Sysco 2009 Annual Report Download - page 42

Download and view the complete annual report

Please find page 42 of the 2009 Sysco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

|

|

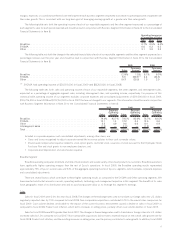

Under current law regarding multi-employer defined benefit plans, a plan’s termination, our voluntary withdrawal or the mass withdrawal of all

contributing employers from any underfunded multi-employer defined benefit plan would require us to make payments to the plan for our

proportionate share of the multi-employer plan’s unfunded vested liabilities. Based on the most recent information available from plan admin-

istrators, our share of withdrawal liability on most of the multi-employer plans we participate in, some of which appear to be underfunded, was

estimated to be $80,000,000 as of June 27, 2009 based on a voluntary withdrawal. Because we are not provided the information by the plan

administrators on a timely basis and we expect that many multi-employer pension plans’ assets have declined due to recent stock market

performance, we believe our share of the withdrawal liability could be greater.

Required contributions to multi-employer plans could increase in the future as these plans strive to improve their funding levels. In addition, the

Pension Protection Act, enacted in August 2006, requires underfunded pension plans to improve their funding ratios within prescribed intervals

based on the level of their underfunding. We believe that any unforeseen requirements to pay such increased contributions, withdrawal liability and

excise taxes would be funded through cash flow from operations, borrowing capacity or a combination of these items. As of June 27, 2009, we have

approximately $17,000,000 in liabilities recorded in total related to certain multi-employer defined benefit plans for which our voluntary withdrawal

has already occurred, all of which are expected to be paid in fiscal 2010.

During fiscal 2008, we obtained information that a multi-employer pension plan we participated in failed to satisfy minimum funding

requirements for certain periods and concluded that it was probable that additional funding would be required as well as the payment of excise tax.

As a result, during fiscal 2008, we recorded a liability of approximately $16,500,000 related to our share of the minimum funding requirements and

related excise tax for these periods. During the first quarter of fiscal 2009, we effectively withdrew from this multi-employer pension plan in an effort

to secure benefits for our employees that were participants in the plan and to manage our exposure to this under-funded plan. We agreed to pay

$15,000,000 to the plan, which included the minimum funding requirements. In connection with this withdrawal agreement, we merged active

participants from this plan into Sysco’s company-sponsored Retirement Plan and assumed $26,704,000 in liabilities. The payment to the plan was

made in the early part of the second quarter of fiscal 2009. If this plan were to undergo a mass withdrawal, as defined by the Pension Benefit

Guaranty Corporation, prior to September 2010, we could have additional liability. We do not currently believe a mass withdrawal from this plan prior

to September 2010 is probable.

We have experienced other instances triggering voluntary withdrawal from multi-employer pension plans. Withdrawal liabilities incurred

include $9,585,000 in fiscal 2009, $5,784,000 in fiscal 2008 and $4,700,000 in fiscal 2007.

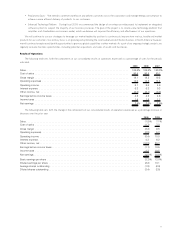

BSCC Cooperative Structure

Sysco’s affiliate, Baugh Supply Chain Cooperative (BSCC), is a cooperative taxed under subchapter T of the United States Internal Revenue

Code the operation of which has resulted in a deferral of tax payments. The IRS, in connection with its audits of our 2003 through 2006 federal

income tax returns proposed adjustments that would have accelerated amounts that we had previously deferred and would have resulted in the

payment of interest on those deferred amounts. Sysco reached a settlement with the IRS on August 21, 2009 to cease paying U.S. federal taxes

related to BSCC on a deferred basis, pay the amounts currently recorded within deferred taxes related to BSCC over a three year period and make a

one-time payment of $41,000,000, of which approximately $39,000,000 is non-deductible.The settlement addresses the BSCC deferred tax issue

as it relates to the IRS audit of our 2003 through 2006 federal income tax returns, and settles the matter for all subsequent periods, including the

2007 and 2008 federal income tax returns already under audit. As a result of the settlement, we will pay the amounts owed in the following

schedule:

Amounts paid annually:

Fiscal 2010 . .................................................................................. $ 528,000,000

Fiscal 2011 ................................................................................... 212,000,000

Fiscal 2012 ................................................................................... 212,000,000

Of the amounts to be paid in fiscal 2010 included in the table above, $316,000,000 will be paid in the first quarter of fiscal 2010 and the

remaining payments will be paid in quarterly installments beginning in the second quarter of fiscal 2010. Amounts to be paid in fiscal 2011 and 2012

will be paid with Sysco’s quarterly tax payments. We believe we have access to sufficient cash on hand, cash flows from operations and current

access to capital to make payments on all of the amounts noted above.

Off-Balance Sheet Arrangements

We have no off-balance sheet arrangements.

22