Lowe's 2012 Annual Report Download - page 57

Download and view the complete annual report

Please find page 57 of the 2012 Lowe's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

|

|

43

The remaining seven operating locations that experienced a triggering event during 2012 were determined to be

recoverable and therefore were not impaired. For these seven locations, the expected undiscounted cash flows substantially

exceeded the net book value of the location’s assets. A 10% reduction in projected sales used to estimate future cash flows

at the latest date these seven operating locations were evaluated for impairment would have resulted in the impairment of

four of these locations and increased recognized impairment losses by $47 million. We analyzed other assumptions made

in estimating the future cash flows of the operating locations evaluated for impairment, but the sensitivity of those

assumptions was not significant to the estimates.

In the determination of impairment for locations identified for closure and for excess properties held-for-use and held-for-

sale, which consisted of retail outparcels and property associated with relocated or closed locations, the fair values were

determined using a market approach based on estimated selling prices. The Company determined the estimated selling

prices by obtaining information from property brokers or appraisers in the specific markets being evaluated or negotiated

non-binding offers to purchase. The information obtained from property brokers or appraisers included comparable sales

of similar assets and assumptions about demand in the market for these assets.

During 2012, the Company incurred total impairment charges of $21 million for 22 excess property locations. A 10%

reduction in the estimated selling prices for these excess properties at the dates the locations were evaluated for impairment

would have increased impairment losses by approximately $4 million.

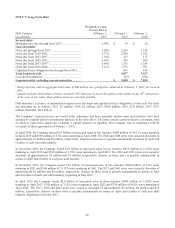

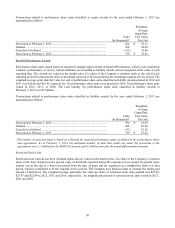

The following tables present the Company’s non-financial assets measured at estimated fair value on a nonrecurring basis

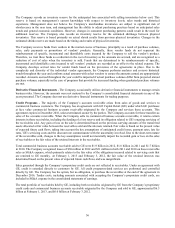

and the resulting long-lived asset impairment losses included in earnings, excluding costs to sell for excess properties held-

for-sale. Because assets subject to long-lived asset impairment were not measured at fair value on a recurring basis, certain

fair value measurements presented in the table may reflect values at earlier measurement dates and may no longer represent

the fair values at February 1, 2013 and February 3, 2012.

Fair Value Measurements - Nonrecurring Basis

February 1, 2013 February 3, 2012

(In millions)

Fair Value

Measurements

Impairment

Losses

Fair Value

Measurements

Impairment

Losses

Assets held-for-use:

Operating locations ............................................... $ 19 $ (55) $ 16 $ (40)

Locations identified for closure ............................. - - 72 (269)

Excess properties ................................................... 33 (17) 117 (78)

Assets held-for-sale:

Excess properties ................................................... 8 (4) 2 (1)

Total ......................................................................... $ 60 $ (76) $ 207 $ (388)

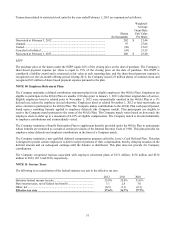

Fair Value of Financial Instruments

The Company’s financial instruments not measured at fair value on a recurring basis include cash and cash equivalents,

accounts receivable, accounts payable, accrued liabilities and long-term debt and are reflected in the financial statements at

cost. With the exception of long-term debt, cost approximates fair value for these items due to their short-term nature. The

fair values of the Company’s unsecured notes classified as Level 1 were estimated using quoted market prices. The fair

values of the Company’s mortgage notes classified as Level 2 were estimated using discounted cash flow analyses, based

on the future cash outflows associated with these arrangements and discounted using the applicable risk-free borrowing

rate.

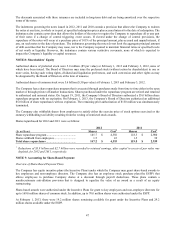

Carrying amounts and the related estimated fair value of the Company’s long-term debt, excluding capitalized lease

obligations, are as follows:

February 1, 2013 February 3, 2012

(In millions)

Carrying

Amoun

t

Fai

r

Value

Carrying

Amount

Fai

r

Value

Unsecured notes (Level 1) ............................................................... 8,627 9,860 7,189 8,250

Mortgage notes (Level 2) ................................................................. 19 22 20 24

Long-term debt (excluding capitalized lease obligations) .......... $ 8,646 $ 9,882 $ 7,209 $ 8,274