Electronic Arts 2013 Annual Report Download - page 180

Download and view the complete annual report

Please find page 180 of the 2013 Electronic Arts annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

|

|

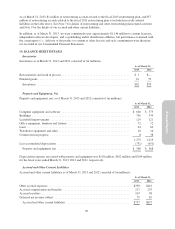

(14) STOCK-BASED COMPENSATION AND EMPLOYEE BENEFIT PLANS

Valuation Assumptions

We are required to estimate the fair value of share-based payment awards on the date of grant. We recognize

compensation costs for stock-based payment awards to employees based on the grant-date fair value using a

straight-line approach over the service period for which such awards are expected to vest.

We determine the fair value of our share-based payment awards as follows:

•Restricted Stock Units, Restricted Stock, and Performance-Based Restricted Stock Units. The fair value

of restricted stock units, restricted stock, and performance-based restricted stock units (other than

market-based restricted stock units) is determined based on the quoted market price of our common

stock on the date of grant. Performance-based restricted stock units include grants made (1) to certain

members of executive management primarily granted in fiscal year 2009 and (2) in connection with

certain acquisitions.

•Market-Based Restricted Stock Units. Market-based restricted stock units consist of grants of

performance-based restricted stock units to certain members of executive management that vest

contingent upon the achievement of pre-determined market and service conditions (referred to herein

as “market-based restricted stock units”). The fair value of our market-based restricted stock units is

determined using a Monte-Carlo simulation model. Key assumptions for the Monte-Carlo simulation

model are the risk-free interest rate, expected volatility, expected dividends and correlation coefficient.

•Stock Options and Employee Stock Purchase Plan. The fair value of stock options and stock purchase

rights granted pursuant to our equity incentive plans and our 2000 Employee Stock Purchase Plan

(“ESPP”), respectively, is determined using the Black-Scholes valuation model based on the multiple-

award valuation method. Key assumptions of the Black-Scholes valuation model are the risk-free

interest rate, expected volatility, expected term and expected dividends.

The determination of the fair value of market-based restricted stock units, stock options and ESPP is affected by

assumptions regarding subjective and complex variables. Generally, our assumptions are based on historical

information and judgment is required to determine if historical trends may be indicators of future outcomes.

The estimated assumptions used in the Black-Scholes valuation model to value our stock option grants and ESPP

were as follows:

Stock Option Grants ESPP

Year Ended March 31, Year Ended March 31,

2013 2012 2011 2013 2012 2011

Risk-free interest rate ......... 0.4-1.0% 0.4 - 1.8% 0.3 - 2.6% 0.1 - 0.2% 0.1 - 0.2% 0.2 - 0.3%

Expected volatility ............ 40-46% 40-46% 39-45% 35-42% 39-41% 34-38%

Weighted-average volatility .... 43% 43% 42% 38% 41% 36%

Expected term ............... 4.4years 4.4 years 4.2 years 6-12 months 6-12 months 6-12 months

Expected dividends ........... None None None None None None

The estimated assumptions used in the Monte-Carlo simulation model to value our market-based restricted stock

units were as follows:

Year Ended

March 31, 2013

Year Ended

March 31, 2012

Risk-free interest rate ................................................ 0.2-0.4% 0.2 - 0.6%

Expected volatility .................................................. 17-116% 14 - 83%

Weighted-average volatility ........................................... 35% 35%

Expected dividends .................................................. None None

There were no market-based restricted stock units granted during the fiscal year ended March 31, 2011.

96