Microsoft 2014 Annual Report Download - page 37

Download and view the complete annual report

Please find page 37 of the 2014 Microsoft annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

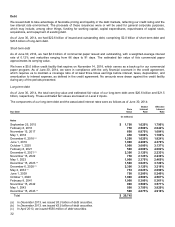

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

|

|

36

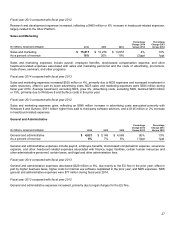

Judgment is also required to assess whether future releases of certain software represent new products or upgrades and

enhancements to existing products. Certain volume licensing arrangements include a perpetual license for current

products combined with rights to receive unspecified future versions of software products (“Software Assurance”) and are

accounted for as subscriptions, with billings recorded as unearned revenue and recognized as revenue ratably over the

coverage period.

Software updates are evaluated on a case-by-case basis to determine whether they meet the definition of an upgrade,

which may require revenue to be deferred and recognized when the upgrade is delivered. If it is determined that implied

post-contract customer support (“PCS”) is being provided, revenue from the arrangement is deferred and recognized over

the implied PCS term. If updates are determined to not meet the definition of an upgrade, revenue is generally recognized

as products are shipped or made available.

Microsoft enters into arrangements that can include various combinations of software, services, and hardware. Where

elements are delivered over different periods of time, and when allowed under U.S. GAAP, revenue is allocated to the

respective elements based on their relative selling prices at the inception of the arrangement, and revenue is recognized

as each element is delivered. We use a hierarchy to determine the fair value to be used for allocating revenue to

elements: (i) vendor-specific objective evidence of fair value (“VSOE”), (ii) third-party evidence, and (iii) best estimate of

selling price (“ESP”). For software elements, we follow the industry specific software guidance which only allows for the

use of VSOE in establishing fair value. Generally, VSOE is the price charged when the deliverable is sold separately or

the price established by management for a product that is not yet sold if it is probable that the price will not change before

introduction into the marketplace. ESPs are established as best estimates of what the selling prices would be if the

deliverables were sold regularly on a stand-alone basis. Our process for determining ESPs requires judgment and

considers multiple factors that may vary over time depending upon the unique facts and circumstances related to each

deliverable.

Windows 7 revenue was subject to deferral as a result of the Windows Upgrade Offer, which started June 2, 2012. The

offer provided significantly discounted rights to purchase Windows 8 Pro to qualifying end-users that purchased Windows

7 PCs during the eligibility period. Microsoft was responsible for delivering Windows 8 Pro to the end customer.

Accordingly, revenue related to the allocated discount for undelivered Windows 8 was deferred until it was delivered or the

redemption period expired.

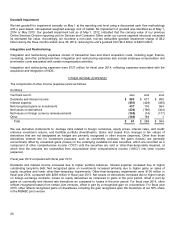

Impairment of Investment Securities

We review investments quarterly for indicators of other-than-temporary impairment. This determination requires significant

judgment. In making this judgment, we employ a systematic methodology quarterly that considers available quantitative

and qualitative evidence in evaluating potential impairment of our investments. If the cost of an investment exceeds its fair

value, we evaluate, among other factors, general market conditions, credit quality of debt instrument issuers, the duration

and extent to which the fair value is less than cost, and for equity securities, our intent and ability to hold, or plans to sell,

the investment. For fixed-income securities, we also evaluate whether we have plans to sell the security or it is more likely

than not that we will be required to sell the security before recovery. We also consider specific adverse conditions related

to the financial health of and business outlook for the investee, including industry and sector performance, changes in

technology, and operational and financing cash flow factors. Once a decline in fair value is determined to be other-than-

temporary, an impairment charge is recorded to other income (expense) and a new cost basis in the investment is

established. If market, industry, and/or investee conditions deteriorate, we may incur future impairments.

Goodwill

We allocate goodwill to reporting units based on the reporting unit expected to benefit from the business combination. We

evaluate our reporting units on an annual basis and, if necessary, reassign goodwill using a relative fair value allocation

approach. Goodwill is tested for impairment at the reporting unit level (operating segment or one level below an operating

segment) on an annual basis (May 1 for us) and between annual tests if an event occurs or circumstances change that

would more likely than not reduce the fair value of a reporting unit below its carrying value. These events or

circumstances could include a significant change in the business climate, legal factors, operating performance indicators,

competition, or sale or disposition of a significant portion of a reporting unit.