Sprint - Nextel 2005 Annual Report Download - page 151

Download and view the complete annual report

Please find page 151 of the 2005 Sprint - Nextel annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161

|

|

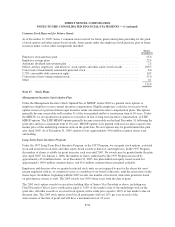

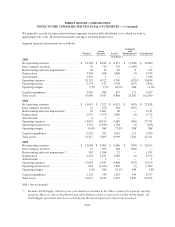

SPRINT NEXTEL CORPORATION

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS — (Continued)

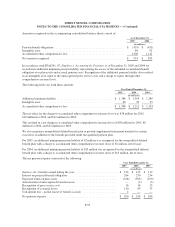

Weighted-average assumptions used to determine net periodic pension costs:

Year Ended December 31,

2005 2004 2003

Discount rate ....................................................... 6.00% 6.25% 6.75%

Expected long-term rate of return on plan assets ........................... 8.75% 8.75% 9.00%

Expected blended rate of future pay raises ................................ 4.25% 4.25% 4.25%

Weighted average assumptions used to determine benefit obligations:

As of December 31,

2005 2004

Discount rate ............................................................... 5.75% 6.00%

Expected blended rate of future pay raises ........................................ 4.25% 4.25%

In choosing the discount rate, our actuaries construct a hypothetical portfolio of bonds rated AA- or better that

produces a cash flow matching the projected benefit payments of the plan. The average yield of this portfolio is

used as the discount rate benchmark. For the December 31, 2005 measurement date, this exercise produced a

range of yields between 5.67% and 5.87%, and our discount rate was set at 5.75%. For the December 31, 2004

measurement date, the bond matching described above produced a range of yields between 5.86% and 6.04%,

guiding us to set the discount rate at 6.0%.

During 2005, the assumption regarding the expected long-term return on plan assets was 8.75%, unchanged from

the prior year. After revising the target asset allocation policy in the second half of 2003 to reduce the pension

trust’s exposure to equities, we obtained from two investment consulting firms forward-looking estimates of the

expected long-term returns for a portfolio invested according to the revised target policy. The average of the two

firms’ estimates was 8.77%, guiding a reduction in the assumed long-term return from the prior year’s 9.0% to

8.75%. We validate this assumption each year against estimates provided by our third party actuaries.

The plan’s asset allocations by asset category, are as follows:

As of December 31,

2005 2004

Equity securities ............................................................ 65% 66%

Debt securities .............................................................. 14% 17%

Real estate ................................................................. 11% 9%

Alternatives ................................................................ 10% 8%

Total ...................................................................... 100% 100%

The pension trust is invested in a well-diversified portfolio of securities. The Employee Benefits Committee has

established an investment policy that specifies asset allocation targets and ranges for the trust of: Equities 65%

(+/-10%), Debt 15% (+/-5%), Real Estate 10% (+/-5%), and Alternatives 10% (+/-5%). The pension trust holds

no Sprint Nextel securities.

The following benefit payments, which reflect expected future service, as appropriate, are expected to be paid (in

millions):

2006 ............................................................................. $ 190

2007 ............................................................................. 194

2008 ............................................................................. 199

2009 ............................................................................. 206

2010 ............................................................................. 214

2011 – 2015 ....................................................................... 1,223

F-56