DTE Energy 2014 Annual Report Download - page 41

Download and view the complete annual report

Please find page 41 of the 2014 DTE Energy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

|

|

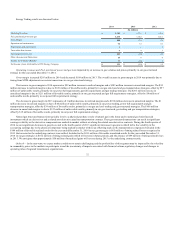

As of October 1, 2014 Valuation Date:

Electric

$ 1,208

38%

7%

9.5x

DCF, assuming stock sale

Gas

743

26%

6%

10.5x

DCF, assuming stock sale

Power and Industrial Projects (d)

26

59%

8%

10.0x

DCF, assuming asset sale (e)

Gas Storage and Pipelines

24

78%

7%

12.5x

DCF, assuming asset sale

Energy Trading

17

45%

10%

n/a

DCF, assuming asset sale

$ 2,018

______________________________________

(a) Percentage by which the fair value of equity of the reporting unit would need to decline to equal its carrying value, including goodwill.

(b) Multiple of enterprise value (sum of debt plus equity value) to earnings before interest, taxes, depreciation and amortization (EBITDA).

(c) Discounted cash flows (DCF) incorporated 2015-2019 projected cash flows plus a calculated terminal value.

(d) Power and Industrial Projects excludes the Biomass reporting unit as this unit has no allocated goodwill.

(e) Asset sales were assumed except for Power and Industrial Projects' reduced emissions fuels projects, which assumed stock sales.

We perform an annual impairment test each October. In between annual tests, we monitor our estimates and assumptions regarding estimated future cash

flows, including the impact of movements in market indicators in future quarters and will update our impairment analyses if a triggering event occurs. While

we believe our assumptions are reasonable, actual results may differ from our projections. To the extent projected results or cash flows are revised downward,

the reporting unit may be required to write down all or a portion of its goodwill, which would adversely impact our earnings.

We evaluate the carrying value of our long-lived assets, excluding goodwill, when circumstances indicate that the carrying value of those assets may

not be recoverable. Conditions that could have an adverse impact on the cash flows and fair value of the long-lived assets are deteriorating business climate,

condition of the asset, or plans to dispose of the asset before the end of its useful life. The review of long-lived assets for impairment requires significant

assumptions about operating strategies and estimates of future cash flows, which require assessments of current and projected market conditions. An

impairment evaluation is based on an undiscounted cash flow analysis at the lowest level for which independent cash flows of long-lived assets can be

identified from other groups of assets and liabilities. Impairment may occur when the carrying value of the asset exceeds the future undiscounted cash flows.

When the undiscounted cash flow analysis indicates a long-lived asset is not recoverable, the amount of the impairment loss is determined by measuring the

excess of the long-lived asset over its fair value. An impairment would require us to reduce both the long-lived asset and current period earnings by the

amount of the impairment, which would adversely impact our earnings.

We sponsor defined benefit pension plans and other postretirement benefit plans for eligible employees of the Company. The measurement of the plan

obligations and cost of providing benefits under these plans involve various factors, including numerous assumptions and accounting elections. When

determining the various assumptions that are required, we consider historical information as well as future expectations. The benefit costs are affected by,

among other things, the actual rate of return on plan assets, the long-term expected return on plan assets, the discount rate applied to benefit obligations, the

incidence of mortality, the expected remaining service period of plan participants, level of compensation and rate of compensation increases, employee age,

length of service, the anticipated rate of increase of health care costs, benefit plan design changes and the level of benefits provided to employees and

retirees. Pension and other postretirement benefit costs attributed to the segments are included with labor costs and ultimately allocated to projects within the

segments, some of which are capitalized.

39