Microsoft 2014 Annual Report Download - page 36

Download and view the complete annual report

Please find page 36 of the 2014 Microsoft annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

|

|

35

Should we require more capital in the U.S. than is generated by our operations domestically, for example to fund

significant discretionary activities, such as business acquisitions and share repurchases, we could elect to repatriate

future earnings from foreign jurisdictions or raise capital in the U.S. through debt or equity issuances. These alternatives

could result in higher effective tax rates, increased interest expense, or dilution of our earnings. We have borrowed funds

domestically and continue to believe we have the ability to do so at reasonable interest rates.

RECENT ACCOUNTING GUIDANCE

Recently Adopted Accounting Guidance

In December 2011, the Financial Accounting Standards Board (“FASB”) issued guidance enhancing disclosure

requirements about the nature of an entity’s right to offset and related arrangements associated with its financial

instruments. The new guidance requires the disclosure of the gross amounts subject to rights of set-off, amounts offset in

accordance with the accounting standards followed, and the related net exposure. In January 2013, the FASB clarified

that the scope of this guidance applies to derivatives, repurchase agreements, and securities lending arrangements that

are either offset or subject to an enforceable master netting arrangement, or similar agreements. We adopted this new

guidance beginning July 1, 2013. Adoption of this new guidance resulted only in changes to the presentation of

Note 5 – Derivatives of the Notes to Financial Statements.

In February 2013, the FASB issued guidance on disclosure requirements for items reclassified out of AOCI. This new

guidance requires entities to present (either on the face of the income statement or in the notes to financial statements)

the effects on the line items of the income statement for amounts reclassified out of AOCI. We adopted this new guidance

beginning July 1, 2013. Adoption of this new guidance resulted only in changes to the presentation of

Note 19 – Accumulated Other Comprehensive Income of the Notes to Financial Statements.

Recent Accounting Guidance Not Yet Adopted

In March 2013, the FASB issued guidance on a parent’s accounting for the cumulative translation adjustment upon

derecognition of a subsidiary or group of assets within a foreign entity. This new guidance requires that the parent release

any related cumulative translation adjustment into net income only if the sale or transfer results in the complete or

substantially complete liquidation of the foreign entity in which the subsidiary or group of assets had resided. The new

guidance will be effective for us beginning July 1, 2014. We do not anticipate material impacts on our consolidated

financial statements upon adoption.

In May 2014, as part of its ongoing efforts to assist in the convergence of U.S. GAAP and International Financial

Reporting Standards, the FASB issued a new standard related to revenue recognition. Under the new standard,

recognition of revenue occurs when a customer obtains control of promised goods or services in an amount that reflects

the consideration to which the entity expects to receive in exchange for those goods or services. In addition, the standard

requires disclosure of the nature, amount, timing, and uncertainty of revenue and cash flows arising from contracts with

customers. The new standard will be effective for us beginning July 1, 2017 and early adoption is not permitted. We

anticipate this standard will have a material impact on our consolidated financial statements, and we are currently

evaluating its impact.

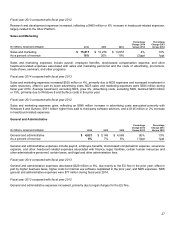

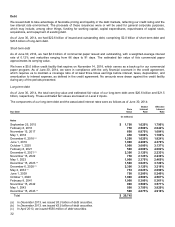

APPLICATION OF CRITICAL ACCOUNTING POLICIES

Our consolidated financial statements and accompanying notes are prepared in accordance with U.S. GAAP. Preparing

consolidated financial statements requires management to make estimates and assumptions that affect the reported

amounts of assets, liabilities, revenue, and expenses. These estimates and assumptions are affected by management’s

application of accounting policies. Critical accounting policies for us include revenue recognition, impairment of investment

securities, goodwill, research and development costs, contingencies, income taxes, and inventories.

Revenue Recognition

Revenue recognition for multiple-element arrangements requires judgment to determine if multiple elements exist,

whether elements can be accounted for as separate units of accounting, and if so, the fair value for each of the elements.