Windstream 2012 Annual Report Download - page 161

Download and view the complete annual report

Please find page 161 of the 2012 Windstream annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

|

|

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

____

F-63

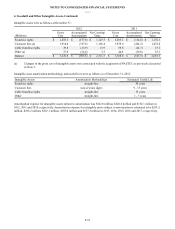

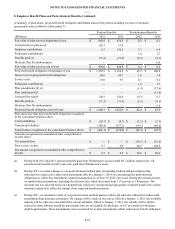

8. Employee Benefit Plans and Postretirement Benefits, Continued:

Information regarding the healthcare cost trend rate was as follows for the years ended December 31:

2012 2011

Healthcare cost trend rate assumed for next year 9.00% 9.00%

Rate that the cost trend ultimately declines to 5.00% 5.00%

Year that the rate reaches the terminal rate 2019 2017

For the year ended December 31, 2012, a one percent increase in the assumed healthcare cost trend rate would increase the

postretirement benefit cost by approximately $0.2 million, while a one percent decrease in the rate would reduce the

postretirement benefit cost by approximately $0.1 million. As of December 31, 2012, a one percent increase in the assumed

healthcare cost trend rate would increase the postretirement benefit obligation by approximately $3.0 million, while a one

percent decrease in the rate would reduce the postretirement benefit obligation by approximately $2.3 million.

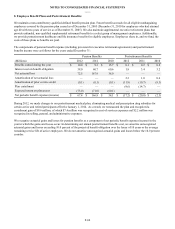

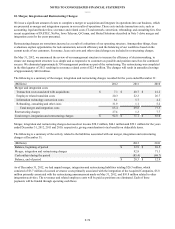

Plan Assets – Our pension plan assets are allocated to asset categories based on the specific strategy employed by the asset’s

investment manager. The asset allocation for our pension plan by asset category was as follows for the years ended December

31:

Target Allocation Percentage of Plan Assets

Asset Category 2013 2012 2011

Equity securities 18.6% - 30.6% 44.2% 50.8%

Fixed income securities 43.2% - 70.2% 33.8% 39.2%

Alternative investments 10.8% - 20.8% 4.4% 3.7%

Money market and other short-term interest bearing securities 3.0% - 3.0% 17.6% 6.3%

100.0% 100.0%

In 2012, we engaged a third party to evaluate the allocation of the total assets in the pension trust, taking into consideration the

pension liabilities and funded status of the pension plan. Assets are managed utilizing a Liability Driven Investment ("LDI")

approach, meaning that assets are managed within a risk management framework which addresses the need to generate

incremental returns in the context of an appropriate level of risk, based on plan liability profiles and changes in funded status.

The return objectives are to satisfy funding obligations when and as prescribed by law and to keep pace with the growth of the

pension plan liabilities. Given the long time horizon for paying out benefits and our strong financial condition, the pension plan

can accept an average level of risk relative to other similar plans. The liquidity needs of the pension plan are manageable given

that lump sum payments are not available to most participants.

Equity securities include stocks of both large and small capitalization domestic and international companies. Equity securities

are expected to provide both diversification and long-term real asset growth. Domestic equities may include modest holdings of

non-U.S. equities, purchased by domestic equity managers as long as they are traded in the U.S and denominated in U.S.

dollars and both active and passive (index) investment strategies. International equities provide a broad exposure to return

opportunities and investment characteristics associated with the world equity markets outside the U.S. The pension plan’s

equity holdings are diversified by investment style, market capitalization, market or region, and economic sector.

Fixed income securities include securities issued by the U.S. Government and other governmental agencies, asset-backed

securities and debt securities issued by domestic and international entities. These securities are expected to provide

diversification benefits, and are expected to reduce asset volatility and pension funding volatility, and a stable source of

income.

Alternative investments may include hedge funds and hedge fund of funds, commodities, both private and public real estate and

private equity investments. In addition to attractive diversification benefits, the alternative investments are expected to provide

both income and capital appreciation.

Investments in money market and other short-term interest bearing securities are maintained to provide liquidity for benefit

payments with protection of principal being the primary objective.