Walmart 2016 Annual Report Download - page 30

Download and view the complete annual report

Please find page 30 of the 2016 Walmart annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

|

|

2016 Annual Report28

Management’s Discussion and Analysis of

Financial Condition and Results of Operations

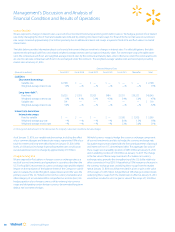

Company Share Repurchase Program

From time to time, we repurchase shares of our common stock under

share repurchase programs authorized by the Company’s Board of

Directors. On October 13, 2015, the Board of Directors replaced the

previous $15.0 billion share repurchase program, which had $8.6 billion

of remaining authorization for share repurchases as of that date, with a

new $20.0 billion share repurchase program. As was the case with the

replaced share repurchase program, the new share repurchase program

has no expiration date or other restrictions limiting the period over

which we can make share repurchases. At January 31, 2016, authorization

for $17.5 billion of share repurchases remained under the current share

repurchase program. Any repurchased shares are constructively retired

and returned to an unissued status. The Company intends to utilize the

current share repurchase authorization through the fiscal year ending

January 31, 2018.

We regularly review share repurchase activity and consider several factors

in determining when to execute share repurchases, including, among

other things, current cash needs, capacity for leverage, cost of borrowings,

our results of operations and the market price of our common stock. We

anticipate that a significant majority of the ongoing share repurchase

program will be funded through the Company’s free cash flows. The

following table provides, on a settlement date basis, the number of

shares repurchased, average price paid per share and total amount paid

for share repurchases for fiscal 2016, 2015 and 2014:

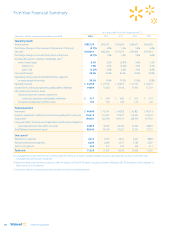

(Amounts in millions, Fiscal Years Ended January 31,

except per share data) 2016 2015 2014

Total number of shares repurchased 62.4 13.4 89.1

Average price paid per share $65.90 $75.82 $74.99

Total amount paid for share repurchases $4,112 $1,015 $6,683

Share repurchases increased $3.1 billion for fiscal 2016 and decreased

$5.7 billion for fiscal 2015, respectively, when compared to the previous

fiscal year. For fiscal 2016, the increase in share repurchases resulted from

our intention to utilize the current share repurchase authorization over

the next two years. For fiscal 2015, the decrease was a result of cash

needs, reduced leverage and increased cash used in transactions with

noncontrolling interests described further below.

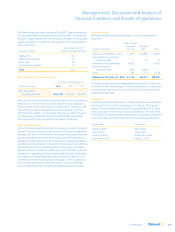

Significant Transactions with Noncontrolling Interests

As described in Note 13 to our Consolidated Financial Statements, in July

2015, we completed the purchase of all of the remaining noncontrolling

interest in Yihaodian, our e-commerce operations in China, for approxi-

mately $760 million, using existing cash to complete this transaction and

during fiscal 2015, we completed the purchase of substantially all of the

remaining noncontrolling interest in Walmart Chile for approximately

$1.5 billion, using existing cash to complete this transaction.

Capital Resources

We believe cash flows from continuing operations, our current cash

position and access to capital markets will continue to be sufficient to

meet our anticipated operating cash needs, which include funding

seasonal buildups in merchandise inventories and funding our capital

expenditures, dividend payments and share repurchases.

We have strong commercial paper and long-term debt ratings that have

enabled and should continue to enable us to refinance our debt as it

becomes due at favorable rates in capital markets. At January 31, 2016,

the ratings assigned to our commercial paper and rated series of our

outstanding long-term debt were as follows:

Rating agency Commercial paper Long-term debt

Standard & Poor’s A-1+ AA

Moody’s Investors Service P-1 Aa2

Fitch Ratings F1+ AA

Credit rating agencies review their ratings periodically and, therefore, the

credit ratings assigned to us by each agency may be subject to revision

at any time. Accordingly, we are not able to predict whether our current

credit ratings will remain consistent over time. Factors that could affect

our credit ratings include changes in our operating performance, the

general economic environment, conditions in the retail industry, our

financial position, including our total debt and capitalization, and

changes in our business strategy. Any downgrade of our credit ratings

by a credit rating agency could increase our future borrowing costs or

impair our ability to access capital and credit markets on terms

commercially acceptable to us. In addition, any downgrade of our

current short-term credit ratings could impair our ability to access the

commercial paper markets with the same flexibility that we have

experienced historically, potentially requiring us to rely more heavily

on more expensive types of debt financing. The credit rating agency

ratings are not recommendations to buy, sell or hold our commercial

paper or debt securities. Each rating may be subject to revision or

withdrawal at any time by the assigning rating organization and should

be evaluated independently of any other rating. Moreover, each credit

rating is specific to the security to which it applies.