Windstream 2012 Annual Report Download - page 105

Download and view the complete annual report

Please find page 105 of the 2012 Windstream annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

|

|

F-7

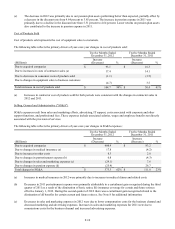

(d) Decreases in traditional voice service revenues were primarily attributable to competition and migration of existing

customers to integrated services and bundled offerings. These declines were partially offset by $8.9 million due to the

implementation of the access recovery charge ("ARC"), which is a monthly charge established by the FCC designed to

mitigate revenue reductions resulting from intercarrier compensation reform implemented in the third quarter of 2012.

Consumer Service Revenues

Consumer service revenues are generated from the provision of high-speed Internet, voice and video services to consumers. We

expect the trend of consumer voice line loss to continue as a result of competition from wireless carriers, cable television

companies and other providers using emerging technologies. For the twelve months ended December 31, 2012, consumer voice

lines decreased by approximately 86,000, or 4.5 percent. Increasing revenues from high-speed Internet and related services

helped offset some of the losses in consumer voice revenues. Demand for faster broadband speeds and Internet-related services,

such as virus protection and online data backup services, are expected to favorably impact consumer high-speed Internet

revenues, offsetting some of the decline in consumer voice revenues.

For the twelve months ended December 31, 2012, consumer high-speed Internet customers increased by approximately 7,000

or 0.6 percent. As of December 31, 2012, we provided high-speed Internet service to approximately 42 percent of total voice

lines in service and approximately 71 percent of primary residential lines in service. As of December 31, 2012, approximately

77 percent of our total voice lines had high-speed Internet competition, primarily from cable service providers. We do not

expect significant additional cable expansions into our service areas during 2013, but we could experience some increased

competition from high-speed Internet offerings of wireless competitors. We expect the pace of high-speed Internet customer

growth to slow as the number of households without high-speed Internet service shrinks and our penetration continues to

increase.

To combat competitive pressures in our markets, we emphasize our bundled service strategy and enhancements to our network

to offer faster Internet speeds. Service bundles provide discounts and other incentives for customers to bundle their voice, long

distance, high-speed Internet and video services and have positively impacted our operating trends.

The following table reflects the primary drivers of year-over-year changes in consumer service revenues:

Twelve Months Ended

December 31, 2012

Twelve Months Ended

December 31, 2011

(Millions)

Increase

(Decrease) %

Increase

(Decrease) %

Due to acquired companies $ — $ 43.1

Due to increases in high-speed Internet revenues (a) 17.9 36.3

Due to changes in miscellaneous revenues (4.7) 1.8

Due to decreases in voice and long distance revenues (b) (52.0) (75.7)

Total changes in consumer revenues $(38.8) (3)% $ 5.5 —%

(a) Increases in high-speed Internet revenues were primarily due to the increase in high-speed Internet customers, continued

migration to higher speeds and increased sales of value added services, as previously discussed.

(b) Decreases in voice service revenues were primarily attributable to declines in voice lines. These declines were partially

offset by $4.8 million due to the implementation of the ARC, described above.

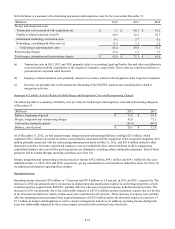

Wholesale Service Revenues

Wholesale service revenues include switched access revenues, Universal Service Fund ("USF") revenues and voice and data

services sold on a wholesale basis.

Switched access revenues include usage sensitive revenues from long distance companies and other carriers for access to our

network in connection with the completion of long distance calls, as well as reciprocal compensation received from wireless

and other local connecting carriers for the use of our facilities. USF revenues are government subsidies designed to partially

offset the cost of providing wireline services in high-cost areas. In addition, we offer our voice and data services on a wholesale

basis to other carriers.