to improve the customer experience. We are also working to

reduce unit costs by negotiating lower first costs from vendors by eliminating funds set aside for promotional and

marketing support. The result is a more localized assortment of products and simpler price point progression within the

category. As SKUs are rationalized, the teams are reinvesting the inventory dollars in greater depth of high volume SKUs.

In addition, we are increasing our in-stock targets for these new lines to ensure items are available when needed by

customers. By the end of 2012, we completed product line reviews and product line resets of approximately 80% and 30%

of our business, respectively.

Through our Product Differentiation initiative, we revised many of our end-cap locations to highlight innovative products,

significant values, or to showcase specific private or national brands. In addition, we redesigned promotional spaces to

better promote seasonally relevant, high value items to drive sales and to provide more open sight lines to navigate and

shop at our stores. During 2012, our product differentiation resets were rolled out to approximately 1,250 stores, and we

expect to roll the resets out to an additional 160 stores in 2013.

In conjunction with our progress on Value Improvement and Product Differentiation, in 2012 we also initiated sales

training programs for store and contact center employees to further develop our sales culture and pave the way for the next

phase of our transformation.

Where we go from here – 2013 and beyond

While the housing market is slowly improving, consumers are still coping with the lingering effects of the recession as

mortgage delinquency rates remain at historic highs. While we are optimistic about a housing recovery and near-term

personal consumption expenditures are expected to grow faster than personal income, employment and income are

expected to continue to grow slowly. Consumers will need to continue to prioritize how and where they spend their

discretionary income and therefore our outlook for 2013 assumes modest growth in the home improvement market.

However we have confidence in our vision and have laid the foundation to continue improving our core business as we

move into fiscal year 2013.

In 2013, our Value Improvement initiative will remain the primary focus of the organization. As we improve our product

offerings by localizing assortments we expect to drive improved close rates. We also have an opportunity to improve close

rates through additional labor in our stores. We expect to add approximately 150 hours per store per week to the staffing

model for nearly two-thirds of our stores to help reduce the gap between our weekend versus weekday close rate. Our goal

is to better serve customers and close more sales during peak weekday hours by increasing assistance available in the

aisles. We believe the increased labor hours and higher in-stock service levels will help us further capitalize on traffic

during the week which will result in an improvement in close rates.

In 2013 and beyond, we will further develop our flexible fulfillment capability by deploying Central Dispatch (CDO) and

Central Production Offices (CPO). The CDO will allow for centralized delivery scheduling and better route planning,

resulting in lower fuel cost, greater fleet utilization, and more productive overall delivery. The CPO will provide

operational efficiencies through the consolidation of labor. Today each store has its own installed sales office, whereas, in

the future, that labor will be consolidated into our contact centers resulting in a significant reduction of labor hours. The

customer’s experience will be enhanced through better coordination and consistency.