Windstream 2011 Annual Report Download - page 166

Download and view the complete annual report

Please find page 166 of the 2011 Windstream annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

|

|

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

____

F-58

which are observable at commonly quoted intervals for the full term of the swaps using discount rates appropriate with

consideration given to our non-performance risk. As of December 31, 2011 and 2010, the fair values of our interest rate swaps

were reduced by $6.9 million and $4.6 million, respectively, to reflect our non-performance risk. Our non-performance risk is

assessed based on the current trading discount of our Tranche B senior secured credit facility as the swap agreements are

secured by the same collateral. In addition, we routinely monitor and update our evaluation of counterparty risk, and based on

such evaluation have determined that the swap agreements continue to meet the requirements of an effective cash flow hedge.

The counterparty to each of the four swap agreements is a bank with a current credit rating at or above A.

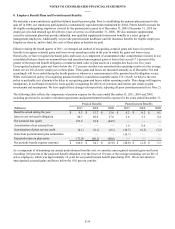

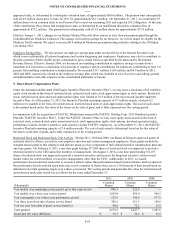

The fair value and carrying value of our long-term debt, including current maturities, was as follows at December 31:

(Millions)

Fair value

Carrying value

2011

$ 9,337.6

$ 9,150.4

2010

$ 7,649.1

$ 7,325.8

The fair value of the corporate bonds was calculated based on quoted market prices of the specific issuances in an active market

when available. When an active market is not available for certain bonds and bank debt, the fair market value and revolving

line of credit was determined based on bid prices and broker quotes. In calculating the fair market value of the Windstream

Holdings of the Midwest, Inc., an appropriate market price for the same or similar instruments in an active market is used

considering credit quality, nonperformance risk and maturity of the instrument.

7. Supplemental Cash Flow Information:

We declared and accrued cash dividends of $148.0 million, $126.5 million and $109.2 million during the fourth quarters of

2011, 2010 and 2009, respectively, which were subsequently paid in January of the following year.

On November 30, 2011, we issued 70.0 million shares of our common stock and assumed stock awards for a total transaction

value of $842.0 million, based on the closing price of our stock on November 30, 2011, and the fair value of the equity awards

assumed, as part of the consideration paid to acquire PAETEC (see Note 3). Also as part of this transaction, we assumed

$1,591.3 million in long-term debt net of cash acquired, which includes a net premium of $113.9 million based on the fair value

of the debt on November 30, 2011 and bank debt of $99.5 million that was repaid on December 1, 2011.

On February 28, 2011, we contributed 4.9 million shares of our common stock to our pension plan. At the time of this

contribution, these shares had an appraised value, as determined by a third-party valuation firm, of approximately $60.6

million. On September 21, 2011, we contributed 5.9 million shares of our common stock to our Pension Plan to meet our

remaining 2011 and expected 2012 obligation. At the time of the contribution, these shares had an appraised value, as

determined by an unaffiliated third party valuation firm, of approximately $75.2 million.

On December 2, 2010, we issued 20.6 million shares of our common stock with a fair market value of $271.6 million as part of

the consideration paid to acquire Q-Comm (see Note 3). Also as part of this transaction, we assumed $266.2 million in long-

term debt, including related interest rate swap liabilities, which was subsequently repaid.

On June 1, 2010, we issued 26.7 million shares of our common stock with a fair market value of $280.8 million as part of the

consideration paid to acquire Iowa Telecom (see Note 3). Also as part of this transaction, we assumed $628.9 million in long-

term debt, including related interest rate swap liabilities, which was subsequently repaid.

On February 8, 2010, we issued 18.7 million shares of our common stock with a fair market value of $185.0 million as part of

the consideration paid to acquire NuVox (see Note 3). Also as part of this transaction, we assumed $281.0 million in long-term

debt and related liabilities on existing swap agreements of NuVox, which was subsequently repaid.

On November 10, 2009, we issued 9.4 million shares of our common stock with a fair market value of $94.6 million as part of

consideration paid to acquire D&E (see Note 3). Also as part of this transaction, we assumed $182.4 million in long-term debt,

which was subsequently repaid as required under the change of control provisions of the D&E debt agreement.