Microsoft 2008 Annual Report Download - page 35

Download and view the complete annual report

Please find page 35 of the 2008 Microsoft annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

|

|

PAGE 34

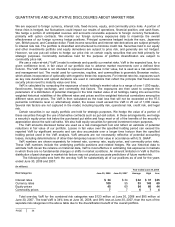

QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK

We are exposed to foreign currency, interest rate, fixed-income, equity, and commodity price risks. A portion of

these risks is hedged, but fluctuations could impact our results of operations, financial position, and cash flows.

We hedge a portion of anticipated revenue and accounts receivable exposure to foreign currency fluctuations,

primarily with option contracts. We monitor our foreign currency exposures daily to maximize the overall

effectiveness of our foreign currency hedge positions. Principal currencies hedged include the euro, Japanese

yen, British pound, and Canadian dollar. Fixed-income securities and interest rate derivatives are subject primarily

to interest rate risk. The portfolio is diversified and structured to minimize credit risk. Securities held in our equity

and other investments portfolio and equity derivatives are subject to price risk, and generally are not hedged.

However, we use put-call collars to hedge our price risk on certain equity securities that are held primarily for

strategic purposes. Commodity derivatives held for the purpose of portfolio diversification are subject to

commodity price risk.

We use a value-at-risk (“VaR”) model to estimate and quantify our market risks. VaR is the expected loss, for a

given confidence level, in fair value of our portfolio due to adverse market movements over a defined time

horizon. The VaR model is not intended to represent actual losses in fair value, but is used as a risk estimation

and management tool. The model used for currencies, equities, and commodities is geometric Brownian motion,

which allows incorporation of optionality with regard to these risk exposures. For interest rate risk, exposures such

as key rate durations and spread durations are used in calculations that reflect the principle that fixed-income

security prices revert to maturity value over time.

VaR is calculated by computing the exposures of each holding’s market value to a range of over 1,000 equity,

fixed-income, foreign exchange, and commodity risk factors. The exposures are then used to compute the

parameters of a distribution of potential changes in the total market value of all holdings, taking into account the

weighted historical volatilities of the different rates and prices and the weighted historical correlations among the

different rates and prices. The VaR is then calculated as the total loss that will not be exceeded at the 97.5

percentile confidence level or, alternatively stated, the losses could exceed the VaR in 25 out of 1,000 cases.

Several risk factors are not captured in the model, including liquidity risk, operational risk, credit risk, and legal

risk.

Certain securities in our equity portfolio are held for strategic purposes. We hedge the value of a portion of

these securities through the use of derivative contracts such as put-call collars. In these arrangements, we hedge

a security’s equity price risk below the purchased put strike and forgo most or all of the benefits of the security’s

appreciation above the sold call strike. We also hold equity securities for general investment return purposes.

The VaR amounts disclosed below are used as a risk management tool and reflect an estimate of potential

reductions in fair value of our portfolio. Losses in fair value over the specified holding period can exceed the

reported VaR by significant amounts and can also accumulate over a longer time horizon than the specified

holding period used in the VaR analysis. VaR amounts are not necessarily reflective of potential accounting

losses, including determinations of other-than-temporary losses in fair value in accordance with U.S. GAAP.

VaR numbers are shown separately for interest rate, currency rate, equity price, and commodity price risks.

These VaR numbers include the underlying portfolio positions and related hedges. We use historical data to

estimate VaR. Given the reliance on historical data, VaR is most effective in estimating risk exposures in markets

in which there are no fundamental changes or shifts in market conditions. An inherent limitation in VaR is that the

distribution of past changes in market risk factors may not produce accurate predictions of future market risk.

The following table sets forth the one-day VaR for substantially all of our positions as of and for the years

ended June 30, 2008 and 2007:

(In millions)

Year ended June 30, 2008

Risk Categories June 30, 2008 June 30, 2007

Average High Low

Interest rates $34 $ 34 $ 32 $37 $25

Currency rates

1

00 55 93

1

45 60

Equity prices 45 60 54 60 44

Commodity prices 7 7 6 7 4

Total one-day VaR for the combined risk categories was $123 million at June 30, 2008 and $95 million at

June 30, 2007. The total VaR is 34% less at June 30, 2008, and 39% less at June 30, 2007, than the sum of the

separate risk categories in the above table due to the diversification benefit of the overall portfolio.