Sprint - Nextel 2005 Annual Report Download - page 63

Download and view the complete annual report

Please find page 63 of the 2005 Sprint - Nextel annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

|

|

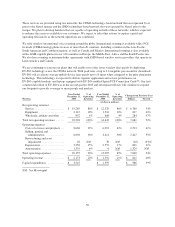

• the introduction of more competitive service pricing plans which are targeted at meeting more of our

customers’ needs;

• selected handset pricing promotions and improved handset choices;

• increased brand name recognition as a result of increased advertising and marketing campaigns, including

advertising and marketing related to our sponsorship of NASCAR and our agreement with the NFL that

began in 2005;

• increased market penetration as a result of opening additional retail stores and selling efforts targeted at

specific vertical markets; and

• the improvement in subscriber retention, which we believe is attributable to the impact of competitive rate

plans, as well as our focus on delivering high quality and differentiated service.

Our average monthly service revenue per user remained stable at $62 in 2004 and 2005 as:

• we integrated Nextel subscribers, who have a higher average monthly service revenue, in the third quarter

2005;

• we saw an increase in revenues from data services, as subscribers used more short message service, or

SMS, text messaging and took advantage of our wider array of premium services; and

• we experienced a full year of increased equipment protection plan rates that were restructured in 2004;

these increases were offset as

• we continued to offer more competitive service pricing plans, including lower priced plans, plans with a

higher number of bundled minutes included in the fixed monthly charge for the plan, plans that offer the

ability to share minutes among a group of related customers, or a combination of these features.

We expect that service revenues will increase in absolute terms in the future as a result of an increasing

subscriber base. As competition among wireless communications providers has increased, we and our

competitors have decreased prices while the average per subscriber utilization of wireless voice services has

increased, resulting in both declining average monthly revenue per subscriber in the wireless industry overall and

in declining average revenue per minute of use for voice services, and we expect these trends will continue. See

“—Forward Looking Statements.”

Revenues from sales of handsets and accessories, generated from both new subscribers and upgrades, were

approximately 10% of net operating revenues in both 2005 and 2004. These revenues increased $637 million or

42% from 2004 to 2005 primarily due to the merger with Nextel. The remainder of the increase was due to a 6%

increase in the number of CDMA handsets sold in 2005, largely offset by a 4% decrease in the average sales

price of the CDMA handsets. We continued to lower our handset retail prices in 2005 as costs of handsets

declined, and we also changed our third party compensation plan in 2005 from one that was based on discounted

handsets to one that is commissions-based. Additionally, we continued offering rebates on handsets as new

promotional programs were rolled out. Consistent with industry practice, our marketing plans assume that

handsets, net of rebates, will continue to be sold at prices below cost in most instances. Our retention efforts,

which often include providing incentives in the form of new handsets, may cause our handset subsidies to

increase as our customer base continues to grow. In addition, we may increase handset subsidies in response to

the competitive environment. See “—Forward Looking Statements.”

Wholesale, affiliate and other revenues increased $284 million or 47% from 2004 to 2005, reflecting the net

subscriber additions in the wholesale and PCS Affiliate bases. Wholesale operators added 1.5 million subscribers

52