Sysco 2009 Annual Report Download - page 62

Download and view the complete annual report

Please find page 62 of the 2009 Sysco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

|

|

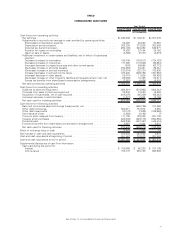

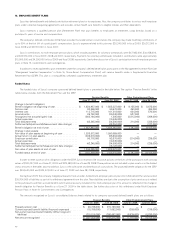

Shipping and Handling Costs

Shipping and handling costs include costs associated with the selection of products and delivery to customers. Included in operating expenses

are shipping and handling costs of approximately $2,136,836,000 in fiscal 2009, $2,155,794,000 in fiscal 2008, and $1,977,516,000 in fiscal 2007.

Insurance Program

Sysco maintains a self-insurance program covering portions of workers’ compensation, general and vehicle liability costs. The amounts in

excess of the self-insured levels are fully insured by third party insurers. The company also maintains a fully self-insured group medical program.

Liabilities associated with these risks are estimated in part by considering historical claims experience, medical cost trends, demographic factors,

severity factors and other actuarial assumptions.

Share-Based Compensation

Sysco recognizes expense for its share-based compensation based on the fair value of the awards that are granted. The fair value of the stock

options is estimated at the date of grant using the Black-Scholes option pricing model. Option pricing methods require the input of highly subjective

assumptions, including the expected stock price volatility. The fair value of restricted stock awards is based on the company’s stock price on the date

of grant. Measured compensation cost is recognized ratably over the vesting period of the related share-based compensation award. Cash flows

resulting from tax deductions in excess of the compensation cost recognized for those options (excess tax benefits) are classified as financing cash

flows on the consolidated cash flows statements.

Acquisitions

Acquisitions of businesses are accounted for using the purchase method of accounting, and the financial statements include the results of the

acquired operations from the respective dates of acquisition.

The purchase price of the acquired entities is allocated to the net assets acquired and liabilities assumed based on the estimated fair value at the

dates of acquisition, with any excess of cost over the fair value of net assets acquired, including intangibles, recognized as goodwill. The balances

included in the consolidated balance sheets related to recent acquisitions are based upon preliminary information and are subject to change when

final asset and liability valuations are obtained. Material changes to the preliminary allocations are not anticipated by management.

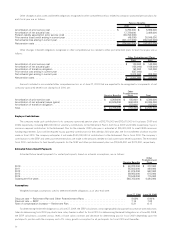

2. CHANGES IN ACCOUNTING

SFAS 165 Adoption

In May 2009, the FASB issued SFAS No. 165, “Subsequent Events” ( SFAS 165), which established general standards of accounting for and

disclosure of events that occur after the balance sheet date but before financial statements are issued or are available to be issued. Specifically, the

standard sets forth the period after the balance sheet date during which management should evaluate events or transactions that may occur for

potential recognition or disclosure in the financial statements, the circumstances under which an entity should recognize events or transactions

occurring after the balance sheet date in its financial statements, and the disclosures that an entity should make about events or transactions that

occurred after the balance sheet date. This standard became effective for Sysco for its fiscal year ending June 27, 2009. The company has included

the required disclosures for this standard in Note 1, “Summary of Accounting Policies.”

SFAS 161

As of the third quarter of fiscal 2009, SFAS No. 161, “Disclosure about Derivative Instruments and Hedging Activities, an amendment of FASB

Statement No. 133” (SFAS 161) became effective for Sysco. SFAS 161 requires enhanced disclosures about an entity’s derivative and hedging

activities and thereby improves the transparency of financial reporting. The company has determined that no additional disclosures were necessary

upon adoption but will continue to assess the need for additional disclosures in future periods.

SFAS 157

As of June 29, 2008, Sysco adopted the provisions of FASB Statement No. 157, “ Fair Value Measurements” (SFAS 157), for financial assets and

liabilities carried at fair value and non-financial assets and liabilities that are recognized or disclosed at fair value on a recurring basis. SFAS 157

establishes a common definition for fair value under generally accepted accounting principles, establishes a framework for measuring fair value and

expands disclosure requirements about such fair value measurements. The adoption of SFAS 157 for financial assets and liabilities carried at fair

value and non-financial assets and liabilities that are recognized or disclosed at fair value on a recurring basis did not have a material impact on the

company’s financial statements. See also the discussion of FASB Staff Position 157-2, “Effective Date of FASB Statement No. 157,” in Note 3, New

Accounting Standards.

FIN 48

Effective July 1, 2007, Sysco adopted FASB Interpretation No. 48, “Accounting for Uncertainty in Income Taxes — an Interpretation of FASB

Statement No. 109” (FIN 48), which clarifies the accounting for uncertainty in income taxes recognized in accordance with SFAS No. 109,

“Accounting for Income Taxes” (SFAS 109). FIN 48 clarifies the application of SFAS 109 by defining criteria that an individual tax position must meet

42