Electronic Arts 2004 Annual Report Download - page 55

Download and view the complete annual report

Please find page 55 of the 2004 Electronic Arts annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

|

|

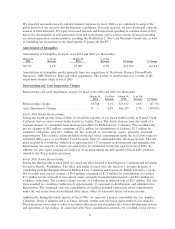

Interest and other income, net, in Ñscal 2003 decreased from Ñscal 2002 primarily due to an other-than-

temporary impairment of investments in aÇliates of $10.6 million in Ñscal 2003, partially oÅset by higher

interest income in Ñscal 2003 of $5.1 million, as a result of higher average cash balances during the Ñscal year.

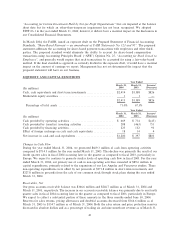

Income Taxes

Income taxes for Ñscal years 2003 and 2002 (in thousands):

March 31, EÅective March 31, EÅective

2003 Tax Rate 2002 Tax Rate % Change

$143,049 31.0% $45,969 31.0% 211.2%

Our eÅective tax rate was 31.0 percent for Ñscal 2003 and Ñscal 2002.

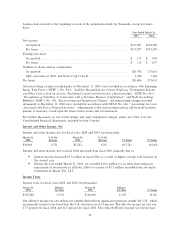

Net Income

Net income for Ñscal years 2003 and 2002 (in thousands):

March 31, % of Net March 31, % of Net

2003 Revenue 2002 Revenue $ Change % Change

$317,097 12.8% $101,509 5.9% $215,588 212.4%

Reported net income increased in Ñscal 2003 compared to Ñscal 2002 primarily due to the reasons discussed

above. Although the dollar amount of expenses rose in Ñscal 2003 versus Ñscal 2002, net income as a

percentage of net revenue increased to 12.8 percent versus 5.9 percent as expenses grew at a slower rate than

did our net revenue.

Impact of Recently Issued Accounting Standards

In January 2003, the Financial Accounting Standards Board (""FASB'') issued Interpretation No. 46

(""FIN 46''), ""Consolidation of Variable Interest Entities''. This interpretation of Accounting Research

Bulletin No. 51, ""Consolidated Financial Statements,'' addresses consolidation by business enterprises of

variable interest entities (""VIEs'') that either (i) do not have suÇcient equity investment at risk to permit the

entity to Ñnance its activities without additional subordinated Ñnancial support, or (ii) are owned by equity

investors who lack an essential characteristic of a controlling Ñnancial interest. This interpretation applies

immediately to VIEs created after January 31, 2003. With regard to VIEs already in existence prior to

February 1, 2003, the implementation of FIN 46 was delayed and currently applies to the Ñrst Ñscal year or

interim period beginning after December 15, 2003. FIN 46 requires disclosure of VIEs in Ñnancial statements

issued after January 31, 2003, if it is reasonably possible that as of the transition date (i) we will be the

primary beneÑciary of an existing VIE that will require consolidation, or (ii) we will hold a signiÑcant variable

interest in, or have signiÑcant involvement with, an existing VIE. We adopted FIN 46 in the quarter ended

December 31, 2003; however, it did not have a material impact on our consolidated Ñnancial position or

results of operations.

In January 2003, the Emerging Issues Task Force reached consensus on Issue No. 00-21 (""EITF 00-21''),

""Revenue Arrangements with Multiple Deliverables''. EITF 00-21 provides guidance on how to determine

whether an arrangement involving multiple deliverables requires that such deliverables be accounted for

separately. EITF 00-21 allows for prospective adoption for arrangements entered into after June 15, 2003 or

adoption via a cumulative eÅect of a change in accounting principle. We adopted EITF 00-21 in the quarter

ended June 30, 2003; however, it did not have a material impact on our consolidated Ñnancial position or

results of operations.

In March 2004, the Emerging Issues Task Force ratiÑed the consensus reached on paragraphs 6 through 23 of

Issue No. 03-01 (""EITF 03-1''), ""The Meaning of Other-Than-Temporary Impairment and Its Application

to Certain Investments''. EITF 03-1 requires that certain quantitative and qualitative disclosures should be

required for debt and marketable equity securities classiÑed as available-for-sale or held-to-maturity under

SFAS No. 115, ""Accounting for Certain Investments in Debt and Equity Securities'' and SFAS No. 124,

40