Walmart 2016 Annual Report Download - page 24

Download and view the complete annual report

Please find page 24 of the 2016 Walmart annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

|

|

2016 Annual Report22

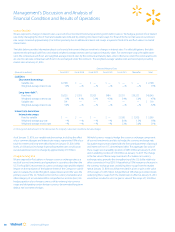

Management’s Discussion and Analysis of

Financial Condition and Results of Operations

a factor of eight for rent expense that estimates the hypothetical capitalization

of our operating leases. We consider return on assets (“ROA”) to be the

financial measure computed in accordance with GAAP that is the most

directly comparable financial measure to our calculation of ROI. ROI differs

from ROA (which is consolidated income from continuing operations for the

period divided by average total assets of continuing operations for the

period) because ROI: adjusts operating income to exclude certain expense

items and adds interest income; adjusts total assets of continuing opera-

tions for the impact of accumulated depreciation and amortization,

accounts payable and accrued liabilities; and incorporates a factor of rent to

arrive at total invested capital. Because of the adjustments mentioned

above, we believe ROI more accurately measures how we are deploying

our key assets and is more meaningful to investors than ROA.

Although ROI is a standard financial metric, numerous methods exist for

calculating a company’s ROI. As a result, the method used by management

to calculate our ROI may differ from the methods used by other companies

to calculate their ROI.

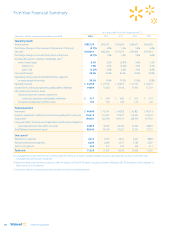

The calculation of ROI, along with a reconciliation to the calculation of

ROA, the most comparable GAAP financial measure, is as follows:

Fiscal Years

Ended January 31,

(Amounts in millions) 2016 2015

CALCULATION OF RETURN ON INVESTMENT

Numerator

Operating income $ 24,105 $ 27,147

+ Interest income 81 113

+ Depreciation and amortization 9,454 9,173

+ Rent 2,532 2,777

= Adjusted operating income $ 36,172 $ 39,210

Denominator

Average total assets of

continuing operations

(1)

$201,536 $203,786

+ Average accumulated depreciation

and amortization

(1)

68,759 63,375

- Average accounts payable

(1)

38,449 37,913

- Average accrued liabilities

(1)

19,380 18,973

+ Rent x 8 20,256 22,216

= Average invested capital $232,722 $232,491

Return on investment (ROI) 15.5% 16.9%

CALCULATION OF RETURN ON ASSETS

Numerator

Income from continuing operations $ 15,080 $ 16,814

Denominator

Average total assets of

continuing operations

(1)

$201,536 $203,786

Return on assets (ROA) 7.5% 8.2%

As of January 31,

2016 2015 2014

Certain Balance Sheet Data

Total assets of

continuing operations

(2)

$199,581 $203,490 $204,081

Accumulated depreciation

and amortization 71,538 65,979 60,771

Accounts payable 38,487 38,410 37,415

Accrued liabilities 19,607 19,152 18,793

(1) The average is based on the addition of the account balance at the end of the current

period to the account balance at the end of the prior period and dividing by 2.

(2) Total assets of continuing operations were adjusted to reflect the adoption of

ASU 2015- 03, Interest-Imputation of Interest (Subtopic 835-30): Simplifying

the Presentation of Debt Issuance Cost, for all periods.

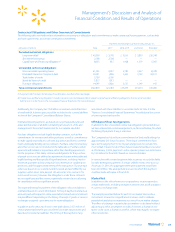

Free Cash Flow

Free cash flow is considered a non-GAAP financial measure. Management

believes, however, that free cash flow, which measures our ability to

generate additional cash from our business operations, is an important

financial measure for use in evaluating the Company’s financial perfor-

mance. Free cash flow should be considered in addition to, rather than

as a substitute for, consolidated income from continuing operations

as a measure of our performance and net cash provided by operating

activities as a measure of our liquidity.

We define free cash flow as net cash provided by operating activities

in a period minus payments for property and equipment made in that

period. We generated free cash flow of $15.9 billion, $16.4 billion and

$10.1 billion for fiscal 2016, 2015 and 2014, respectively. The decrease in

free cash flow in fiscal 2016 from fiscal 2015 was primarily due to lower

income from continuing operations, partially offset by lower capital

spending and improved working capital management.

Walmart’s definition of free cash flow is limited in that it does not

represent residual cash flows available for discretionary expenditures due

to the fact that the measure does not deduct the payments required for

debt service and other contractual obligations or payments made for

business acquisitions. Therefore, we believe it is important to view free

cash flow as a measure that provides supplemental information to our

Consolidated Statements of Cash Flows.

Although other companies report their free cash flow, numerous methods

may exist for calculating a company’s free cash flow. As a result, the

method used by Walmart’s management to calculate our free cash flow

may differ from the methods used by other companies to calculate their

free cash flow.