Windstream 2012 Annual Report Download - page 101

Download and view the complete annual report

Please find page 101 of the 2012 Windstream annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

|

|

F-3

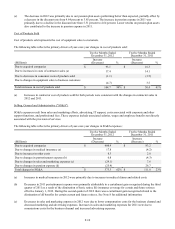

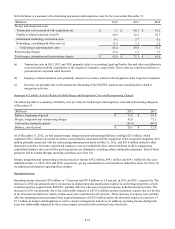

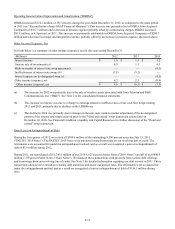

BUSINESS TRENDS

The following discussion highlights key trends affecting our business.

Business communications services: Demand for advanced communications services is expected to drive growth in revenues

from business customers. To meet this demand, we continue to expand our capabilities in integrated voice and data services,

which deliver voice and broadband services over a single Internet connection. We also offer multi-site networking services

which provide a fast and private connection between business locations as well as a variety of other data services. We view this

as a strategic growth area, but we are subject to competition from other carriers and cable television companies, which could

suppress growth. See "Competition" in Item 1 of Part I of this Annual Report for more details.

Data center services: Many businesses are moving towards cloud computing and managed services as an alternative to a

traditional information technology ("IT") infrastructure. Our data centers are capable of delivering those services, and we are

actively investing in data center expansion in order to meet the growing demand for these types of services. In addition to cloud

computing and managed services, our data centers offer colocation services, in which we provide a safe, secure environment

for storage of servers and networking equipment.

Wireless backhaul: As wireless data usage grows, wireless carriers need additional bandwidth on the wireline network to

accommodate the additional wireless traffic. We have made significant success-based capital investments to provide backhaul

services to wireless carriers. These investments include building out fiber to new wireless towers and replacing copper facilities

with fiber facilities to wireless towers we already serve. We spent approximately $270.5 million in fiber-to-the-tower

investments during 2012 and we expect to continue to make significant success-based capital investments in 2013 to offer

additional wireless backhaul services to wireless carriers; however, fiber to the tower investments will decrease in 2013.

Consumer high-speed Internet: New consumer high-speed Internet additions are slowing as a result of our already high

penetration of 71 percent of primary residential lines. We expect the pace of high-speed Internet customer growth to continue to

slow as the number of households without high-speed Internet service shrinks and our penetration continues to increase.

However, we believe growing customer demand for faster speeds and value-added services, such as online security and back-

up, will drive growth in consumer high-speed Internet revenues. We are continuing to focus on increasing our broadband

speeds available to customers. As of December 31, 2012, we could deliver speeds of 3 Megabits per second ("Mbps") to

approximately 97 percent of our addressable lines, and speeds of 6 Mbps, 12 Mbps and 24 Mbps are available to approximately

73 percent, 48 percent and 13 percent of our addressable lines, respectively.

Consumer voice line losses: Voice and switched access revenues will continue to be adversely impacted by future declines in

voice lines due to competition from cable television companies, wireless carriers and providers using other emerging

technologies. To combat competitive pressures, we continue to emphasize our bundled products and services. Our consumers

can bundle voice, high-speed Internet and video services, providing one convenient billing solution and bundle discounts. We

believe that product bundles positively impact customer retention, and the associated discounts provide our customers the best

value for their communications and entertainment needs. As of December 31, 2012, all of our voice lines had wireless

competition and approximately 70 percent of our voice lines had fixed-line voice competition. Consumer lines decreased

86,000, or 4.5 percent during 2012, primarily due to the effects of competition.

Synergies and operational efficiencies: We continually strive to identify opportunities for operational efficiencies, in the context

of both our acquired businesses and legacy operations. During the year ended December 31, 2012, we recognized

approximately $171.0 million in synergies from our acquisitions completed since the beginning of 2010, primarily related to

workforce and network efficiencies. In addition to acquisition-related synergies, we also evaluate our legacy operations for

operational efficiency. On May 31, 2012, we announced the review of our management structure to increase the efficiency of

decision-making, to ensure our management structure is as simple and as responsive to customers as possible and position

ourselves for continued success. We eliminated approximately 350 management positions as a part of the restructuring, which

was completed in the third quarter of 2012 and resulted in severance related costs of $22.4 million. The changes will result in

annualized savings of approximately $40.0 million. During 2010, we announced a workforce reduction which resulted in

annual pretax savings of approximately $20.0 million. We expect to continue to evaluate our operations for these opportunities.