Windstream 2012 Annual Report Download - page 141

Download and view the complete annual report

Please find page 141 of the 2012 Windstream annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

|

|

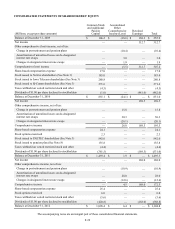

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

____

F-43

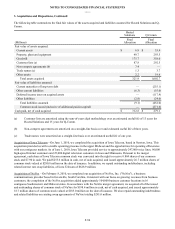

2. Summary of Significant Accounting Policies and Changes, Continued:

In 2006, we entered into four pay fixed, receive variable interest rate swap agreements to serve as cash flow hedges of the

interest rate risk inherent in our senior secured credit facilities. We renegotiated the four interest rate swap agreements on

December 3, 2010, and again on August 21, 2012, each time lowering the fixed interest rate paid and extending the maturity.

As a result of the August 21, 2012 transaction, we reduced our fixed rate paid from 4.553 percent to 3.391 percent effective

October 17, 2012. The fixed rate paid includes a component which serves to settle the liability existing on our swaps at the time

of the transaction. The variable rate received resets on the seventeenth day of each month to the one-month London Interbank

Offered Rate ("LIBOR"). Our swaps had a notional value of $943.8 million as of December 31, 2012, which will amortize to

$900.0 million on July 17, 2013, where they will remain until maturity.

The current swaps are designated as cash flow hedges of the benchmark LIBOR interest rate risk created by the variable rate

cash flows paid on our senior secured credit facilities, which have varying maturity dates from July 17, 2013 to August 8, 2019.

We are hedging probable variable cash flows which extend up to four years beyond the maturity of certain components of our

variable rate debt. Consistent with past practice, we expect to extend or otherwise replace these components of our debt with

variable rate debt.

We recognize all derivative instruments at fair value in the accompanying consolidated balance sheets as either assets or

liabilities, depending on the rights or obligations under the related contracts.

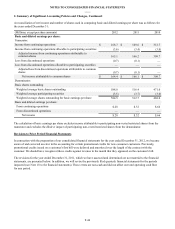

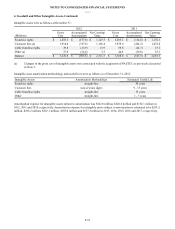

Set forth below is information related to our interest rate swap agreements:

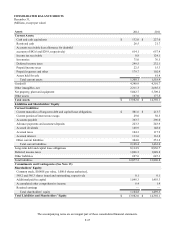

(Millions, except for percentages) 2012 2011 2010

Designated portion, measured at fair value

Other current liabilities $ 29.0 $ 30.5 $ 35.4

Other non-current liabilities $ 91.2 $ 88.7 $ 75.9

Accumulated other comprehensive (loss) income $ (14.7)$ (26.9) $ 5.6

De-designated portion, unamortized value

Accumulated other comprehensive loss $ (45.9)$ (58.6)$ (107.6)

Weighted average fixed rate paid 4.26% 4.60% 5.60%

Variable rate received 0.21% 0.40% 0.29%

We assess our derivatives for effectiveness each quarter and recognized a $7.5 million charge to earnings, reflected in other

income (expense), net related to ineffectiveness of our cash flow hedges for the twelve months ended December 31, 2012.

Our swaps are off-market swaps, meaning they contain an embedded financing element. Our swap counterparties recover this

financing through an incremental charge in our fixed rate over what we would be charged for an on-market swap. As such, a

portion of our swaps' cash payment is representing the rate we would pay on a hypothetical on-market interest rate swap and is

recognized in interest expense. The remainder represents the repayment of the embedded financing element and reduces our

swap liability.

All or a portion of the change in fair value of our interest rate swap agreements recorded in accumulated other comprehensive

income (loss) may be recognized in earnings in certain situations. If we extinguish all of our variable rate debt, or a portion of

our variable rate debt such that our variable rate interest received on our swaps exceeds the variable rate interest paid on our

debt, we would recognize in earnings all or a portion of the change in fair value of our swaps. In addition, we may recognize

the change in fair value of our swaps in earnings if we determine it is no longer probable that we will have future variable rate

cash flows to hedge against or if a swap agreement is terminated prior to maturity. We have assessed our counterparty risk and

determined that no substantial risk of default exists as of December 31, 2012. Each counterparty is a bank with a current credit

rating at or above A.

We expect to recognize losses of $17.9 million, net of taxes, in interest expense in the next twelve months related to the

unamortized value of the de-designated portion of interest rate swap agreements at December 31, 2012. Payments on our off-

market swaps are presented in the financing activities section of our consolidated statements of cash flows.