DTE Energy 2014 Annual Report Download - page 70

Download and view the complete annual report

Please find page 70 of the 2014 DTE Energy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

|

|

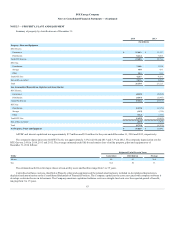

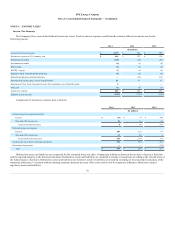

•Recoverable pension and other postretirement costs — Accounting rules for pension and other postretirement benefit costs require, among other

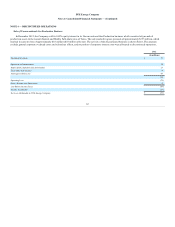

things, the recognition in other comprehensive income of the actuarial gains or losses and the prior service costs that arise during the period but

that are not immediately recognized as components of net periodic benefit costs. DTE Electric and DTE Gas record the impact of actuarial gains or

losses and prior service costs as a regulatory asset since the traditional rate setting process allows for the recovery of pension and other

postretirement costs. The asset will reverse as the deferred items are amortized and recognized as components of net periodic benefit costs. (a)

•Asset retirement obligation — This obligation is primarily for Fermi 2 decommissioning costs. The asset captures the timing differences between

expense recognition and current recovery in rates and will reverse over the remaining life of the related plant. (a)

•Recoverable Michigan income taxes — In July 2007, the MBT was enacted by the State of Michigan. State deferred tax liabilities were established

for the Company’s utilities, and offsetting regulatory assets were recorded as the impacts of the deferred tax liabilities will be reflected in rates as

the related taxable temporary differences reverse and flow through current income tax expense. In May 2011, the MBT was repealed and the MCIT

was enacted. The regulatory asset was remeasured to reflect the impact of the MCIT tax rate. (a)

•Unamortized loss on reacquired debt — The unamortized discount, premium and expense related to debt redeemed with a refinancing are

deferred, amortized and recovered over the life of the replacement issue.

• Other recoverable income taxes — Income taxes receivable from DTE Electric’s customers representing the difference in property-related deferred

income taxes and amounts previously reflected in DTE Electric’s rates. This asset will reverse over the remaining life of the related plant. (a)

• Accrued PSCR/GCR revenue — Receivable for the temporary under-recovery of and carrying costs on fuel and purchased power costs incurred by

DTE Electric which are recoverable through the PSCR mechanism and temporary under-recovery of and carrying costs on gas costs incurred by

DTE Gas which are recoverable through the GCR mechanism.

• Deferred environmental costs — The MPSC approved the deferral of investigation and remediation costs associated with DTE Gas's former MGP

sites. Amortization of deferred costs is over a ten-year period beginning in the year after costs were incurred, with recovery (net of any insurance

proceeds) through base rate filings. (a)

• Cost to achieve Performance Excellence Process (PEP) — The MPSC authorized the deferral of costs to implement the PEP. These costs consist of

employee severance, project management and consultant support. These costs are amortized over a ten-year period beginning with the year

subsequent to the year the costs were deferred.

• Recoverable income taxes related to securitized regulatory assets — Receivable for the recovery of income taxes to be paid on the non-

bypassable securitization bond surcharge. A non-bypassable securitization tax surcharge, which ended in December 2014, was in place to recover

the income tax over a fourteen-year period. (a)

•Removal costs asset — Receivable for the recovery of asset removal expenditures in excess of amounts collected from customers.

•Transitional Reconciliation Mechanism (TRM) — The MPSC approved the recovery of the deferred net incremental revenue requirement

associated with the transition of PLD customers to DTE Electric's distribution system, effective July 1, 2014. Annual reconciliations will be filed

and surcharges will be implemented to recover approved amounts. (a)

•Securitized regulatory assets — The net book balance of the Fermi 2 nuclear plant was written off in 1998 and an equivalent regulatory asset was

established. In 2001, the Fermi 2 regulatory asset and certain other regulatory assets were securitized pursuant to PA 142 and an MPSC order. A

non-bypassable securitization bond surcharge, which ended in December 2014, was in place to recover the securitized regulatory asset over a

fourteen-year period.

_________________________________

(a) Regulatory assets not earning a return or accruing carrying charges.

67