Target 2003 Annual Report Download - page 24

Download and view the complete annual report

Please find page 24 of the 2003 Target annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

|

|

22

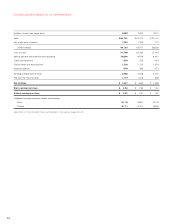

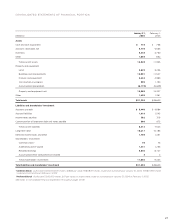

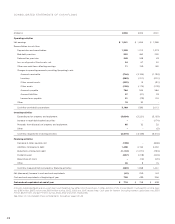

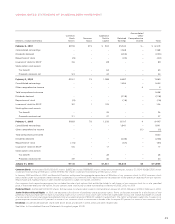

Analysis of Financial Condition

Liquidity and Capital Resources

Our financial condition remains strong.

In assessing our financial condition,

management considers factors such

as cash flows provided by operations,

capital expenditures and debt service

obligations. Cash flow provided by

operations increased to $3.2 billion

in 2003 from $1.6 billion in 2002,

primarily due to a smaller increase in

our gross accounts receivable balance

and a higher net income.

During 2003, our total gross year-

end receivables increased 3.9 percent,

or $231 million, to $6,195 million. The

growth in year-end receivables was

driven by modest growth in issuance and usage of the Target Visa

credit card during 2003. Average total receivables in 2003 increased

21 percent reflecting the substantial growth of the Target Visa

credit card portfolio throughout 2002.

During 2003, inventory levels increased $583 million, or

12.2 percent. This growth was more than fully funded by the $764

million increase in accounts payable over the same period. The

increase in inventory was primarily a result of our store square

footage growth.

In January 1999 and March 2000, our Board of Directors

authorized the aggregate repurchase of $2 billion of our common

stock. Since that time, we have repurchased a total of 42 million

shares of our common stock at a total cost of $1,247 million

($29.39 per share), net of the premium from exercised and expired

put options. In 2001, common stock repurchases were essentially

suspended. Consequently, common stock repurchases did not

have a material impact on our 2003 or 2002 net earnings and

financial position.

Our financing strategy is to ensure liquidity and access to

capital markets, to manage the amount of floating-rate debt and

to maintain a balanced spectrum of debt maturities. Within these

parameters, we seek to minimize our cost of borrowing.

A key to our access to liquidity and capital markets is main-

taining strong investment-grade debt ratings.

Credit Ratings

Standard

Moody’s and Poor’s Fitch

Long-term debt A2 A+ A

Commercial paper P-1 A-1 F1

Securitized receivables Aaa AAA n/a

Interest Coverage Ratio

We view interest coverage as an important indicator of our credit-

worthiness.

Interest coverage ratio represents the ratio of pre-tax earnings

before fixed charges to fixed charges (interest expense and the

interest portion of rent expense). Our interest coverage ratio was

5.5x, 4.9x and 4.7x in 2003, 2002 and 2001, respectively.

Further liquidity is provided by $1.6 billion of committed lines

of credit obtained through a group of 26 banks. Of these credit

lines, an $800 million credit facility expires in June 2004 but

includes a one-year term-out option to June 2005. The remaining

$800 million credit facility expires in June 2008. There were no

balances outstanding at any time during 2003 or 2002 under these

agreements. These committed credit lines as well as most of our

long-term debt obligations contain certain financial covenants. We

are, and expect to remain, well within the compliance requirements

of these covenants. No material debt instrument contains provisions

requiring acceleration of payment upon a debt rating downgrade.

Management believes that cash flows from operations, proceeds

from long-term financing activities and issuance of short-term debt

will be sufficient to fund any seasonal buildup in inventories and meet

other cash requirements, including the refinancing of existing long-

term debt, growth in receivables and projected capital expenditures.

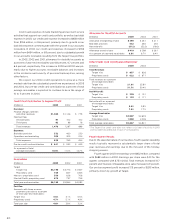

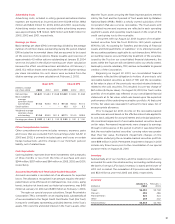

Capital Expenditures

Capital expenditures were $3,004

million in 2003, compared with

$3,221 million in 2002 and $3,163

million in 2001. Our modestly lower

spending level in 2003 is due to a

larger mix of leased stores and our

ability to accomplish our expansion

plans with less capital. Investment in

Target accounted for 90 percent of

capital expenditures in 2003 and

92 percent of capital expenditures in

both 2002 and 2001. Net property

and equipment increased $1,662

million in 2003, compared with an

increase of $1,774 million in 2002.

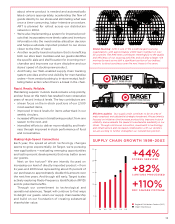

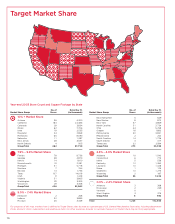

Over the past five years, Target’s net retail square footage has

grown at a compound annual rate of 10 percent, at the higher end

of our objective of 8 to 10 percent in new net growth annually.

Approximately 74 percent and 66 percent of total capital

expenditures in 2003 and 2002, respectively, were for new stores,

expansions and remodels. Other capital investments were for

information system hardware and software, distribution capacity

and other infrastructure to support store growth, primarily at Target.

’99 ’00 ’01 ’02 ’03

$1,918

$2,528

$3,163

$3,221

$3,004

3,000

2,250

1,500

750

Capital

Expenditures

(millions)

’99 ’00 ’01 ’02 ’03

$2,403

$2,134

$2,012

$1,590

$3,160

3,000

2,250

1,500

750

Cash Flow from

Operations

(millions)