Microsoft 2008 Annual Report Download - page 31

Download and view the complete annual report

Please find page 31 of the 2008 Microsoft annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

|

|

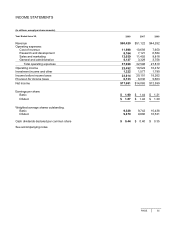

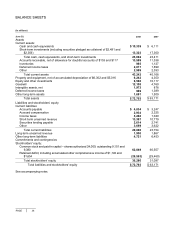

PAGE 30

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND

RESULTS OF OPERATIONS (CONTINUED)

Recent Accounting Pronouncements Not Yet Adopted

In March 2008, the FASB issued SFAS No. 161, Disclosures about Derivative Instruments and Hedging Activities,

an amendment of FASB Statement No. 133, which requires additional disclosures about the objectives of the

derivative instruments and hedging activities, the method of accounting for such instruments under SFAS No. 133

and its related interpretations, and a tabular disclosure of the effects of such instruments and related hedged

items on our financial position, financial performance, and cash flows. SFAS No. 161 is effective for us beginning

January 1, 2009. We are currently assessing the potential impact that adoption of SFAS No. 161 may have on our

financial statements.

In December 2007, the FASB issued SFAS No. 141R, Business Combinations, which replaces SFAS No. 141.

The statement retains the purchase method of accounting for acquisitions, but requires a number of changes,

including changes in the way assets and liabilities are recognized in the purchase accounting. It also changes the

recognition of assets acquired and liabilities assumed arising from contingencies, requires the capitalization of in-

process research and development at fair value, and requires the expensing of acquisition-related costs as

incurred. SFAS No. 141R is effective for us beginning July 1, 2009 and will apply prospectively to business

combinations completed on or after that date.

In December 2007, the FASB issued SFAS No. 160, Noncontrolling Interests in Consolidated Financial

Statements, an amendment of ARB No. 51, which changes the accounting and reporting for minority interests.

Minority interests will be recharacterized as noncontrolling interests and will be reported as a component of equity

separate from the parent’s equity, and purchases or sales of equity interests that do not result in a change in

control will be accounted for as equity transactions. In addition, net income attributable to the noncontrolling

interest will be included in consolidated net income on the face of the income statement and, upon a loss of

control, the interest sold, as well as any interest retained, will be recorded at fair value with any gain or loss

recognized in earnings. SFAS No. 160 is effective for us beginning July 1, 2009 and will apply prospectively,

except for the presentation and disclosure requirements, which will apply retrospectively. We are currently

assessing the potential impact that adoption of SFAS No. 160 may have on our financial statements.

In February 2007, the FASB issued SFAS No. 159, The Fair Value Option for Financial Assets and Financial

Liabilities. SFAS No. 159 gives us the irrevocable option to carry many financial assets and liabilities at fair

values, with changes in fair value recognized in earnings. SFAS No. 159 is effective for us beginning July 1, 2008.

We do not believe SFAS No. 159 will have a material impact on our financial statements.

In September 2006, the FASB issued SFAS No. 157, Fair Value Measurements, which defines fair value,

establishes a framework for measuring fair value in generally accepted accounting principles, and expands

disclosures about fair value measurements. This statement does not require any new fair value measurements,

but provides guidance on how to measure fair value by providing a fair value hierarchy used to classify the source

of the information. In February 2008, the FASB issued FASB Staff Position (“FSP”) 157-2, Effective Date of FASB

Statement No. 157, which delays the effective date of SFAS No. 157 for all nonfinancial assets and nonfinancial

liabilities, except for items that are recognized or disclosed at fair value in the financial statements on a recurring

basis (at least annually). SFAS No. 157 is effective for us beginning July 1, 2008; FSP 157-2 delays the effective

date for certain items to July 1, 2009. We do not believe SFAS No. 157 will have a material impact on our

financial statements.

APPLICATION OF CRITICAL ACCOUNTING POLICIES

Our financial statements and accompanying notes are prepared in accordance with U.S. GAAP. Preparing

financial statements requires management to make estimates and assumptions that affect the reported amounts

of assets, liabilities, revenue, and expenses. These estimates and assumptions are affected by management’s

application of accounting policies. Critical accounting policies for us include revenue recognition, impairment of

investment securities, impairment of goodwill, accounting for research and development costs, accounting for

contingencies, accounting for income taxes, accounting for stock-based compensation, and accounting for

product warranties.

We account for the licensing of software in accordance with American Institute of Certified Public Accountants

Statement of Position (“SOP”) 97-2, Software Revenue Recognition. The application of SOP 97-2 requires

judgment, including whether a software arrangement includes multiple elements, and if so, whether vendor-

specific objective evidence (“VSOE”) of fair value exists for those elements. For some of our products, customers

receive certain