Electronic Arts 2004 Annual Report Download - page 77

Download and view the complete annual report

Please find page 77 of the 2004 Electronic Arts annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

|

|

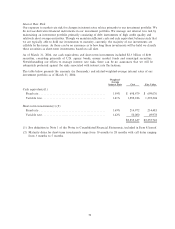

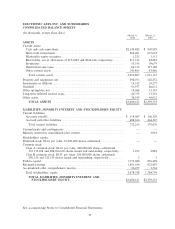

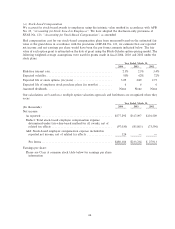

(i) Long-Lived Assets

We evaluate long-lived assets and certain identiÑable intangibles for impairment, in accordance with

SFAS No. 144, ""Accounting for the Impairment or Disposal of Long-Lived Assets'', whenever events or

changes in circumstances indicate that the carrying amount of an asset may not be recoverable. Recoverability

of assets is measured by a comparison of the carrying amount of an asset to future undiscounted net cash

Öows expected to be generated by the asset. This may include assumptions about future prospects for the

business that the asset relates to and typically involves computations of the estimated future cash Öows to be

generated by these businesses. Based on these judgments and assumptions, we determine whether we need

to take an impairment charge to reduce the value of the asset stated on the Consolidated Balance Sheet to

reÖect its actual fair value. Judgments and assumptions about future values and remaining useful lives are

complex and often subjective. They can be aÅected by a variety of factors, including but not limited to,

signiÑcant negative industry or economic trends, signiÑcant changes in the manner of our use of the acquired

assets or the strategy of our overall business and signiÑcant under-performance relative to expected historical

or projected future operating results. If such assets are considered to be impaired, the impairment to be

recognized is measured by the amount by which the carrying amount of the asset exceeds its fair value. During

Ñscal 2004, 2003 and 2002, we recorded $0.5 million, $66.3 million and $12.8 million, respectively, of asset

impairment charges in accordance with SFAS No. 144. See Note 5 of the Notes to Consolidated Financial

Statements.

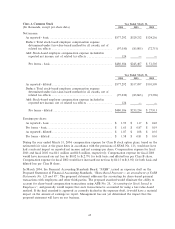

(j) Concentration of Credit Risk

We extend credit to various companies in the retail and mass merchandising industry. Collection of trade

receivables may be aÅected by changes in economic or other industry conditions and may, accordingly, impact

our overall credit risk. Although we generally do not require collateral, we perform ongoing credit evaluations

of our customers and reserves for potential credit losses are maintained. As of March 31, 2004, we had

17.3 percent and 11.3 percent of our gross accounts receivable outstanding with Pinnacle, a European logistics

and collections company, and Wal-Mart Stores, Inc., respectively. As of March 31, 2003, there were no

customers with receivable balances greater than 10 percent of total gross accounts receivables.

Short-term investments are placed with high credit-quality Ñnancial institutions or in short-duration high

quality securities. We limit the amount of credit exposure in any one Ñnancial institution or type of investment

instrument.

(k) Revenue Recognition

We evaluate the recognition of revenue based on the criteria set forth in SOP 97-2, ""Software Revenue

Recognition'', as amended by SOP 98-9, ""ModiÑcation of SOP 97-2, Software Revenue Recognition, With

Respect to Certain Transactions'' and StaÅ Accounting Bulletin (""SAB'') No. 101, ""Revenue Recognition in

Financial Statements'', as revised by SAB 104, ""Revenue Recognition''. We evaluate revenue recognition

using the following basic criteria:

䡵Evidence of an arrangement: We recognize revenue when we have evidence of an agreement with

the customer reÖecting the terms and conditions to deliver products.

䡵Delivery: Delivery is considered to occur when the products are shipped and risk of loss has been

transferred to the customer. For online games, revenue is recognized as the service is provided.

䡵Fixed or determinable fee: If a portion of the arrangement fee is not Ñxed or determinable, we

recognize that amount as revenue when the amount becomes Ñxed or determinable.

䡵Collection is deemed probable: At the time of the transaction, we conduct a credit review of each

customer involved in a signiÑcant transaction to determine the creditworthiness of the customer.

Collection is deemed probable if we expect the customer to be able to pay amounts under the

arrangement as those amounts become due. If we determine that collection is not probable, we

recognize revenue when collection becomes probable (generally upon cash collection).

Product Revenue: Product revenue, including sales to resellers and distributors (""channel partners''), is

recognized when the above criteria are met. We reduce product revenue for estimated customer returns, price

62