DTE Energy 2014 Annual Report Download - page 71

Download and view the complete annual report

Please find page 71 of the 2014 DTE Energy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

|

|

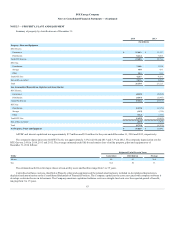

•Removal costs liability — The amount collected from customers for the funding of future asset removal activities.

•Renewable energy — Amounts collected in rates in excess of renewable energy expenditures.

•Over recovery of Securitization — Over recovery of securitization bond expenses.

• Refundable revenue decoupling / deferred gain — Amounts were originally accrued as refundable to DTE Electric customers for the change in

revenue resulting from the difference between actual average sales per customer compared to the base level of average sales per customer

established by the MPSC. In 2012, the MCOA issued a decision reversing the MPSC's decision to authorize a RDM for DTE Electric. The revenue

decoupling liability was reversed and, after receiving an order from the MPSC to defer the resulting gain for future amortization, DTE Electric

created a regulatory liability representing its obligation to refund the gain. The deferred gain is being amortized into earnings in 2014 and 2015.

•Negative pension offset — DTE Gas's negative pension costs are not included as a reduction to its authorized rates; therefore, the Company is

accruing a regulatory liability to eliminate the impact on earnings of the negative pension expense accrued. This regulatory liability will reverse

to the extent DTE Gas’s pension expense is positive in future years.

•Refundable income taxes — Income taxes refundable to DTE Gas’s customers representing the difference in property-related deferred income taxes

payable and amounts recognized pursuant to MPSC authorization.

• Energy optimization (EO) — Amounts collected in rates in excess of energy optimization expenditures.

•Fermi 2 refueling outage — Accrued liability for refueling outage at Fermi 2 pursuant to MPSC authorization.

• Refundable other postretirement costs — Accounting rules for other postretirement benefit costs require, among other things, the recognition in

other comprehensive income of the actuarial gains or losses and the prior service costs or credits that arise during the period but that are not

immediately recognized as components of net periodic benefit costs. DTE Electric and DTE Gas record the favorable impact of actuarial gains or

losses and prior service credits as a regulatory liability since the impact will reduce expense in a future rate setting process as the deferred items are

recognized as a component of net periodic benefit costs.

•Accrued PSCR/GCR refund — Liability for the temporary over-recovery of and a return on power supply costs and transmission costs incurred by

DTE Electric which are recoverable through the PSCR mechanism and temporary over-recovery of and a return on gas costs incurred by DTE Gas

which are recoverable through the GCR mechanism.

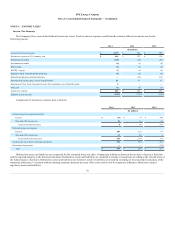

DTE Electric filed a rate case with the MPSC on December 19, 2014 requesting an increase in base rates of $370 million based on a projected twelve-

month period ending June 30, 2016. The requested increase in base rates is due primarily to an increase in net plant resulting from infrastructure investments,

plant acquisitions, environmental compliance and reliability improvement projects. The rate filing also included projected changes in sales, working capital,

operation and maintenance expenses, return on equity and capital structure. New rates could be self-implemented in July 2015, with a final order expected in

December 2015.

-

In July 2013, the MCOA issued a decision relating to an appeal of the October 2011 MPSC order in DTE Electric's October 2010 rate case filing. The

MCOA found that the record of evidence in the 2010 rate case order was insufficient to support the MPSC's authorization to recover costs for the AMI

program and remanded this matter to the MPSC. The MPSC had approved an approximately $11 million rate increase related to the AMI program in the

October 2011 order. DTE Electric is currently operating its AMI program pursuant to the MPSC's approval set forth in the October 2011 order. In August

2013, the MPSC reopened the 2010 electric rate case for the limited purpose of addressing the MCOA's opinion on AMI. On November 6, 2014, the MPSC

issued an order affirming the recovery of costs associated with the AMI program.

68