Target 2003 Annual Report Download - page 19

Download and view the complete annual report

Please find page 19 of the 2003 Target annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

|

|

17

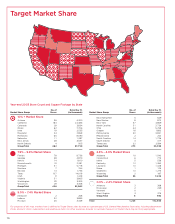

Analysis of Operations

Target Corporation operates large-format general merchandise

stores in the United States, including discount stores, moderate-

priced promotional stores and traditional department stores, and

additionally operates a small, rapidly growing on-line business. We

drive incremental merchandise sales and profitability through

increases in our comparable-store sales and through contribution

of new store growth at Target. Additionally, we benefit from our

credit card operations which strategically support each of our retail

segments. We focus on delighting our guests by offering both

everyday essentials and fashionable, differentiated merchandise at

exceptional prices. Our ability to deliver a shopping experience that

is preferred by our guests is supported by our strong supply chain

and technology network, a devotion to innovation which is ingrained

in our organization and culture and our disciplined approach to

managing our current business and investing in future growth.

Though our industry is highly competitive and subject to macro-

economic conditions, we believe we are well-positioned to deliver

continued profitable market share growth for many years to come.

On March 10, 2004, we began reviewing strategic alternatives

for Mervyn’s and Marshall Field’s that include but are not limited

to, the possible sale of one or both of these segments as ongoing

businesses to existing retailers or other qualified buyers. The follow-

ing Management’s Discussion and Analysis, Consolidated Financial

Statements, and Notes to Consolidated Financial Statements do

not reflect any impact of any strategic alternatives as we are in

the early stages of this review process.

Management’s Discussion and Analysis is based on our

Consolidated Financial Statements as shown on pages 26-29.

Revenues and

Comparable-store Sales

Total revenues include retail sales and

net credit card revenues. Net credit

card revenues represent income

derived from finance charges, late

fees and other revenues from use of

our Target Visa and proprietary credit

cards. Comparable-store sales are

sales from stores open longer than

one year. Stores that were remodeled

at their existing location and did not

convert to a SuperTarget remain in

the comparable-store sales calculation.

Stores that have been converted to

a SuperTarget or moved to a new

location are included in the comparable-store sales calculation

once they are open longer than one year.

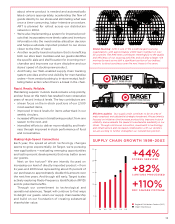

In 2003, total revenues increased 9.7 percent and comparable-

store sales increased 2.9 percent. Retail price deflation had a negative

impact of approximately 3 percent on sales growth. At Target,

which accounted for 86 percent of our total revenues, slightly

more than half of our 12 percent increase in revenues was driven

by new store expansion, while the rest of the increase resulted

from a 4.4 percent increase in comparable-store sales and an

increase in net credit card revenues. Mervyn’s and Marshall Field’s,

which accounted for 7 percent and 5 percent of our total revenues,

respectively, experienced a decline in revenues, primarily due to

decreases in comparable-store sales.

In 2002, total revenues increased 10.3 percent and comparable-

store sales increased 1.1 percent. Retail price deflation had a negative

impact of approximately 3 percent on sales growth. At Target,

which accounted for 84 percent of our total revenues, the increase

was driven by new store expansion, an increase in net credit card

revenues and a 2.2 percent increase in comparable-store sales.

Mervyn’s and Marshall Field’s, which accounted for 9 percent and

6 percent of our total revenues, respectively, experienced a decline

in revenues primarily due to decreases in comparable-store sales.

Revenues and Comparable-store Sales Growth

2003 2002 2001

Comparable- Comparable- Comparable-

store store store

Revenues Sales Revenues Sales Revenues Sales

Target 12.0% 4.4% 13.3% 2.2% 13.1% 4.1%

Mervyn’s (6.9) (7.6) (5.2) (5.3) (1.7) (1.5)

Marshall Field’s (4.0) (2.6) (3.1) (3.7) (5.2) (5.7)

Total 9.7% 2.9% 10.3% 1.1% 9.7% 2.7%

Revenues per Square Foot*

2003 2002 2001

Target $282 $278 $274

Mervyn’s 165 178 187

Marshall Field’s 178 180 186

* Thirteen-month average retail square feet.

In 2004, we expect revenues to increase due to new store

growth and an increase in comparable-store sales and net credit

card revenues.

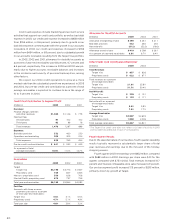

Gross Margin Rate

Gross margin rate represents gross margin (sales less cost of sales)

as a percent of sales. Cost of sales primarily includes purchases,

markdowns and other costs associated with our merchandise. These

costs are partially offset by various forms of consideration earned

or received from our vendors, which we refer to as “vendor income.”

’99 ’00 ’01 ’02 ’03

$33,657

$36,851

$39,826

$43,917

$48,163

45,000

37,500

30,000

22,500

15,000

7,500

Total Revenues

(millions)

MANAGEMENT’S DISCUSSION AND ANALYSIS