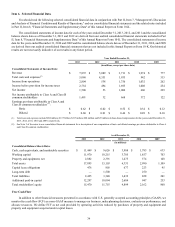

Facebook 2013 Annual Report Download - page 45

Download and view the complete annual report

Please find page 45 of the 2013 Facebook annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

|

|

43

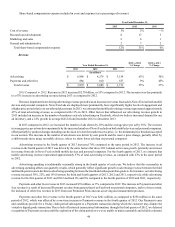

satisfied in connection with our IPO in May 2012. Therefore, we did not recognize any expense relating to the granting of the Pre-2011

RSUs until the completion of our IPO. For the Pre-2011 RSUs, we recognize share-based compensation expense using the accelerated

attribution method, net of estimated forfeitures, in which compensation cost for each vesting tranche in an award is recognized ratably

from the service inception date to the vesting date for that tranche.

RSUs granted on or after January 1, 2011 (Post-2011 RSUs) are not subject to a liquidity condition in order to vest, and compensation

expense related to these grants is based on the grant date fair value of the RSUs and is recognized on a straight-line basis over the applicable

service period. The majority of Post-2011 RSUs are earned over a service period of four to five years. For Post-2011 RSUs, which are

only subject to a service condition, we recognize share-based compensation expense on a ratable basis over the requisite service period

for the entire award.

We account for share-based employee compensation plans under the fair value recognition and measurement provisions in

accordance with applicable accounting standards, which require all share-based payments to employees, including grants of stock options

and RSUs, to be measured based on the grant-date fair value of the awards.

Share-based compensation expense is recorded net of estimated forfeitures in our consolidated statements of income and as such

is recorded for only those share-based awards that we expect to vest. We estimate the forfeiture rate based on historical forfeitures of

equity awards and adjust the rate to reflect changes in facts and circumstances, if any. We will revise our estimated forfeiture rate if actual

forfeitures differ from our initial estimates.

We have historically issued unvested restricted shares to employee stockholders of certain acquired companies. As these awards

are generally subject to continued post-acquisition employment, we have accounted for them as post-acquisition share-based compensation

expense. We recognize compensation expense equal to the grant date fair value of the common stock on a straight-line basis over the

employee's required service period.

Loss Contingencies

We are involved in various lawsuits, claims, investigations and proceedings that arise in the ordinary course of business. Certain

of these matters include speculative claims for substantial or indeterminate amounts of damages. We record a liability when we believe

that it is both probable that a loss has been incurred and the amount can be reasonably estimated. Significant judgment is required to

determine both probability and the estimated amount. We review these provisions at least quarterly and adjust these provisions accordingly

to reflect the impact of negotiations, settlements, rulings, advice of legal counsel, and updated information.

We believe that the amount or estimable range of reasonably possible loss, will not, either individually or in the aggregate, have

a material adverse effect on our business, consolidated financial position, results of operations, or cash flows with respect to loss

contingencies for legal and other contingencies as of December 31, 2013. However, the outcome of litigation is inherently uncertain.

Therefore, if one or more of these legal matters were resolved against us for amounts in excess of management's expectations, our results

of operations and financial condition, including in a particular reporting period, could be materially adversely affected.

Business Combinations and Valuation of Goodwill and Other Acquired Intangible Assets

We allocate the fair value of purchase consideration to the tangible assets acquired, liabilities assumed and intangible assets acquired

based on their estimated fair values. The excess of the fair value of purchase consideration over the fair values of these identifiable assets

and liabilities is recorded as goodwill. Such valuations require management to make significant estimates and assumptions, especially

with respect to intangible assets. During the measurement period, which is one year from the acquisition date, we may record adjustments

to the assets acquired and liabilities assumed, with the corresponding offset to goodwill. Upon the conclusion of the measurement period,

any subsequent adjustments are recorded to earnings.

We review goodwill for impairment at least annually or more frequently if events or changes in circumstances indicate that the

carrying value of goodwill may not be recoverable. We have elected to first assess the qualitative factors to determine whether it is more

likely than not that the fair value of our single reporting operating unit is less than its carrying amount as a basis for determining whether

it is necessary to perform the two-step goodwill impairment under Accounting Standards Update (ASU) No. 2011-08, Goodwill and

Other (Topic 350): Testing Goodwill for Impairment, issued by the Financial Accounting Standards Board (FASB). If we determine that

it is more likely than not that its fair value is less than its carrying amount, then the two-step goodwill impairment test will be performed.

The first step, identifying a potential impairment, compares the fair value of the reporting unit with its carrying amount. If the carrying

amount exceeds its fair value, the second step will be performed; otherwise, no further step is required. The second step, measuring the

impairment loss, compares the implied fair value of the goodwill with the carrying amount of the goodwill. Any excess of the goodwill

carrying amount over the applied fair value is recognized as an impairment loss, and the carrying value of goodwill is written down to

fair value. As of December 31, 2013, no impairment of goodwill has been identified.

Acquired intangible assets are amortized over their estimated useful lives. We evaluate the recoverability of amortizable intangible

assets for possible impairment whenever events or circumstances indicate that the carrying amount of such assets may not be recoverable.

Recoverability of these assets is measured by a comparison of the carrying amounts to the future undiscounted cash flows the assets are