Sysco 2009 Annual Report Download - page 43

Download and view the complete annual report

Please find page 43 of the 2009 Sysco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

|

|

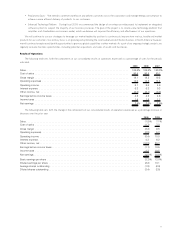

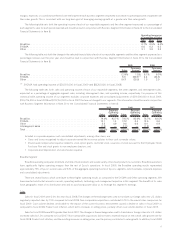

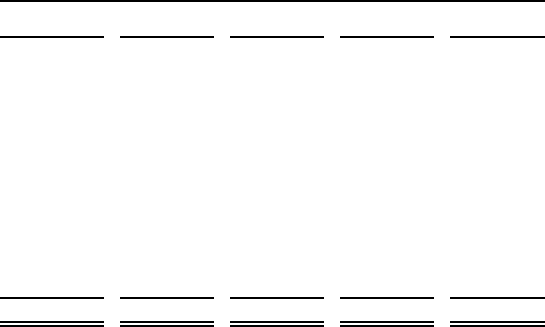

Contractual Obligations

The following table sets forth, as of June 27, 2009, certain information concerning our obligations and commitments to make contractual future

payments:

Total G1 Year 1-3 Years 3-5 Years

More Than

5 Years

Payments Due by Period

(In thousands)

Recorded Contractual Obligations:

Long-term debt . ............................... $ 2,434,859 $ 250 $ 200,547 $ 455,065 $ 1,778,997

Capital lease obligations . ......................... 41,790 8,913 10,489 4,136 18,252

Deferred compensation

(1)

......................... 139,938 56,554 18,981 12,264 52,139

SERP and other postretirement plans

(2)

............... 258,908 19,817 43,293 48,694 147,104

Multi-employer pension plans

(3)

..................... 16,869 16,869 — — —

Unrecognized tax benefits and interest

(4)

.............. 225,569 41,000

IRS deferred tax settlement

(4)

...................... 911,000 487,000 424,000 — —

Unrecorded Contractual Obligations:

Interest payments related to commercial paper and debt

(5)

. . 1,598,374 133,233 266,465 231,564 967,112

Retirement plan

(6)

.............................. 1,441,391 21,754 312,368 337,475 769,794

Long-term non-capitalized leases . ................... 229,091 51,289 69,967 41,932 65,903

Purchase obligations

(7)

........................... 3,149,072 2,287,839 750,973 95,135 15,125

Total contractual cash obligations ................. $ 10,446,861 $ 3,124,518 $ 2,097,083 $ 1,226,265 $ 3,814,426

(1)

The estimate of the timing of future payments under the Executive Deferred Compensation Plan involves the use of certain

assumptions, including retirement ages and payout periods. Included in the G1 Year amount are accelerated distributions to

participants who took advantage during calendar year 2008 of a one-time opportunity, pursuant to certain transitional relief under the

provisions of Section 409A of the Internal Revenue Code, to elect to receive a distribution of all or a portion of their vested balances

under the plan in early fiscal 2010.

(2)

Includes estimated contributions to the unfunded SERP and other postretirement benefit plans made in amounts needed to fund benefit

payments for vested participants in these plans through fiscal 2019, based on actuarial assumptions.

(3)

Represents voluntary withdrawal liabilities recorded and excludes normal contributions required under our collective bargaining

agreements.

(4)

Unrecognized tax benefits relate to uncertain tax positions recorded under accounting standards related to uncertain tax positions. As

of June 27, 2009, we had a liability of $78,571,000 for unrecognized tax benefits for all tax jurisdictions and $146,998,000 for related

interest that could result in cash payment. Sysco reached a settlement with the IRS on August 21, 2009 related to timing of tax

payments.This will result in a one-time payment of $41,000,000 as well as accelerating the payments previously deferred. See further

discussion of this settlement under Note 22, Subsequent Events, in the Notes to Consolidated Financial Statements in Item 8. Apart

from this settlement, we are not able to reasonably estimate the timing of non-current payments or the amount by which the liability

will increase or decrease over time, the related non-current balances have not been reflected in the “Payments Due by Period” section of

the table.

(5)

Includes payments on floating rate debt based on rates as of June 27, 2009, assuming amount remains unchanged until maturity, and

payments on fixed rate debt based on maturity dates.

(6)

Provides the estimated minimum contribution to the Retirement Plan through fiscal 2019 to meet ERISA minimum funding

requirements.

(7)

For purposes of this table, purchase obligations include agreements for purchases of product in the normal course of business, for which

all significant terms have been confirmed, including minimum quantities resulting from our sourcing initiative. Such amounts included

in the table above are based on estimates. Purchase obligations also includes amounts committed with a third party to provide

hardware and hardware hosting services over a ten year period ending in fiscal 2015 (See discussion under Note 19, Commitments and

Contingencies, in the Notes to Consolidated Financial Statements in Item 8), fixed electricity agreements and fixed fuel purchase

commitments. Purchase obligations exclude full requirements electricity contracts where no stated minimum purchase volume is

required.

Certain acquisitions involve contingent consideration, typically payable only in the event that certain operating results are attained or certain

outstanding contingencies are resolved. Aggregate contingent consideration amounts outstanding as of June 27, 2009 included $78,250,000 in

cash. This amount is not included in the table above.

Critical Accounting Policies and Estimates

The preparation of financial statements in conformity with generally accepted accounting principles requires us to make estimates and

assumptions that affect the reported amounts of assets, liabilities, sales and expenses in the accompanying financial statements. Significant

accounting policies employed by Sysco are presented in the notes to the financial statements.

Critical accounting policies and estimates are those that are most important to the portrayal of our financial condition and results of operations.

These policies require our most subjective or complex judgments, often employing the use of estimates about the effect of matters that are

23