Microsoft 2008 Annual Report Download - page 44

Download and view the complete annual report

Please find page 44 of the 2008 Microsoft annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

|

|

PAGE 43

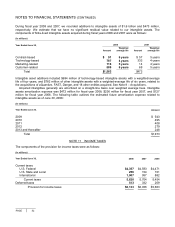

PROPERTY AND EQUIPMENT

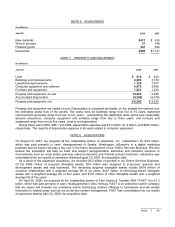

Property and equipment is stated at cost and depreciated using the straight-line method over the shorter of the

estimated life of the asset or the lease term, ranging from one to 15 years. Computer software developed or

obtained for internal use is depreciated using the straight-line method over the estimated useful life of the

software, generally three years or less.

GOODWILL

Goodwill is tested for impairment on an annual basis as of July 1, and between annual tests if indicators of

potential impairment exist, using a fair-value-based approach. No impairment of goodwill has been identified

during any of the periods presented.

INTANGIBLE ASSETS

Intangible assets are amortized using the straight-line method over their estimated period of benefit, ranging from

one to ten years. We evaluate the recoverability of intangible assets periodically and take into account events or

circumstances that warrant revised estimates of useful lives or that indicate that impairment exists. All of our

intangible assets are subject to amortization. No material impairments of intangible assets have been identified

during any of the periods presented.

RECENTLY ISSUED ACCOUNTING STANDARDS

Recently Adopted Accounting Pronouncements

On July 1, 2007, we adopted the provisions of Financial Accounting Standards Board (“FASB”) Interpretation

No. 48 (“FIN 48”), Accounting for Uncertainty in Income Taxes – an interpretation of FASB Statement No. 109,

which provides a financial statement recognition threshold and measurement attribute for a tax position taken or

expected to be taken in a tax return. Under FIN 48, we may recognize the tax benefit from an uncertain tax

position only if it is more likely than not that the tax position will be sustained on examination by the taxing

authorities, based on the technical merits of the position. The tax benefits recognized in the financial statements

from such a position should be measured based on the largest benefit that has a greater than 50% likelihood of

being realized upon ultimate settlement. FIN 48 also provides guidance on derecognition of income tax assets

and liabilities, classification of current and deferred income tax assets and liabilities, accounting for interest and

penalties associated with tax positions, and income tax disclosures. Upon adoption, we recognized a $395 million

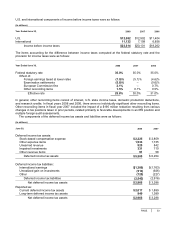

charge to our beginning retained deficit as a cumulative effect of a change in accounting principle. See Note 11 –

Income Taxes.

On July 1, 2007, we adopted Emerging Issues Task Force Issue No. 06-2 (“EITF 06-2”), Accounting for

Sabbatical Leave and Other Similar Benefits Pursuant to FASB Statement No. 43. EITF 06-2 requires companies

to accrue the costs of compensated absences under a sabbatical or similar benefit arrangement over the requisite

service period. Upon adoption, we recognized a $17 million charge to our beginning retained deficit as a

cumulative effect of a change in accounting principle.

Recent Accounting Pronouncements Not Yet Adopted

In March 2008, the FASB issued SFAS No. 161, Disclosures about Derivative Instruments and Hedging Activities,

an amendment of FAS 133, which requires additional disclosures about the objectives of derivative instruments

and hedging activities, the method of accounting for those instruments under SFAS No. 133 and its related

interpretations, and a tabular disclosure of the effects of those instruments and related hedged items on our

financial position, financial performance, and cash flows. SFAS No. 161 is effective for us beginning January 1,

2009. We are currently assessing the potential impact that adoption of SFAS No. 161 may have on our financial

statements.

In December 2007, the FASB issued SFAS No. 141R, Business Combinations, which replaces SFAS No 141.

The statement retains the purchase method of accounting for acquisitions, but requires a number of changes,

including changes in the way assets and liabilities are recognized in the purchase accounting. It also changes the

recognition of assets acquired and liabilities assumed arising from contingencies, requires the capitalization of in-

process research and development at fair value, and requires the expensing of acquisition-related costs as

incurred. SFAS No. 141R is effective for us beginning July 1, 2009 and will apply prospectively to business

combinations completed on or after that date.