Lowe's 2012 Annual Report Download - page 40

Download and view the complete annual report

Please find page 40 of the 2012 Lowe's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

|

|

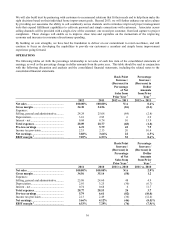

26

We have not made any material changes in the methodology used to estimate the expected future cash flows of closed

locations under operating leases during the past three fiscal years. If the actual results are not consistent with the

assumptions and judgments we have made in estimating expected future cash flows, our store closing lease obligation

losses could vary positively or negatively from our estimated losses. A 10% change in the store closing lease liability

would have affected net earnings by approximately $5 million for 2012.

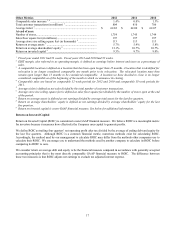

Self-Insurance

Description

We are self-insured for certain losses relating to workers’ compensation; automobile; general and product liability;

extended protection plan; and certain medical and dental claims. Our self-insured retention or deductible, as applicable, is

limited to $2 million per occurrence involving workers’ compensation and $3 million per occurrence involving automobile,

general or product liability. Additionally, a corridor retention of $2 million per occurrence applies to commercial general

liability and product liability claims, subject to a $6 million maximum over a three-year period. We do not have any stop

loss limits for self-insured extended protection plan or medical and dental claims. Self-insurance claims filed and claims

incurred but not reported are accrued based upon our estimates of the discounted ultimate cost for self-insured claims

incurred using actuarial assumptions followed in the insurance industry and historical experience. During 2012, our self-

insurance liability increased approximately $35 million to $899 million as of February 1, 2013. During 2012, we reduced

the discount rate applied to self-insurance claims by 100 basis points, which resulted in a $20 million unfavorable impact to

net earnings.

Judgments and uncertainties involved in the estimate

These estimates are subject to changes in the regulatory environment; utilized discount rate; projected exposures including

payroll, sales and vehicle units; as well as the frequency, lag and severity of claims.

Effect if actual results differ from assumptions

We have not made any material changes in the methodology used to establish our self-insurance liability during the past

three fiscal years. Although we believe that we have the ability to reasonably estimate losses related to claims, it is possible

that actual results could differ from recorded self-insurance liabilities. A 10% change in our self-insurance liability would

have affected net earnings by approximately $56 million for 2012. A 100 basis point change in our discount rate would

have affected net earnings by approximately $23 million for 2012.

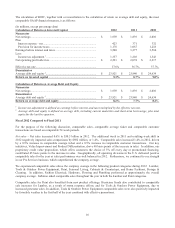

Revenue Recognition

Description

See Note 1 to the consolidated financial statements for a discussion of our revenue recognition policies. The following

accounting estimates relating to revenue recognition require management to make assumptions and apply judgment

regarding the effects of future events that cannot be determined with certainty.

We sell separately-priced extended protection plan contracts under a Lowe’s-branded program for which the Company is

ultimately self-insured. The Company recognizes revenues from extended protection plan sales on a straight-line basis over

the respective contract term. Extended protection plan contract terms primarily range from one to four years from the date

of purchase or the end of the manufacturer’s warranty, as applicable. The Company consistently groups and evaluates

extended protection plan contracts based on the characteristics of the underlying products and the coverage provided in

order to monitor for expected losses. A loss on the overall contract would be recognized if the expected costs of performing

services under the contracts exceeded the amount of unamortized acquisition costs and related deferred revenue associated

with the contracts. Deferred revenues associated with the extended protection plan contracts increased $11 million to $715

million as of February 1, 2013.

We defer revenue and cost of sales associated with settled transactions for which customers have not yet taken possession

of merchandise or for which installation has not yet been completed. Revenue is deferred based on the actual amounts

received. We use historical gross margin rates to estimate the adjustment to cost of sales for these transactions. During

2012, deferred revenues associated with these transactions increased $11 million to $441 million as of February 1, 2013.

Judgments and uncertainties involved in the estimate

For extended protection plans, there is judgment inherent in our evaluation of expected losses as a result of our

methodology for grouping and evaluating extended protection plan contracts and from the actuarial determination of the

estimated cost of the contracts. There is also judgment inherent in our determination of the recognition pattern of costs of

performing services under these contracts.