Windstream 2012 Annual Report Download - page 120

Download and view the complete annual report

Please find page 120 of the 2012 Windstream annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

|

|

F-22

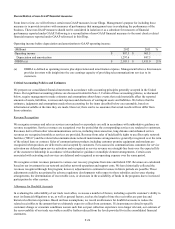

operations while dividend payments, share repurchases and other certain restricted investments reduce the available restricted

payments capacity.

Debt Covenants and Amendments

The terms of the credit facility and indentures, issued by Windstream, include customary covenants that, among other things,

require us to maintain certain financial ratios and restrict our ability to incur additional indebtedness. These financial ratios

include a maximum leverage ratio of 4.5 to 1.0 and a minimum interest coverage ratio of 2.75 to 1.0. The terms of the

indentures assumed in connection with the acquisition of PAETEC, include restrictions on the ability of the subsidiary to incur

additional indebtedness, including a maximum leverage ratio with the most restrictive being 4.75 to 1.0.

Effective January 23, 2013, we amended and restated our senior secured credit facilities pursuant to the refinancing amendment

provisions thereunder to incur $1,345.0 million of Tranche B4 term loans due January 23, 2020, the proceeds of which were

used to refinance in full the outstanding Tranche A2, Tranche B1 and Tranche B2 term loans. The additional term loans under

the credit facility consist of $408.8 million Tranche A3 term loan due December 30, 2016, $292.5 million Tranche A4 term loan

due August 8, 2017 and $597.0 million Tranche B3 term loan due August 8, 2019.

Effective August 8, 2012, we amended and restated our existing senior secured credit facilities to provide for the incurrence of

up to $900.0 million of additional term loans. We used the proceeds to repay the full outstanding balance of the credit facility

revolver, without any reduction in commitments, and for general corporate purposes.

Effective February 23, 2012, we amended and restated $150.4 million of the Tranche A2 senior secured credit facilities

outstanding to Tranche A3 and extended the maturity to December 30, 2016. In addition, we incurred new borrowings of

$280.0 million of Tranche A3 senior secured credit facilities, which will also be due December 30, 2016. The proceeds from

these borrowings were used to partially repay the credit facility revolver, without any reduction in commitments. Additionally,

the restatement extended the maturity of certain existing term loans and provided for the ability to refinance and extend the

maturity of any term loan or revolving loan with the consent of the affected lenders, modify certain other definitions and

provisions and increase secured debt capacity to 2.25 times adjusted OIBDA, as defined per the credit facility. The restatement

also provided for unlimited additional tranches of secured incremental facilities, subject to no default, pro forma compliance

with the an interest coverage ratio test of 2.75 to 1.00 and a leverage ratio test of 4.00 to 1.00 and pro forma compliance with a

secured leverage ratio test of 2.25 to 1.00.

On August 11, 2011, in connection with our acquisition of PAETEC, we amended our senior secured credit agreement to,

among other things, (i) permit the issuance of bridge loans, (ii) permit the issuance and repayment of escrow notes, (iii) waive

guaranty and security requirements with regard to PAETEC and its subsidiaries, (iv) delete the capital expenditures covenant

and (v) waive any breach due to the change of control provisions under PAETEC's outstanding notes. In addition, we amended

the security agreement to, among other things, waive the obligation to grant security on accounts relating to escrow notes and

the proceeds of notes held in such accounts.

On September 17, 2010, we amended our credit facility to permit the signing of rural broadband stimulus grant agreements

with the Rural Utilities Service. On March 18, 2011, we increased the capacity under our senior secured revolving credit

facility from $750.0 million to $1,250.0 million. We had approximately $1,234.3 million of availability under our senior

secured revolving credit facility.

Scheduled principal payments for debt outstanding as of December 31, 2012 for each of the twelve month periods ended

December 31, 2013, 2014, 2015, 2016 and 2017 were $866.1 million, $85.1 million, $92.6 million, $350.8 million and

$1,964.6 million, respectively. Scheduled principal payments remaining after 2017 are $5,544.5 million.

Certain of our debt agreements contain various covenants and restrictions specific to the subsidiary that is the legal

counterparty to the agreement. Under our long-term debt agreements, acceleration of principal payments would occur upon

payment default, violation of debt covenants not cured within 30 days, a change in control including a person or group

obtaining 50 percent or more of our outstanding voting stock, or breach of certain other conditions set forth in the borrowing

agreements. At December 31, 2012, we were in compliance with all such covenants and restrictions.