Sprint - Nextel 2005 Annual Report Download - page 113

Download and view the complete annual report

Please find page 113 of the 2005 Sprint - Nextel annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

|

|

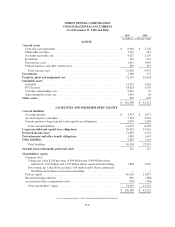

SPRINT NEXTEL CORPORATION

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS — (Continued)

Financial Accounting Standards Board, or FASB, Interpretation No. 47, or FIN 47, Accounting for Conditional

Asset Retirement Obligations was issued in 2005, interpreting the application of SFAS No. 143. FIN 47 requires

the recognition of a liability for legal obligations to perform an asset retirement activity in which the timing and

(or) method of the settlement are conditional on a future event. We adopted FIN 47 in the fourth quarter 2005

resulting in the recognition of asset retirement obligations in our Local segment for environmental remediation

requirements and contractual obligations for which estimated settlement dates can be determined. The asset

retirement obligations are comprised of removal and disposal of the asbestos in company buildings, removal and

environmental cleanup of fuel storage tanks used in standby power supply systems and decommissioning of

leased building spaces. An asset retirement obligation exists, but will not be recognized, in situations where

Local has been granted easements and rights-of-way by municipalities and private landowners to route its cable

facilities. Most cable facilities are buried; however, some metallic and fiber cable are above-ground on company-

owned poles. Local also contracts with other utilities to connect cable and wire to their poles. An estimated

settlement date for these obligations is indeterminate. Upon adoption in the fourth quarter 2005, an asset

retirement obligation of $33 million, a related asset of $6 million and a cumulative adjustment due to change in

accounting principle, net of tax, of $16 million were recorded.

Capitalized Interest

Capitalized interest totaled $55 million in 2005, $57 million in 2004, and $59 million in 2003. Capitalized

interest is incurred in connection with the construction of capital assets. SFAS No. 34, Capitalization of Interest

Costs, requires that assets under construction be incurring interest cost through the payment of cash or incurrence

of an interest-bearing liability in order to qualify for interest capitalization.

Intangible Assets

Goodwill and Other Indefinite Life Intangibles

In conformity with SFAS No. 142, Goodwill and Other Intangible Assets, we do not amortize our indefinite life

intangibles, which consist of our Federal Communications Commission, or FCC, licenses, goodwill, and the

Sprint and Boost Mobile trade names. We are required to test these assets for impairment at least annually or

whenever events or changes in circumstances indicate that the carrying amount may not be recoverable. We

perform our annual review for impairment in the fourth quarter of each year using the direct value method.

Goodwill represents the excess of the purchase price over the fair value of the net assets acquired in business

combinations accounted for as purchases. Virtually all of our goodwill is allocated to the Wireless segment. We

determine impairment of goodwill by comparing the net assets of the reporting unit, identified as our operating

segments, to their respective fair values. In the event a unit’s net assets exceed its fair value, an implied fair value

of goodwill must be determined by assigning the unit’s fair value to each asset and liability of the unit. The

excess of the fair value of the reporting unit over the amounts assigned to its assets and liabilities is the implied

fair value of goodwill. An impairment loss is measured by the difference between the goodwill carrying value

and the implied fair value.

For FCC licenses and other indefinite lived intangibles, we determine impairment by comparing an asset’s

respective carrying value to estimates of fair value using the direct value method, which requires the use of

estimates, judgments and projections. In the event impairment exists, a loss is recognized based on the amount by

which the carrying value exceeds the fair value of the asset. In accordance with EITF Issue No. 02-07, Unit of

Accounting for Testing Impairment of Indefinite-Lived Intangible Assets, our FCC licenses are combined as a

single unit of accounting for impairment testing purposes.

In 2005, we were assisted in our annual impairment review by an independent third party valuation firm and we

concluded that as of December 31, 2005, no impairments existed.

F-18