Sprint - Nextel 2005 Annual Report Download - page 149

Download and view the complete annual report

Please find page 149 of the 2005 Sprint - Nextel annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

-

161

|

|

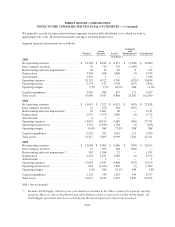

SPRINT NEXTEL CORPORATION

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS — (Continued)

At the time of the merger with Nextel, we did not extend plan participation to former Nextel employees.

Additionally, as of December 31, 2005, the pension plan was amended to freeze benefit accruals for plan

participants not designated to work for Embarq. This amendment was treated as a curtailment under SFAS

No. 88, Employers’ Accounting for Settlements and Curtailments of Defined Benefit Pension Plans and for

Termination Benefits. We recognized a $4 million curtailment loss. This amendment also resulted in a $233

million reduction in the projected benefit obligation, which is offset against existing unrecognized losses.

We use a December 31 measurement date for our pension plan.

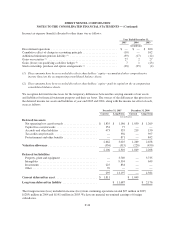

The following table shows the changes in the projected benefit obligation:

Year Ended December 31,

2005 2004

(in millions)

Benefit obligation at beginning of year ........................................ $ 4,466 $ 4,038

Service cost ............................................................. 134 133

Interest cost ............................................................. 264 250

Amendments ............................................................ 8 12

Curtailment ............................................................. (233) —

Actuarial loss ............................................................ 252 223

Benefits paid ............................................................ (208) (190)

Benefit obligation at end of year ............................................. $ 4,683 $ 4,466

The plan’s accumulated benefit obligation was $4.6 billion as of December 31, 2005 and $4.1 billion as of

December 31, 2004.

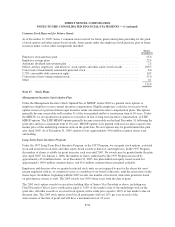

The following table shows the changes in plan assets:

Year Ended December 31,

2005 2004

(in millions)

Beginning balance ........................................................ $ 3,678 $ 3,176

Employer contributions .................................................... 300 300

Investment return ......................................................... 363 392

Benefits paid ............................................................ (208) (190)

Ending balance .......................................................... $ 4,133 $ 3,678

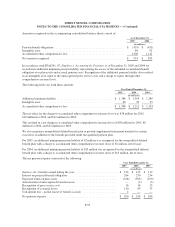

The funded status and amounts recognized on the accompanying consolidated balance sheets for the plan were as

follows:

As of December 31,

2005 2004

(in millions)

Projected benefit obligation in excess of plan assets ............................. $ (550) $ (788)

Unrecognized net losses ................................................... 1,424 1,551

Unrecognized prior service cost ............................................. 80 92

Unamortized transition asset ................................................ (1) (2)

Net amount recognized .................................................... $ 953 $ 853

F-54