Sysco 2009 Annual Report Download - page 70

Download and view the complete annual report

Please find page 70 of the 2009 Sysco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

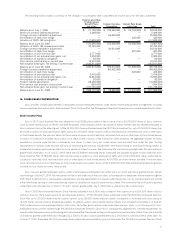

|

|

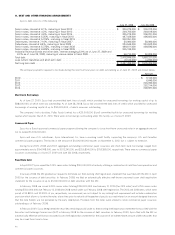

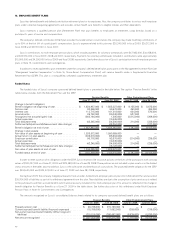

Other changes in plan assets and benefit obligations recognized in other comprehensive loss related to company-sponsored pension plans for

each fiscal year are as follows:

2009 2008

Pension Benefits

Amortization of prior service cost ........................................... $ 3,793,000 $ 5,985,000

Amortization of net actuarial loss. ........................................... 17,729,000 3,409,000

Pension liability assumption (prior service cost) . ................................. (26,704,000) —

Prior service (cost) credit arising in current year ................................. (48,000) 30,048,000

Net actuarial loss arising in current year . . ..................................... (201,417,000) (232,044,000)

Net pension costs . ..................................................... $ (206,647,000) $ (192,602,000)

Other changes in benefit obligations recognized in other comprehensive loss related to other postretirement plans for each fiscal year are as

follows:

2009 2008

Other Postretirement Plans

Amortization of prior service cost ................................................. $ 130,000 $ 143,000

Amortization of net actuarial gain ................................................. (158,000) (156,000)

Amortization of transition obligation ............................................... 153,000 153,000

Prior service cost arising in current year . . . ......................................... (527,000) —

Net actuarial gain arising in current year . . . ......................................... 3,813,000 208,000

Net pension costs. ........................................................... $ 3,411,000 $ 348,000

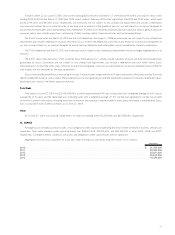

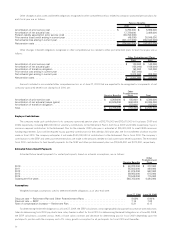

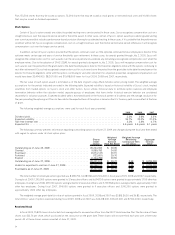

Amounts included in accumulated other comprehensive loss as of June 27, 2009 that are expected to be recognized as components of net

company-sponsored benefit cost during fiscal 2010 are:

Pension Benefits

Other

Postretirement

Plans Total

Amortization of prior service cost . .................................. $ 4,209,000 $ 185,000 $ 4,394,000

Amortization of net actuarial losses (gains) ............................ 40,526,000 (490,000) 40,036,000

Amortization of transition obligation ................................. — 153,000 153,000

Total . ...................................................... $ 44,735,000 $ (152,000) $ 44,583,000

Employer Contributions

The company made cash contributions to its company-sponsored pension plans of $95,776,000 and $92,670,000 in fiscal years 2009 and

2008, respectively, including $80,000,000 in voluntary contributions to the Retirement Plan in both fiscal 2009 and 2008, respectively. Sysco’s

minimum required contribution to the Retirement Plan for the calendar 2009 plan year is estimated at $95,000,000 to meet ERISA minimum

funding requirements. Sysco will be required to pay quarterly contributions for the calendar 2010 plan year, the first installment of which must be

made in fiscal 2010. The company anticipates it will make $140,000,000 of contributions to the Retirement Plan in fiscal 2010. The company’s

contributions to the SERP and other post-retirement plans are made in the amounts needed to fund current year benefit payments. The estimated

fiscal 2010 contributions to fund benefit payments for the SERP and other postretirement plans are $19,445,000 and $372,000, respectively.

Estimated Future Benefit Payments

Estimated future benefit payments for vested participants, based on actuarial assumptions, are as follows:

Pension Benefits

Other

Postretirement

Plans

2010 ................................................................... $ 50,222,000 $ 372,000

2011 ................................................................... 55,503,000 469,000

2012 ................................................................... 61,974,000 562,000

2013 ................................................................... 69,983,000 618,000

2014 ................................................................... 78,548,000 715,000

Subsequent five years ....................................................... 546,763,000 4,484,000

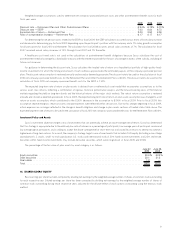

Assumptions

Weighted-average assumptions used to determine benefit obligations as of year-end were:

June 27, 2009 June 28, 2008

Discount rate — Retirement Plan and Other Postretirement Plans . . . ........................ 8.02% 6.94%

Discount rate — SERP ......................................................... 7.14 7.03

Rate of compensation increase — Retirement Plan. . . ................................... 5.21 6.17

For determining the benefit obligations as of June 27, 2009, the SERP calculations use an age-graded salary growth assumption with reductions

taken for determining fiscal 2010 pay due to base salary freezes in effect for fiscal 2010. For determining the benefit obligations as of June 28, 2008,

the SERP calculations assumed various levels of base salary increase and decrease for determining pay for fiscal 2009 depending upon the

participant’s position with the company and a 7% salary growth assumption for all participants for fiscal 2010 and thereafter.

50